Key Takeaways

-

AI monitoring replaces static thresholds with continuous behavioral analysis, catching suspicious patterns before chargebacks or regulatory flags occur.

-

Effective systems combine supervised models, anomaly detection, graph AI, and NLP alongside hard rules for sanctions and compliance limits.

-

False positive reduction requires behavioral baselines, alert clustering, analyst feedback loops, and multi-vote escalation working together.

-

Build costs range from $30,000 for basic rule-based monitoring to $250,000 and above for enterprise AML infrastructure with SAR workflows and multi-region compliance.

-

How Intellivon builds AI transaction monitoring systems your enterprise fully owns, connecting AML, sanctions, fraud models, and audit trails into one real-time financial crime layer.

Every financial platform eventually reaches a stage where the volume, speed, and complexity of transactions exceed what a rules-based monitoring system can manage. Thresholds get manipulated, review queues build up, and the fraud patterns that really cost money are often those that look just legitimate enough to be overlooked. For entrepreneurs creating payment platforms, neobanks, or embedded finance products, this is a scaling problem that comes sooner than expected and hits harder than anticipated.

AI-powered transaction monitoring completely changes the situation. Instead of waiting for a rule to be activated, machine learning models continuously assess behavioral patterns, create dynamic risk profiles, and identify anomalies before they lead to chargebacks, regulatory flags, or reputation problems. For investors and founders focused on building financial infrastructure that performs well at scale, this capability is essential.

Intellivon has developed AI-driven transaction monitoring systems for financial enterprises that operate under strict regulatory demands in various markets. This blog draws on that experience to explain what is needed to create a system that truly works.

![]()

Why Fintechs Need AI Transaction Monitoring Systems Now

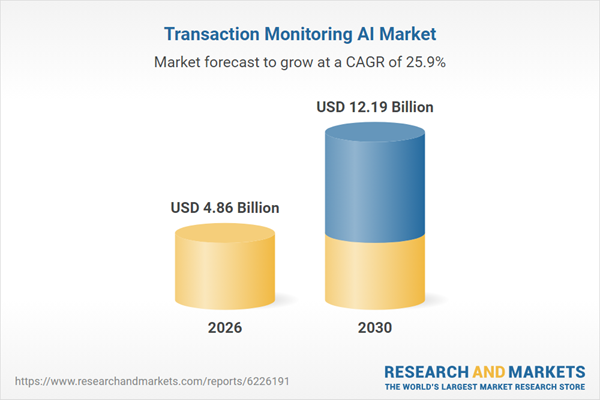

Global scam losses reached $442 billion last year, fraud attacks in financial services climbed 63%, and digital payment volumes continue to grow faster than traditional monitoring infrastructure can handle.

AI-powered transaction monitoring addresses all three pressures simultaneously by reducing false positives by 40 to 65%, enabling real-time compliance, and giving financial platforms the proactive detection capability that the scale of modern fraud demands.

1. Financial crime patterns are becoming more complex

Criminal networks now use automated scripts to move funds through thousands of accounts in seconds. AI identifies these intricate webs by analyzing data points that remain invisible to traditional oversight.

2. Manual reviews cannot scale with transaction volume

Scaling a fintech startup becomes impossible if compliance costs grow linearly with every new user. Automation handles the heavy lifting of initial screening so your experts focus only on the most critical threats.

3. Regulators expect risk-based monitoring controls

Global bodies like FATF and FinCEN now prioritize outcomes over simple rule adherence. Deploying AI demonstrates a sophisticated commitment to risk management that satisfies the most stringent regulatory audits.

4. Real-time payments require real-time risk decisions

Instant settlement leaves no room for delayed manual checks. AI engines score risk in milliseconds, allowing you to block fraudulent transfers before the funds actually leave the ecosystem.

5. AI helps detect behavior rules often missed

Traditional systems only look for known threats. AI identifies subtle shifts in user habits or transaction velocity, catching new fraud techniques the moment they emerge.

Implementing these intelligent systems transforms compliance from a cost center into a competitive advantage for growing fintech enterprises.

What Is an AI-Powered Transaction Monitoring System?

An AI-powered transaction monitoring system is a financial compliance infrastructure that uses machine learning, behavioral analytics, and real-time data processing to detect suspicious activity across every transaction a platform handles.

Unlike rule-based systems that flag predefined patterns, AI models learn continuously, adapt to emerging fraud behaviors, and generate risk signals with the speed and precision that enterprise-scale financial operations require.

1. Why AI improves traditional rule-based monitoring

Traditional systems rely on fixed logic, such as flagging any transfer over $10,000. While easy to understand, these rigid parameters fail to catch criminals who intentionally stay just below the limit.

AI moves beyond these basic thresholds by evaluating the context behind every movement of money.

- Pattern Recognition: Machine learning models identify “smurfing” or “structuring” where multiple small transactions mimic a single large one.

- Adaptive Learning: The system learns from historical data and past investigations to improve its accuracy over time.

- Contextual Analysis: AI looks at user history, device metadata, and geographical shifts to determine if a transaction is truly out of character.

- Reduced Friction: By accurately identifying low-risk behavior, AI prevents unnecessary account freezes that frustrate legitimate customers.

Model Insight: AI-powered monitoring integrates deep learning to analyze non-linear relationships between accounts. This approach identifies money laundering rings that remain invisible to standard “if-then” logic engines.

2. Where transaction monitoring fits in AML programs

Monitoring acts as the continuous surveillance stage within a broader Anti-Money Laundering (AML) framework. It bridges the gap between initial customer onboarding and final regulatory reporting, ensuring ongoing safety after a user is approved.

- Post-Onboarding Surveillance: While Know Your Customer (KYC) verifies identity, transaction monitoring tracks actual behavior throughout the customer lifecycle.

- Risk Scoring: The system assigns a dynamic risk score to every user, allowing teams to focus resources on the highest threats.

- Suspicious Activity Reporting: It automates the collection of evidence required to file reports with government financial intelligence units.

- Audit Readiness: Digital logs provide a transparent trail that proves to auditors your platform actively scans for illicit activity.

Transitioning to an intelligent monitoring framework ensures your enterprise remains compliant without sacrificing the speed your customers expect.

What Problems Should the System Solve First?

Enterprise leaders must prioritize functional outcomes that directly impact the bottom line and regulatory standing.

A precisely engineered AI-powered transaction monitoring system addresses the most draining operational bottlenecks while closing the gaps that leave the platform vulnerable to exploitation.

1. Detecting suspicious transaction patterns early

Speed is the primary defense against irreversible financial loss. This monitoring software identifies anomalies the moment they occur, rather than waiting for end-of-day batch processing to flag a problem.

This proactive stance allows the enterprise to pause high-risk transfers before the capital exits the ecosystem.

2. Reducing false positives in compliance queues

Traditional monitoring often flags legitimate users, creating a mountain of noise for investigators. High false-positive rates waste expensive human capital and frustrate your best customers.

The AI architecture filters out benign deviations by understanding the nuance of individual spending habits, ensuring your team only reviews high-probability threats.

3. Prioritizing alerts by real financial crime risk

Not all alerts carry the same weight or urgency. The monitoring engine ranks every flag based on a multidimensional risk score, considering factors like jurisdiction, counterparty reputation, and velocity. This hierarchy ensures that your compliance officers tackle the most dangerous threats first, maximizing their effectiveness.

4. Linking customer behavior with transaction activity

A transaction is part of a broader user narrative. By connecting login locations, device IDs, and typical spending categories, the AI determines if a specific transfer makes sense for that specific user.

This holistic view makes it much harder for stolen accounts or identity fraud to go unnoticed.

5. Identifying mule accounts and layered transfers

Money laundering often involves moving funds through several “clean” accounts to hide the original source. The system specializes in graph analysis, which maps the relationships between seemingly unrelated users.

- Network Mapping: It identifies clusters of accounts that frequently interact in circular patterns.

- Velocity Tracking: The software flags accounts that receive and immediately transfer funds, a hallmark of money mules.

- Source Tracking: It maintains a digital breadcrumb trail of funds across multiple hops within your platform.

6. Monitoring merchants, wallets, cards, and accounts

Modern platforms are complex, often involving diverse payment methods and user types. A robust monitoring solution must provide a unified view across every touchpoint to prevent siloed data from hiding illicit activity.

- Card Fraud: Identifying cloned cards or “carding” behavior through rapid small-value tests.

- Merchant Risk: Monitoring for transaction laundering where a legitimate business processes payments for an illegal one.

- Wallet Security: Tracking high-frequency transfers between digital wallets that suggest automated layering.

7. Escalating cases before regulatory deadlines

Compliance is a race against the clock. Most jurisdictions have strict windows for reporting suspicious activity, and missing these leads to heavy fines.

The AI tracks the “age” of every alert and automatically moves stagnant cases to senior management to ensure the enterprise remains within legal timelines.

8. Creating evidence for SAR and audit reviews

Generating a Suspicious Activity Report (SAR) is traditionally a manual, time-consuming task. The platform streamlines this by automatically gathering all relevant data points into a structured format for human review.

- Auto-Population: The software pulls transaction history, KYC data, and risk scores into a single file.

- Narrative Support: It provides the technical reasoning behind an alert, helping investigators write faster and more accurate summaries.

- Audit Trail: Every action taken by the engine or the investigator is logged, creating a bulletproof record for future regulatory inspections.

Advanced transaction monitoring utilizes entity resolution to recognize when the same individual operates across different account types.

This capability prevents criminals from bypassing limits by spreading their activity across multiple card or wallet products.

![]()

What Compliance Rules Shape the System Design?

Regulatory compliance serves as the structural blueprint for a secure financial platform.

Engineering a system that aligns with international mandates ensures your enterprise remains shielded from heavy penalties and maintains its institutional reputation.

1. AML and CTF obligations under FATF standards

The Financial Action Task Force (FATF) sets the global benchmark for Anti-Money Laundering (AML) and Counter-Terrorist Financing (CTF). To meet these standards, the system must support cross-border data consistency and high-velocity screening.

This requirement necessitates a design that can process diverse currency formats and regional risk profiles while maintaining a unified global audit trail.

2. BSA and FinCEN suspicious activity reporting

Under the Bank Secrecy Act (BSA), institutions must report transactions that appear suspicious or lack a clear economic purpose. FinCEN’s recent guidance confirms that institutions can utilize risk-based internal controls to automate this monitoring.

Consequently, the system design must include automated workflows that flag, hold, and package these events into standardized reports ready for immediate regulatory filing.

3. Customer due diligence and ongoing monitoring

Compliance does not end after a customer is approved during onboarding. Ongoing monitoring requirements dictate that the software must continuously compare current transaction behavior against the initial “Know Your Customer” (KYC) profile.

If a user’s activity shifts significantly from their declared income or business type, the system must trigger a profile refresh or an enhanced due diligence (EDD) workflow.

4. Sanctions, PEP, and adverse media screening

Global regulations require the immediate freezing of assets belonging to sanctioned individuals or Politically Exposed Persons (PEPs). The system architecture must integrate real-time API feeds from international watchlists.

- Real-time Matching: The engine must screen every sender and receiver against global lists before the transaction settles.

- Fuzzy Logic: The software should account for name variations, misspellings, or different alphabets to prevent criminals from slipping through on technicalities.

- Adverse Media: Advanced systems now scan news and public records to identify emerging risks associated with a specific entity.

5. Risk-based monitoring policies and procedures

Regulators increasingly favor a risk-based approach rather than a one-size-fits-all model. This means the system must be highly configurable, allowing business leaders to set different monitoring intensities for different customer segments.

For instance, a high-volume corporate account in a stable jurisdiction requires a different logic set than a retail user in a high-risk region.

6. Recordkeeping rules for alerts and investigations

Most jurisdictions require financial institutions to maintain records of suspicious activity for at least five years. This necessitates a robust, immutable database within the system design.

- Data Integrity: Every alert, note, and decision made by an investigator must be timestamped and encrypted.

- Retrieval Speed: During a regulatory audit, the platform must be able to pull years of historical data instantly to demonstrate consistent oversight.

7. Data privacy rules for sensitive financial data

Handling financial records requires strict adherence to privacy laws like GDPR or CCPA. The system design must balance the need for deep surveillance with the user’s right to privacy.

This is often achieved through privacy-by-design principles, such as encrypting personal identifiers and restricting access to sensitive data only to authorized compliance officers.

Aligning your infrastructure with these regulatory pillars transforms compliance from a burden into a scalable asset.

A well-integrated AI-powered transaction monitoring system ensures that your business can expand into new markets with the confidence that its legal and operational foundations are secure.

How to Design the Transaction Monitoring Architecture

Building a resilient architecture requires a multi-layered approach that prioritizes data integrity and processing speed.

The following structural components form the backbone of a high-performance system capable of defending an enterprise against complex financial crimes.

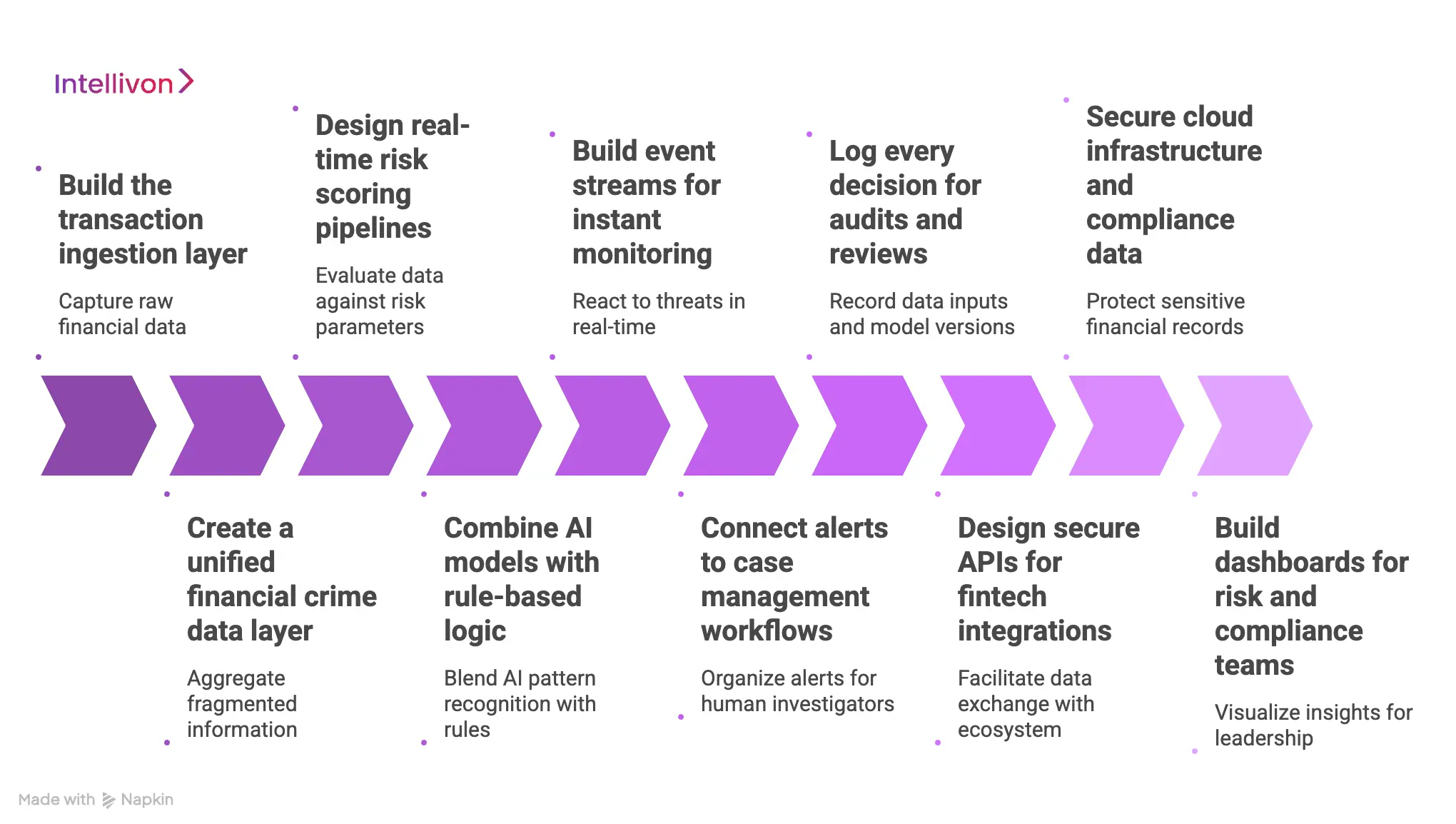

1. Build the transaction ingestion layer

The ingestion layer serves as the system’s entry point, capturing raw financial data from diverse sources like payment gateways, core banking ledgers, and digital wallets. This layer ensures that every event is captured accurately and sequenced correctly to provide a reliable foundation for risk analysis.

- API-based ingestion: RESTful or gRPC APIs.

- Streaming and Event Queues: Apache Kafka, AWS Kinesis, or Google Pub/Sub.

- Data Processing: Apache Flink or Spark Streaming for real-time validation.

- Normalization: Custom middleware for JSON/XML schema mapping and deduplication.

2. Create a unified financial crime data layer

This layer aggregates fragmented information into a single source of truth, combining transaction history with KYC/KYB records and external threat intelligence.

By unifying these datasets, the system gains the context necessary to distinguish between a legitimate high-value transfer and a suspicious one.

- Entity Resolution: Senzing or custom probabilistic matching algorithms.

- Graph Databases: Neo4j, Amazon Neptune, or Memgraph for relationship mapping.

- Feature Stores: Tecton or Feast for managing ML risk signals.

- Storage: Snowflake, Google BigQuery, or Amazon Redshift for structured data lakes.

3. Design real-time risk scoring pipelines

The scoring pipeline is the engine’s decision-making core, where incoming data is evaluated against risk parameters to produce a numerical probability of illicit activity. This process must occur in milliseconds to support modern instant payment environments.

- ML Inference: NVIDIA Triton Inference Server, TensorFlow Serving, or Seldon Core.

- Orchestration: Kubernetes (K8s) for scaling scoring microservices.

- Risk Engines: Custom-built Python/Go scoring services or Drools for business logic.

- Caching: Redis or Aerospike for ultra-low latency lookups of user risk scores.

4. Combine AI models with rule-based logic

A hybrid approach is essential for institutional trust, blending the intuitive pattern recognition of AI with the non-negotiable logic of regulatory rules. While AI discovers new fraud techniques, hardcoded rules ensure that explicit legal limits and sanctions requirements are never bypassed.

- Rules Engines: NRules, Drools, or custom JSON-based rule evaluators.

- Anomaly Detection: Scikit-learn, PyOD, or isolation forests for unsupervised learning.

- Supervised Learning: XGBoost, LightGBM, or CatBoost for known fraud patterns.

- Explainability: SHAP or LIME for generating human-readable decision logic.

5. Build event streams for instant monitoring

Event-driven architecture allows the system to react to threats the moment they are detected rather than processing them in batches. This real-time response capability enables an enterprise to freeze a suspicious account or hold a payment before settlement.

- Message Brokers: RabbitMQ or Apache Pulsar.

- Workflow Automation: Temporal.io or Camunda for managing payment holds.

- Function as a Service (FaaS): AWS Lambda or Google Cloud Functions for triggered alerts.

6. Connect alerts to case management workflows

Once the architecture identifies a threat, it must transition smoothly into the hands of human investigators. This layer organizes alerts into actionable work queues, ensuring no suspicious event is overlooked or delayed beyond regulatory windows.

- Case Management: ServiceNow, JIRA Service Management, or custom React-based dashboards.

- Identity & Access: Okta or Auth0 for secure investigator login.

- Document Storage: Amazon S3 or Google Cloud Storage for encrypted evidence files.

7. Log every decision for audits and reviews

Transparency is a non-negotiable requirement for banking partners and government regulators. This layer meticulously records every data input, model version, and human override to create a bulletproof audit trail of the institution’s compliance efforts.

- Immutable Logging: Amazon QLDB or Hyperledger Fabric for tamper-proof records.

- Log Aggregation: ELK Stack (Elasticsearch, Logstash, Kibana) or Datadog.

- Archiving: AWS Glacier or Google Cloud Storage for long-term regulatory data retention.

8. Design secure APIs for fintech integrations

A transaction monitoring system must communicate seamlessly with the broader financial ecosystem. Secure APIs facilitate the exchange of data between the monitoring engine and external tools like identity providers or core ledgers.

- API Gateway: Kong, Apigee, or AWS API Gateway.

- Authentication: OAuth 2.0 and Mutual TLS (mTLS) for machine-to-machine security.

- Webhooks: Custom event notification systems for real-time platform actions.

9. Secure cloud infrastructure and compliance data

The underlying infrastructure must meet the highest standards of cybersecurity to protect sensitive financial records. Strong security protocols prevent unauthorized access and ensure the system itself does not become a point of vulnerability.

- Cloud Providers: AWS, Azure, or Google Cloud (GCP) with VPC isolation.

- Secrets Management: HashiCorp Vault or AWS Secrets Manager.

- Compliance Tools: Vanta or Drata for continuous SOC 2 and ISO 27001 monitoring.

10. Build dashboards for risk and compliance teams

Dashboards translate complex data into visual insights, allowing leadership to monitor the health of the compliance program at a glance. These tools help teams identify emerging trends, track investigator productivity, and report on overall risk exposure.

- Visualization: Tableau, Power BI, or Looker.

- Real-time UI: Next.js or Vue.js with WebSocket support for live alert feeds.

- Metrics Tracking: Prometheus and Grafana for system and model performance.

A strong transaction monitoring architecture connects data, AI models, and human expertise into a single operating system for financial crime compliance.

Custom engineering creates a significant competitive advantage by securing your platform without compromising user experience.

Which AI Models Work for Transaction Monitoring Systems?

Selecting the right AI model is critical for balancing detection accuracy with operational efficiency.

A high-performance AI-powered transaction monitoring system typically employs a multi-model ensemble to address different types of financial risk.

| Model Category | Primary Use Case | Key Benefit |

| Supervised | Known fraud/AML patterns | High precision for established risks |

| Unsupervised | Emerging/Unknown threats | Detects “black swan” anomalies |

| Graph-Based | Money laundering networks | Uncovers hidden entity relationships |

| Behavioral | Account takeover detection | Identifies shifts in individual habits |

| NLP | Sentiment & Media analysis | Automates context for investigations |

1. Supervised models trained on labeled risk cases

Supervised learning models utilize historical data where transactions have already been marked as “fraudulent” or “legitimate.”

By training on these labels, the system learns the specific characteristics of known criminal activity, such as specific velocity triggers or high-risk country corridors.

2. Unsupervised models for anomaly detection

Unlike supervised versions, these models do not require labeled data; they look for outliers that deviate from the norm.

This is essential for detecting new, “zero-day” money laundering techniques that have not yet been categorized by regulators or law enforcement.

3. Graph models

Graph theory allows the system to visualize the financial ecosystem as a series of nodes and connections.

By analyzing the distance and frequency of transfers between accounts, graph models identify “synthetic identities” and “mule rings” that appear unrelated on the surface.

4. Behavioral models

These models create a unique “fingerprint” for every user based on their typical transaction times, locations, and spending amounts.

If a customer who usually spends $50 at a local grocery store suddenly attempts a $5,000 international wire transfer, the behavioral engine flags the deviation immediately.

5. NLP models for adverse media and case summaries

Natural Language Processing (NLP) scans thousands of news articles, court records, and social feeds to find negative information about a customer or merchant.

It also helps investigators by automatically drafting summaries of suspicious activity, saving hours of manual documentation.

6. Risk scoring models for alert prioritization

Not every flag requires an immediate account freeze. Scoring models aggregate signals from across the platform to assign a numerical risk value.

This ensures that your compliance team focuses on the top 5% of alerts that represent the most significant threats to the enterprise.

7. Hybrid models combining rules and machine learning

Regulatory compliance often requires rigid “if-then” logic for sanctions and limits. Hybrid architectures run these deterministic rules alongside probabilistic AI models, ensuring that the system is both legally compliant and intellectually flexible.

Implementing a diverse suite of models ensures that your AI-powered transaction monitoring framework remains resilient against both traditional fraud and sophisticated, modern financial crimes.

Which Companies Use AI Transaction Monitoring?

Observing how global financial leaders deploy these systems provides a clear benchmark for enterprise-grade success.

Leading institutions have moved beyond experimentation, integrating AI-powered transaction monitoring into the core of their global operations to achieve massive gains in both accuracy and speed.

1. HSBC uses AI for AML transaction monitoring

As one of the world’s largest banking entities, HSBC processes over 1.2 billion transactions every month.

By transitioning to a cloud-based, AI-first approach for Anti-Money Laundering (AML), the bank has fundamentally changed its risk profile.

HSBC reports that this shift reduced false positive alerts by 60% and compressed investigation timelines from several weeks down to just a few days.

2. Stripe uses machine learning to detect payment fraud

Stripe Radar serves as a primary example of how AI-powered transaction analysis protects the modern merchant ecosystem. The system utilizes machine learning to scan patterns across a massive global payment dataset in real time.

This allows the platform to distinguish between legitimate customers and sophisticated fraud rings without adding friction to the checkout process.

3. PayPal scores transaction risk with machine learning

PayPal leverages a dual-sided network of millions of merchants and consumers to train its risk models. Every transaction is assigned a real-time risk score based on a multidimensional analysis of device metadata, IP addresses, and behavioral history. This intelligence allows the system to detect account takeovers and synthetic identity fraud before the funds are moved.

4. ClearBank uses AI for real-time fraud and AML detection

ClearBank utilizes advanced, real-time detection platforms to maintain the integrity of its clearing services. Their architecture is designed to operate across diverse portfolios, making it a critical case study for embedded finance and cloud banking providers.

This approach ensures that as fintech partners scale, the underlying monitoring remains robust and regulator-ready.

5. Bradesco and Lunar use Google Cloud AML AI

Major regional banks like Brazil’s Bradesco and the digital-first Lunar have adopted specialized AML AI products to replace legacy logic. These systems generate risk scores that include “explainable” indicators.

This ensures that when a transaction is flagged, the bank’s investigators know exactly why the AI made that decision, satisfying both internal policy and external regulatory audits.

6. Visa uses Featurespace for AI-native risk detection

Following its late 2024 acquisition of Featurespace, Visa has solidified its position in AI-native financial defense. This technology specializes in analyzing data in real time to stop financial crime at the point of interaction.

By integrating these capabilities, Visa provides its global network of banks and merchants with a sophisticated layer of protection that evolves alongside criminal tactics.

The success of these global institutions demonstrates that AI-powered transaction monitoring is the established standard for high-growth financial enterprises. Adopting these technologies is the most effective way to ensure your platform can handle high volumes while maintaining the highest levels of security and compliance.

How to Reduce False Positives With AI

Operational inefficiency in compliance is almost always driven by noise, like the thousands of harmless transactions flagged by outdated systems.

High false-positive rates drain human capital and delay genuine investigations, making noise reduction a top priority for any AI-powered transaction monitoring strategy.

1. Replacing static thresholds with behavior baselines

Traditional systems flag any transaction over a specific dollar amount, regardless of the user’s history. AI replaces these rigid limits with a dynamic baseline of normal behavior for every individual account.

This shift ensures that a high-value transfer from a corporate entity is cleared immediately, while a sudden $500 spike from a dormant retail account receives the scrutiny it deserves.

2. Grouping similar alerts into fewer investigations

Criminal activity often triggers multiple alerts across different rules, leading to redundant work for compliance teams.

An AI-powered transaction engine can cluster these related flags into a single comprehensive case based on shared entities, IP addresses, or timestamps.

This consolidation allows investigators to see the full picture at once rather than closing dozens of individual, identical tickets.

3. Suppressing low-risk repetitive alerts safely

Certain activities may appear suspicious to a computer but are perfectly explained by a customer’s business model. AI learns to recognize these safe, repetitive patterns over time, such as recurring monthly vendor payments or payroll cycles.

By safely suppressing these low-risk alerts, the system frees up your team to focus on truly anomalous and high-threat events.

4. Using analyst feedback to refine alert logic

Every time a compliance officer dismisses a false positive, the system should learn why that mistake happened. Modern machine learning models incorporate this disposition data back into the training loop.

This continuous feedback cycle ensures the AI-powered transaction monitoring software becomes more accurate with every human interaction, steadily lowering the false-positive rate.

5. Combining rules, AI scores, and risk context

The most effective noise-reduction strategy uses a multi-vote system. A transaction is only escalated if it triggers a rule, receives a high risk score from the AI model, and lacks a reasonable business context.

This layered approach ensures that only the highest-probability threats ever reach the manual review queue.

6. Keeping explainability while reducing alert volume

Regulators will never accept an alert being dismissed just because the AI said so. Every suppressed alert or reduced threshold must be backed by a clear, data-driven rationale.

Advanced systems provide a transparent audit trail for every automated decision, ensuring that your reduction in alert volume does not come at the cost of regulatory transparency.

Reducing false positives transforms compliance from a reactive cost center into a streamlined, high-efficiency operation. Strategic AI integration ensures your investigators spend their time on real risks, protecting your platform without slowing down your business growth.

How to Monitor Crypto and Stablecoin Transactions

Digital asset monitoring presents unique challenges due to the pseudonymous nature of blockchain ledger data.

A robust AI-powered transaction monitoring system must bridge the gap between decentralized activity and traditional compliance standards to ensure every asset movement is fully transparent.

1. Screening wallet addresses and blockchain entities

Every interaction on the blockchain begins with a wallet address. To manage risk, the system must cross-reference these addresses against global databases of known actors, including sanctioned entities, high-risk exchanges, and darknet marketplaces.

- Attribution Engines: Identifying the real-world entity behind an address, such as a known VASP (Virtual Asset Service Provider) or a private unhosted wallet.

- Sanction Scanning: Immediate blocking of any transaction involving addresses listed on OFAC or international watchlists.

2. Detecting mixer, bridge, and layering activity

Criminals use technical tools like mixers or cross-chain bridges to obscure the origin of their funds. Advanced monitoring detects the distinct mathematical signatures of these “obfuscation” techniques, flagging funds that have passed through high-risk protocols before reaching your platform.

- Mixer Detection: Identifying patterns consistent with coin-joining or “tumbling” services designed to hide transaction trails.

- Chain Hopping: Tracking assets as they move across different blockchains (e.g., from Ethereum to Solana) to ensure the audit trail remains intact.

3. Applying Travel Rule and AML expectations

The FATF Travel Rule requires financial institutions to share originator and beneficiary information for virtual asset transfers over certain thresholds.

Your monitoring architecture must integrate messaging protocols that attach identity data to the blockchain transaction, ensuring full regulatory compliance during cross-border transfers.

4. Linking on-chain activity to customer profiles

On-chain data is only useful when connected to the “Know Your Customer” (KYC) data of the account holder.

The system maps blockchain interactions, such as frequent transfers to a specific decentralized exchange, directly to the user’s risk profile, creating a unified view of their financial behavior.

5. Using blockchain analytics for risk scoring

Risk is calculated based on the “taint” or “exposure” of the funds. If a stablecoin transfer originated from a wallet only two hops away from a major hack, the system assigns a high risk score.

- Heuristic Analysis: Using AI to predict the likelihood of an address being part of a larger criminal cluster.

- Risk Taint Metrics: Calculating the percentage of a wallet’s funds that can be traced back to illicit sources.

6. Monitoring stablecoin settlement and transfers

Stablecoins like USDT and USDC are frequently used for settlement due to their price stability. The monitoring engine must treat these assets with the same level of scrutiny as fiat currency, tracking high-velocity transfers that might suggest unauthorized commercial activity or money laundering.

7. Managing fiat and crypto risk in one workflow

The most effective enterprise platforms do not silo crypto and fiat data. By using an integrated AI-powered transaction monitoring workflow, compliance officers can see how a user moves money from a traditional bank account into a digital wallet, providing a complete 360-degree view of potential layering.

Comprehensive blockchain oversight ensures that your platform can embrace digital assets without becoming a conduit for financial crime. Integrating these specialized tools allows you to meet global standards while providing customers with the speed and flexibility of modern crypto finance.

How to Build an AI-Powered Transaction Monitoring System

Building an enterprise-grade AI-powered transaction monitoring platform requires a disciplined engineering roadmap.

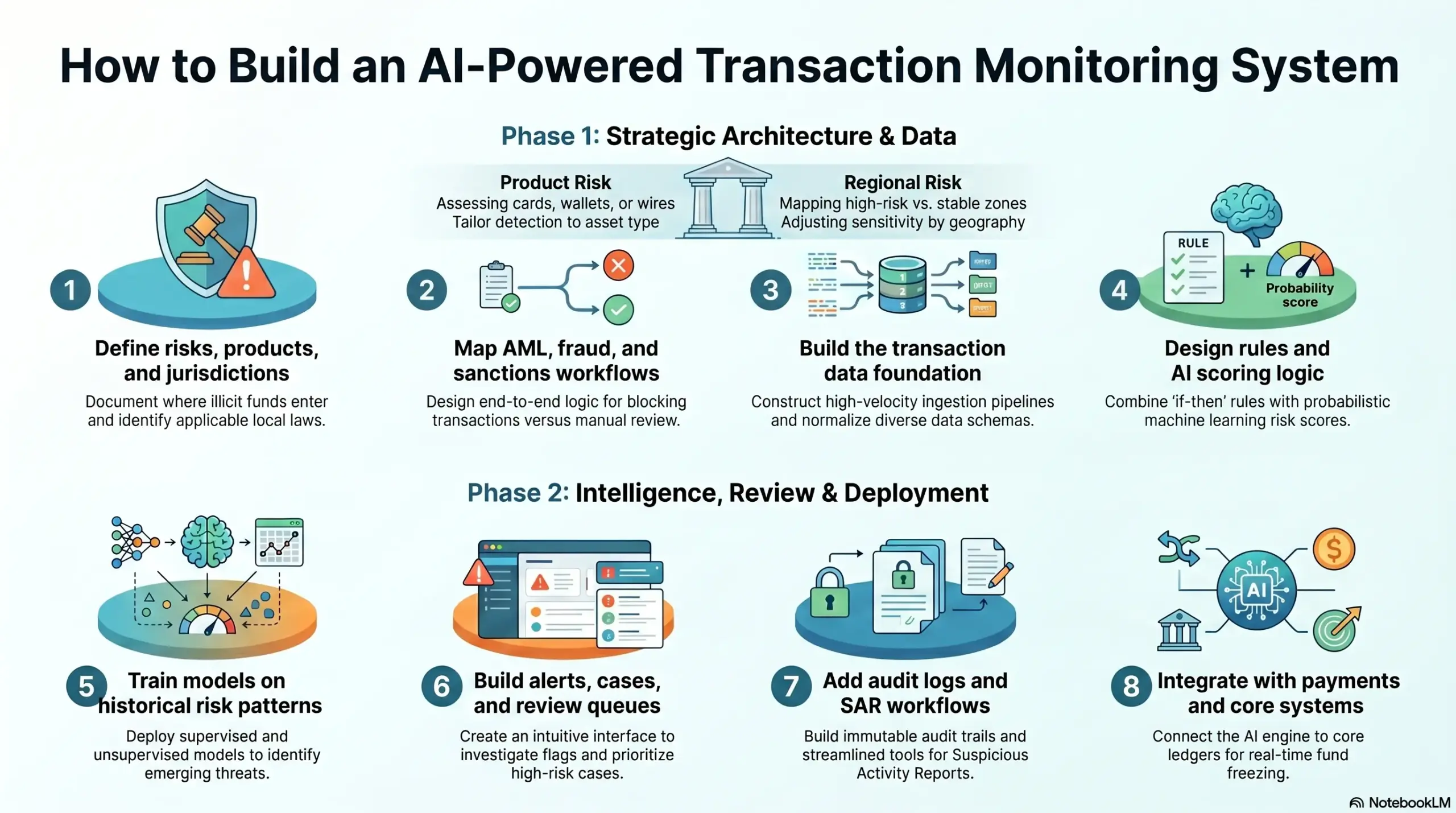

At Intellivon, we follow a rigorous eight-step methodology to ensure the resulting system is resilient, regulator-ready, and perfectly aligned with your specific business model.

Step 1: Define risks, products, and jurisdictions

The foundation of any security system is a clear understanding of the threat landscape. We begin by identifying the specific financial products you offer and the geographic regions where you operate, as these factors dictate your inherent risk level.

| Focus Area | Description | Strategic Goal |

| Product Risk | Assessing cards, wallets, or wires | Tailor detection to asset type |

| Regional Risk | Mapping high-risk vs. stable zones | Adjusting sensitivity by geography |

- Risk Mapping: Documenting exactly where illicit funds are most likely to enter your ecosystem.

- Regulatory Scoping: Identifying which local laws (e.g., EU’s AMLD6 or Singapore’s MAS) apply to your operations.

Step 2: Map AML, fraud, and sanctions workflows

A system is only as good as the processes it automates. We design the end-to-end logic for how the platform should respond when a high-risk event occurs, ensuring no gap exists between detection and action.

- Workflow Logic: Defining when a transaction should be blocked instantly versus held for manual review.

- Sanctions Integration: Ensuring every counterparty is screened against global watchlists before settlement.

- Escalation Paths: Establishing clear protocols for when a standard alert becomes a high-priority case for senior compliance officers.

Step 3: Build the transaction data foundation

Data is the fuel for AI-powered transaction monitoring. We construct high-velocity ingestion pipelines that normalize data from various payment rails, ensuring a clean and consistent stream for analysis.

| Component | Technical Role | Benefit |

| Ingestion | Real-time API / Kafka streams | No data lag in monitoring |

| Normalization | Standardizing diverse schemas | Unified analysis across products |

- Data Integrity: Implementing strict validation rules to prevent “garbage in, garbage out” scenarios.

- Historical Depth: Building data lakes that store years of activity for pattern recognition and audit readiness.

Step 4: Design rules and AI scoring logic

We implement a hybrid decisioning layer that combines deterministic “if-then” rules with probabilistic machine learning scores. This ensures that while absolute limits are enforced, the system remains flexible enough to catch subtle, non-linear patterns of crime.

- Rule Configuration: Hardcoding mandatory limits, such as velocity caps or prohibited merchant categories.

- Score Weighting: Assigning numerical values to various risk signals to create a final, actionable risk percentage.

Step 5: Train models on historical risk patterns

Using your historical data, our data scientists train supervised models to recognize the “signatures” of past fraudulent activity. We also deploy unsupervised models that scan for anomalies, allowing the system to identify emerging threats that rules might miss.

| Model Type | Training Input | Output |

| Supervised | Labeled past fraud cases | High-precision alerts |

| Unsupervised | Raw transaction flows | Outlier/Anomaly detection |

- Backtesting: Running models against past data to prove they would have caught known threats without excessive noise.

- Feature Engineering: Identifying the specific behaviors—like rapid micro-transfers—that correlate with financial crime.

Step 6: Build alerts, cases, and review queues

We transform raw scores into a functional workspace for your compliance team. This stage focuses on creating an intuitive interface where analysts can quickly investigate flags and make informed decisions.

- Case Management: Organizing alerts into logical folders with all necessary context, like user history and device data.

- Prioritization: Automatically moving the highest-risk cases to the top of the queue to prevent “alert fatigue.”

Step 7: Add audit logs and SAR workflows

To satisfy regulators, every action must be recorded. We build an immutable audit trail that logs every data point, model version, and human note, alongside automated tools for filing Suspicious Activity Reports (SARs).

- Immutability: Ensuring that once a decision is made, the record cannot be altered or deleted.

- One-Click Reporting: Streamlining the documentation process so that reporting to authorities takes minutes, not hours.

Step 8: Integrate with payments and core systems

In the final step, the monitoring engine is connected directly to your core ledger or payment processor. This “closed-loop” integration allows the AI-powered transaction monitoring system to send real-time commands to freeze funds or block users.

| Integration Point | Action Taken | Result |

| Core Ledger | Balance hold | Prevents fund withdrawal |

| Payment Gateway | Transaction decline | Stops the transfer mid-stream |

- API Webhooks: Sending instant triggers to your app to notify users or internal teams of a security hold.

- Fail-Safe Protocols: Ensuring that if the monitoring system experiences a lag, the core platform remains secure.

Following this structured path ensures that your compliance infrastructure is not a patchwork of tools but a unified, intelligent operating system. This methodology allows Intellivon to deliver solutions that are robust enough for global enterprises yet flexible enough for fast-moving fintech startups.

How Much Do AI Transaction Monitoring Systems Cost?

AI transaction monitoring system development typically costs between $30,000 and $250,000+, depending on platform complexity, transaction volume, compliance scope, AI model depth, and integration requirements.

A basic monitoring system may only include rules, alerts, and simple dashboards. However, an enterprise-grade platform needs real-time transaction ingestion, AI risk scoring, sanctions screening, case management, SAR workflows, explainability, audit trails, and compliance reporting.

For fintech platforms, banks, payment providers, crypto wallets, and embedded finance companies, the cost depends less on the dashboard and more on the infrastructure behind it.

AI Transaction Monitoring Cost by System Type

| System Type | Estimated Cost | Best For |

| Basic Rule-Based Monitoring System | $30,000–$60,000 | Early-stage fintechs needing basic AML checks, alerts, and manual review workflows |

| AI-Assisted Monitoring Platform | $60,000–$120,000 | Payment apps, wallets, lending platforms, and fintechs need risk scoring and alert prioritization |

| Real-Time AI Monitoring System | $120,000–$180,000 | Platforms handling high transaction volumes, instant payments, card flows, or merchant transactions |

| Enterprise AML Monitoring Infrastructure | $180,000–$250,000+ | Banks, BaaS platforms, PSPs, crypto firms, and multi-region fintech platforms |

Cost Breakdown by Core Development Module

| Module | Estimated Cost |

| Transaction ingestion and data pipelines | $10,000–$35,000 |

| AML rules engine and risk logic | $8,000–$25,000 |

| AI risk scoring models | $20,000–$60,000 |

| Sanctions and watchlist integrations | $8,000–$25,000 |

| Alert generation and prioritization | $10,000–$30,000 |

| Case management workflows | $15,000–$40,000 |

| SAR support and compliance reporting | $10,000–$35,000 |

| Audit trails and evidence logging | $8,000–$30,000 |

| Admin dashboards and analytics | $10,000–$35,000 |

| Security, access control, and cloud setup | $15,000–$45,000 |

Key Factors That Affect Development Cost

Several factors influence the final cost of building an AI-powered transaction monitoring system.

The biggest cost drivers include transaction volume, number of data sources, real-time processing needs, AI model complexity, sanctions and KYC integrations, case management depth, reporting requirements, cloud infrastructure, security controls, and the number of regions the platform operates in.

For example, a single-market fintech app with basic payment flows will cost much less than a multi-region BaaS platform monitoring cards, ACH, wallets, merchants, stablecoins, and partner bank transactions.

At Intellivon, we estimate the cost of an AI transaction monitoring system based on the infrastructure your platform needs, not just the number of features.

We assess your transaction flows, compliance obligations, data sources, AI model requirements, risk workflows, alert volumes, reporting needs, and integration points. Then, we design a monitoring system that fits your current stage while staying scalable for future products, regions, and regulatory expectations.

For early-stage fintechs, this may mean building a focused AML and alerting layer first. For enterprise fintech platforms, it may mean engineering a complete AI-powered financial crime monitoring infrastructure with real-time scoring, explainable decisions, case management, and audit-ready reporting.

Conclusion

Building a sophisticated monitoring infrastructure transforms compliance from a regulatory burden into a strategic growth lever. By integrating intelligent data layers and automated scoring, your platform can scale securely while maintaining institutional trust.

This investment builds the operational resilience required to lead in the global financial landscape. Secure your enterprise today with an architecture designed for the future of digital finance.

Build AI Transaction Monitoring With Intellivon

Building AI transaction monitoring requires more than adding alerts to a compliance dashboard. It needs a real-time financial crime layer where transaction data, AML rules, sanctions checks, fraud signals, AI risk scores, case workflows, and audit trails work together.

At Intellivon, we build AI transaction monitoring systems for fintech platforms, PSPs, digital banks, wallets, lenders, marketplaces, BaaS providers, and embedded finance companies. Our systems help teams detect suspicious activity earlier, reduce false positives, improve investigations, and stay audit-ready as they scale.

A. Designing Real-Time Monitoring Architecture

Transaction monitoring must happen while activity is still actionable. We design systems that screen users, merchants, accounts, wallets, counterparties, and transactions before risk turns into regulatory exposure.

- Real-time data ingestion: Payment, wallet, card, bank transfer, merchant, and ledger activity flows into the monitoring system instantly.

- Unified risk data layer: KYC, KYB, sanctions, fraud, device, location, and transaction history create one risk view.

- Low-latency scoring APIs: Risk checks can run before payment approval, settlement, withdrawal, payout, or account action.

This helps teams detect suspicious activity during the transaction lifecycle, not after delayed reporting.

B. Building AI Risk Scoring and Detection Models

Rules alone often miss hidden patterns and create too many false positives. We build AI models that strengthen monitoring accuracy while keeping decisions explainable for compliance teams.

- Dynamic risk scoring: Each transaction is scored using customer behavior, transaction context, geography, velocity, counterparty risk, and historical patterns.

- Anomaly detection models: AI identifies transaction spikes, new counterparties, unusual device behavior, and abnormal account activity.

- Graph-based detection: The system maps linked users, accounts, merchants, wallets, and counterparties to detect mule networks and layering patterns.

This helps analysts focus on meaningful risk instead of reviewing repetitive, low-value alerts.

C. Connecting AML, Fraud, KYC, and Sanctions

AI transaction monitoring works best when it connects the full compliance ecosystem. We build systems where AML checks, fraud signals, sanctions screening, and customer risk profiles support one risk decision.

- KYC and KYB integrations: Identity checks, business verification, beneficial ownership, and onboarding risk feed into monitoring logic.

- Sanctions and watchlist checks: Users, merchants, wallets, counterparties, and transactions are screened against sanctions, PEP, and adverse media data.

- Risk-based escalation: Low-risk activity clears automatically, while higher-risk events move into review, hold, block, or escalation workflows.

This turns fragmented compliance tools into one connected monitoring system.

D. Creating Case Management and SAR Workflows

Alerts only create value when they lead to structured investigations. We build workflows that help compliance teams review, document, escalate, and resolve suspicious activity faster.

- Investigation-ready queues: Related alerts are grouped by customer, merchant, account, typology, counterparty, or transaction pattern.

- Evidence capture: Each case stores triggered rules, model scores, transaction history, customer data, analyst notes, and review actions.

- SAR support: Case evidence and investigation notes can support suspicious activity reporting, audit reviews, and regulator examinations.

This gives teams a clear path from detection to investigation, decision, reporting, and audit readiness.

Whether you need an MVP monitoring layer, an AI risk scoring engine, AML workflow automation, case management, SAR support, or full financial crime monitoring infrastructure, Intellivon can help you design, build, integrate, and scale it.

Contact Intellivon today to discuss your AI transaction monitoring system and get a development roadmap tailored to your fintech platform.

![]()

FAQs

Q1. How do fintechs handle AML monitoring without compliance staff?

A1. Fintechs without compliance staff need external AML expertise and internal system ownership. Consultants can define policies, but the platform still needs to be configured with alert rules, sanctions checks, escalation paths, review queues, audit records, and clear accountability.

Q2. How can AI reduce false positives in AML alerts?

A2. AI reduces false positives by adding context beyond static thresholds. It reviews customer history, transaction frequency, counterparties, geography, device signals, merchant risk, and past outcomes to separate unusual activity from genuinely suspicious behavior.

Q3. Should transaction monitoring be rule-based or AI-driven?

A3. Transaction monitoring should be hybrid. Rules handle sanctions, limits, thresholds, and known red flags, while AI detects behavior shifts, hidden relationships, mule accounts, layering patterns, and emerging risks that static rules often miss.

Q4. What should an AI transaction monitoring system log?

A4. The system should log transaction details, customer risk, triggered rules, model scores, alert reasons, sanctions results, analyst notes, escalations, overrides, case outcomes, SAR decisions, and model versions so every action remains audit-ready.