Key Takeaways:

- Static routing rules silently cost enterprises revenue through failed transactions, higher interchange fees, and compliance exposure as payment environments scale.

- AI routing engines combine supervised models, reinforcement learning, and ensemble architectures to evaluate gateway performance.

- Sub-100ms routing decisions require Kafka stream processing and regional clusters working together as infrastructure, not just smart models.

- Intelligent retry logic and real-time fallback across multiple rails recover revenue that static systems permanently lose to declines and gateway failures.

- How Intellivon builds AI payment routing systems your enterprise fully owns, with real-time decisioning and compliance-ready explainability from day one.

Payment routing has always been a background function, perceived as something enterprises set up once and rarely revisit. A transaction comes in, a gateway handles it, and the payment either goes through or it does not. The problem is that now payment environments have grown significantly more complex. Businesses operate across multiple gateways, currencies, and regulatory jurisdictions simultaneously. At the same time, a routing decision that worked well six months ago can silently cost a business thousands in failed transactions, higher interchange fees, or compliance exposure today.

AI changes how that decision gets made. Rather than following a fixed set of rules, an intelligent payment routing system evaluates each transaction in real time before assigning a route. The entire process happens in milliseconds, without human intervention. The shift from static routing logic to AI-powered decisioning directly affects approval rates, processing costs, customer experience, and the ability to scale across markets without adding operational complexity.

At Intellivon, we design and build enterprise-grade AI systems that turn payment routing from a passive background process into a precise, intelligent decisioning layer. Our teams have built these architectures across fintech platforms, global merchants, and multi-rail payment processors. This guide covers how intelligent payment routing works, the AI behind it, and how we build one from scratch.

Why Do Enterprises Need Intelligent Routing Now?

The global market for intelligent routing and workflow automation is expanding at a CAGR of roughly 15 to 20 % through 2030. Digital operations are accelerating, regulatory complexity is deepening, and customer expectations for real-time service are rising simultaneously. Together, these forces are exposing a serious gap between what legacy routing infrastructure delivers and what modern enterprises actually require.

Static systems were built for predictable, contained environments. Therefore, they struggle the moment volumes spike, channels multiply, or compliance requirements shift.

Enterprises that continue relying on them face rising costs, slower resolution times, and steadily degrading customer experience.

1. Static Queues Can’t Handle Dynamic Workloads

Rules-based queues like first-in-first-out were designed for stable, low-complexity environments. However, when transaction volumes surge or service level agreements shift, these systems create backlogs, uneven agent load, and buried high-priority cases.

Intelligent routing evaluates channel, risk, priority, and workload in real time, ensuring critical transactions reach the right destination without delay.

2. Compliance, Risk, and Escalation Demands

In regulated industries, every routing decision carries a compliance dimension. Static rules cannot respect jurisdiction boundaries, risk classifications, or reviewer credentials consistently. Consequently, they create blind spots that surface only during audits.

Intelligent routing dynamically escalates flagged items to the correct reviewer pool with a full audit trail, which becomes increasingly critical as global AML and fraud-prevention infrastructure grows at a similar CAGR.

3. Customer Experience and Operational Efficiency

Misrouted interactions and manual re-assignments create friction that customers notice immediately. Intelligent routing reduces handoffs, improves first-contact resolution, and lowers unit-handling costs across the operation.

In addition, consistent routing accuracy becomes a measurable competitive advantage in markets where switching costs are low.

4. The Market Shift to AI-Driven Routing

The market is moving toward systems that blend business rules with machine learning scoring. These platforms predict optimal paths, assess risk dynamically, and integrate directly with CRM, case management, and fraud stacks.

For enterprise leaders, intelligent routing is therefore no longer optional. It is a foundational capability that determines how well a business scales, stays compliant, and retains customers.

For enterprises, intelligent routing is now a core enabler of scalability, compliance, and customer‑centric operations in a digital‑first world.

What Is Intelligent Payment Routing in Payments?

Intelligent payment routing is an AI-powered decisioning system that evaluates each transaction in real time and selects the optimal processing path before routing it to an acquiring bank or payment processor.

Rather than following fixed rules, it weighs live variables such as gateway performance, transaction risk, card type, cost, and compliance requirements simultaneously. The result is higher approval rates, lower processing costs, and faster settlement across every transaction.

Key decision variables across real-time payment flows

Every routing decision relies on a precise set of variables evaluated simultaneously within milliseconds. These inputs determine which path a transaction takes and why.

1. Gateway Performance and Availability

The system monitors each gateway’s live success rates, latency, and uptime continuously. If a gateway is underperforming, traffic reroutes to a healthier alternative before the transaction fails.

2. Transaction Risk Score

Behavioral signals, device data, and historical patterns combine to generate a real-time risk score. High-risk transactions route to stricter verification pathways, while low-risk ones move through frictionlessly.

3. Card Type and Issuer Data

Card network, issuing bank, and card category all influence which processor handles the transaction most efficiently. Routing to the wrong processor for a specific card type directly increases decline rates.

4. Transaction Value and Currency

Higher-value transactions trigger additional validation logic. Cross-border payments factor in currency conversion costs, local acquiring advantages, and settlement speed before a route is assigned.

5. Cost and Interchange Optimization

The system compares processing fees across available gateways in real time. Therefore, each transaction routes through the path that minimizes interchange cost without compromising approval probability.

6. Compliance and Jurisdictional Rules

Regional regulations, data residency requirements, and industry-specific mandates narrow the eligible routing options for each transaction. The system applies these constraints automatically before a gateway is selected.

7. Time and Volume Patterns

Peak traffic periods affect gateway capacity and success rates. Intelligent routing accounts for time-of-day patterns and current volume load to avoid sending transactions into congested processing environments.

Together, these variables give the routing engine the contextual intelligence to make decisions that no static rule set could replicate at scale.

What Factors Decide the Best Payment Route?

Selecting the right payment route is not a single calculation. It is a layered evaluation that weighs multiple live signals simultaneously before a transaction ever moves.

Each factor below plays a distinct role in determining which path produces the best outcome for both the business and the customer.

1. Issuer, Geography, and Currency Decision Signals

Every transaction carries issuer-level data that directly influences routing logic. The issuing bank, the country of origin, and the currency attached to the card all shape which processors are best positioned to handle that specific transaction successfully.

Cross-border transactions require particular attention. A payment initiated in Southeast Asia and processed through a European gateway introduces unnecessary latency and a higher decline probability. In addition, local acquiring often produces significantly better approval rates because processors have established relationships with regional issuers.

Therefore, the routing engine factors geography and issuer identity into every decision before a gateway is selected.

2. Payment Method and Network-Specific Constraints

Different payment methods operate under different network rules. A Visa debit card, an ACH transfer, and a digital wallet each carry their own processing requirements, fee structures, and settlement timelines. Consequently, a routing decision suitable for one method can be entirely wrong for another.

Intelligent routing accounts for these constraints at the method level. The system identifies the payment type first, then narrows the eligible gateway pool to those best equipped to handle it. This approach reduces mismatches that silently increase decline rates and processing costs.

3. Transaction Size, Risk, and Approval Likelihood

Transaction value and risk profile work together to shape routing logic. A high-value transaction from a new device in an unfamiliar location carries a different risk signature than a routine purchase from a recognized customer. The routing engine reads both signals simultaneously.

Higher-risk transactions route through pathways with stronger fraud controls, even if that path carries a marginally higher processing fee. Lower-risk, high-value transactions can route through cost-optimized paths without compromising security.

Furthermore, the system uses historical approval data for similar transaction profiles to predict which gateway is most likely to authorize a given payment before committing to a route.

4. Provider Latency, Uptime, and Success Rates

Gateway performance fluctuates in real time. A processor that delivered strong approval rates yesterday may be experiencing degraded performance today due to technical issues or regional outages. Static routing systems have no mechanism to detect or respond to these shifts.

Intelligent routing monitors every connected provider continuously. As a result, transactions automatically avoid underperforming gateways without any manual intervention. This live performance awareness is one of the clearest differences between AI-driven routing and traditional rule-based systems.

5. Cost Optimization Across Fees and FX Spreads

Processing fees and foreign exchange spreads vary meaningfully across providers. For businesses handling large transaction volumes, even marginal differences in interchange fees compound into high costs over time.

The routing engine compares available fee structures in real time and selects the most cost-efficient path that still meets approval probability and compliance thresholds.

Meanwhile, for cross-border transactions, FX spread optimization runs in parallel, ensuring the business captures the most favorable conversion rate available at that moment. The result is a routing decision that protects both approval rates and margins simultaneously.

Together, these five factors give the routing engine the contextual depth to make decisions that static systems simply cannot replicate. Every variable works in combination, ensuring each transaction takes the path that balances cost, compliance, approval likelihood, and speed simultaneously.

How Does AI Improve Payment Routing Decisions?

Modern payment systems often rely on rigid rules that fail to account for the volatility of global banking networks.

By embedding machine learning into the routing engine, enterprises can transform static decision trees into a fluid infrastructure that anticipates outcomes instead of just reacting to failures.

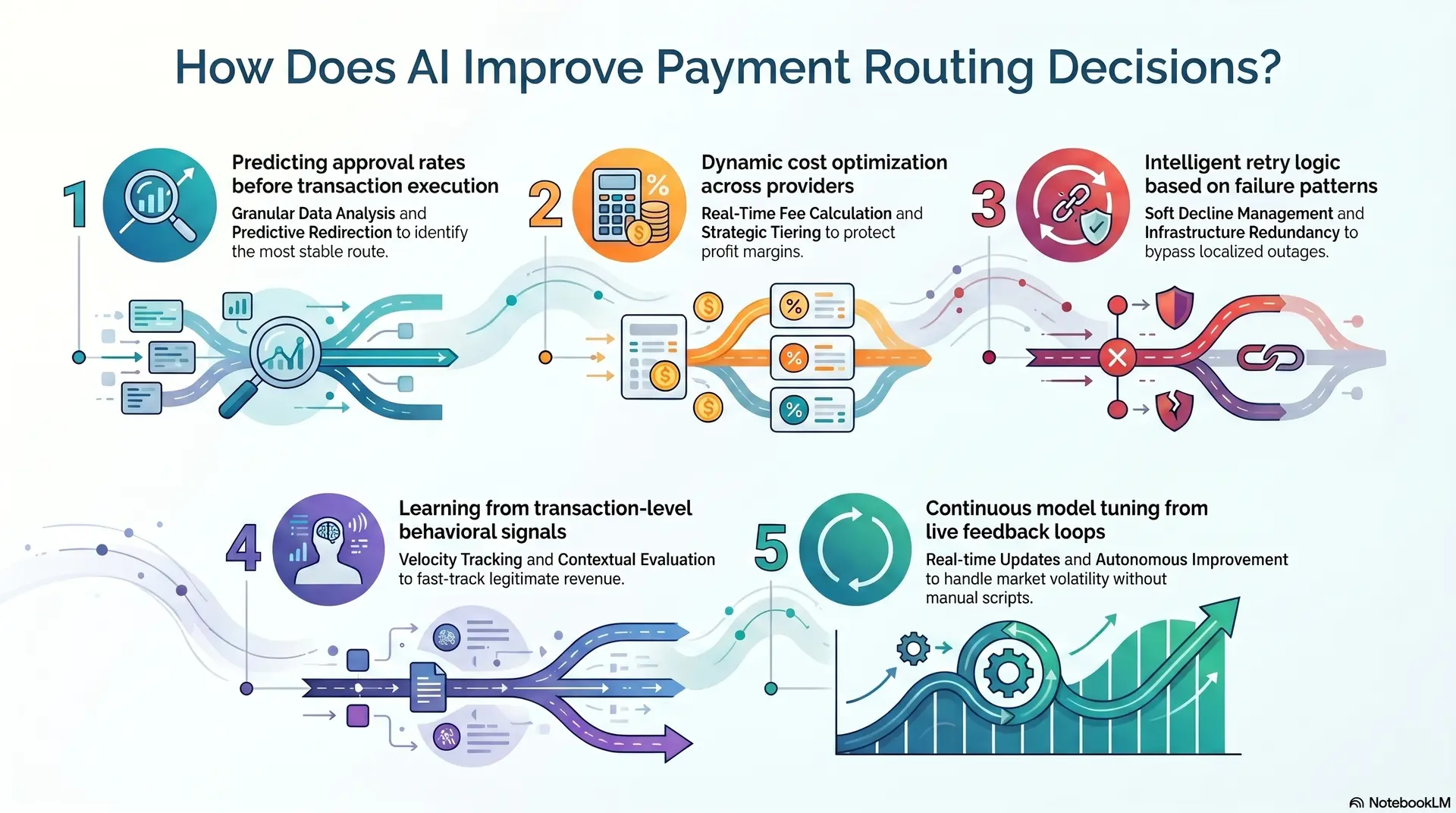

1. Predicting approval rates before transaction execution

Success in high-volume environments depends on knowing which gateway is most likely to authorize a specific card at a specific moment. AI models analyze hundreds of data points to calculate a probability score for each available route before the request is even sent.

- Granular Data Analysis: The system evaluates variables such as bin country, merchant category codes, and current bank latency.

- Predictive Redirection: If a specific processor shows a dip in performance for European credit cards, the system identifies this trend in seconds and diverts traffic to a more stable alternative.

- Friction Reduction: This proactive selection prevents the trial-and-error approach that typically leads to higher decline rates and customer abandonment.

2. Dynamic cost optimization across providers

Payment margins are frequently eroded by complex fee structures, including interchange rates, scheme fees, and cross-border surcharges. An intelligent system evaluates the financial impact of every route in real time to protect the bottom line.

- Real-Time Fee Calculation: The AI balances the urgency of the transaction against the processing cost of the gateway.

- Strategic Tiering: The system might route a low-risk domestic payment through a local provider with lower fees while reserving premium gateways for high-value international transactions.

- Margin Protection: This ensures that the enterprise maintains the highest possible profit margin without compromising the speed or reliability of the checkout experience.

3. Intelligent retry logic based on failure patterns

Not all payment failures are final, but blind retries often trigger fraud alerts or incur unnecessary costs. Intelligent routing uses granular failure codes to determine the most logical next step.

- Soft Decline Management: The system recognizes temporary issues like technical timeouts and schedules an immediate retry through a different gateway.

- Hard Decline Filtering. For stolen cards or invalid accounts, the AI stops the process immediately to protect the merchant’s reputation with networks.

- Infrastructure Redundancy: If a specific banking rail is down, the retry is directed to a completely separate infrastructure to bypass the localized outage.

4. Learning from transaction-level behavioral signals

The depth of AI allows it to see patterns that human analysts would naturally miss over thousands of daily interactions. It looks at the behavior of the transaction itself to assess risk and legitimacy.

- Velocity Tracking: The system monitors the time elapsed since the last purchase and the typical spend velocity for a specific user profile.

- Contextual Evaluation: These signals help the routing engine decide if a transaction needs additional friction or if it can be fast-tracked.

- Revenue Preservation: This level of sophistication ensures that security does not become a bottleneck for legitimate revenue growth.

5. Continuous model tuning from live feedback loops

The most critical advantage of an AI-driven system is that it never stops learning from its own performance. Every successful authorization and every rejected attempt serves as a new data point.

- Real-time Updates As payment processors change their internal risk appetites, the AI adjusts its routing preferences accordingly without manual intervention.

- Adaptive Thresholds The system automatically shifts its logic during peak shopping seasons or regional economic shifts to handle volatility.

- Autonomous Improvement Because the loop is closed and automated, the routing logic stays ahead of industry trends without requiring manual script updates from the IT department.

This shift from manual oversight to automated intelligence allows businesses to reclaim lost revenue and focus on scaling their core operations.

Rule-Based vs AI Routing: What Actually Works?

Choosing between deterministic rules and machine learning is not a binary decision but a strategic calculation of stability against agility.

While many enterprises start with basic logic, the complexity of modern global commerce eventually exposes the limitations of manual intervention.

Comparison: Rules vs. AI Routing

| Feature | Rule-Based Routing | AI-Driven Routing |

| Setup Speed | Fast and straightforward | Requires a data training period |

| Adaptability | Manual updates required | Self-learning and autonomous |

| Accuracy | 100 percent on known paths | Probabilistic and improving over time |

| Maintenance | High overhead as rules multiply | Low manual overhead, but needs monitoring |

| Cost | Fixed, but leads to missed savings | Dynamic and optimized for the lowest fees |

The goal is not to replace human logic with a black box, but to use automation to execute that logic at a scale and speed that humans cannot match.

What Data Powers AI Routing Systems?

An intelligent routing engine is only as accurate as the data feeding it. The quality, freshness, and diversity of inputs determine whether the system makes optimal decisions or educated guesses at scale.

The sections below break down exactly what data the engine relies on and why each layer matters.

1. Transaction Metadata and Behavioral Feature Design

Every transaction generates a rich set of metadata that the routing engine processes instantly. Card type, issuing bank, device fingerprint, and purchase category all contribute to the routing context. Behavioral feature design, then the engineers derived signals from this raw data.

For example, the gap between page load and checkout submission becomes a behavioral feature. So does consistency between the billing address and the device location. Therefore, the engine evaluates not just what the transaction is, but how it arrived. This deeper context improves routing precision at the individual transaction level.

2. Historical Approval and Decline Pattern Analysis

Past transaction outcomes carry strong predictive value. The engine continuously analyzes historical approval and decline patterns across gateway and card combinations. This analysis helps the system anticipate failures before they occur.

If a specific issuer consistently declines transactions through a particular processor on weekends, the engine learns that pattern. It then adjusts routing logic accordingly, without manual intervention. Consequently, approval rates improve continuously as the model accumulates more outcome data over time.

3. Provider Uptime and Performance Telemetry Data

Gateway performance fluctuates throughout the day. Latency, error rates, and processing capacity shift based on traffic volume and infrastructure conditions. The engine ingests live telemetry from every connected provider to maintain an accurate, real-time view.

This monitoring ensures transactions avoid degraded gateways automatically. Furthermore, the system distinguishes between a brief latency spike and a sustained period of underperformance. As a result, routing decisions always reflect current conditions rather than outdated configurations.

4. Issuer-Level and Regional Performance Signals

Approval rates vary across issuers and geographies. A gateway that performs strongly for North American Visa transactions may produce poor results for Southeast Asian debit cards. The engine maintains issuer-level and regional performance profiles to account for these differences.

These signals directly shape gateway selection for cross-border and multi-currency transactions. In addition, local acquiring relationships factor into the model. Regional processors frequently achieve better authorization rates with domestic issuers than international alternatives do.

5. External Fraud, Risk, and Compliance Data Inputs

Internal transaction data alone cannot provide a complete risk picture. Therefore, the engine integrates external sources, including fraud consortium feeds, AML watchlists, device reputation databases, and jurisdictional compliance requirements. These inputs narrow eligible routing options for flagged transactions in real time.

A payment linked to a high-risk device routes through enhanced verification pathways automatically. Meanwhile, regional compliance constraints ensure the system never selects a gateway that creates regulatory exposure. Together, these external signals give the engine a compliance-aware view of every transaction before a route is assigned.

Together, these data layers give the routing engine the situational awareness to make decisions that are accurate, compliant, and commercially optimized across every transaction it processes.

What Architecture Supports AI Routing Systems?

Building a payment engine that thinks in real time requires more than just a smart model. It requires a resilient, high-throughput infrastructure that can process complex logic without introducing latency into the checkout flow.

1. Stateless vs stateful routing service design

The foundation of a modern routing engine often rests on a stateless architecture to ensure maximum agility and reliability.

- Stateless Benefits: By treating each request as an independent event, the system can scale instantly to handle traffic spikes. This design prevents a single failure from cascading through the entire payment pipeline.

- Managing State: While the routing service itself remains stateless, it pulls necessary context from external distributed databases. This allows the system to remember previous attempts without being tethered to a specific server.

- Simplified Updates: Developers can deploy new routing logic or AI models to stateless clusters without disrupting active transactions, which is critical for 24/7 global operations.

2. Stream processing with Kafka or similar systems

Handling millions of transactions requires a robust messaging backbone to ensure data flows smoothly between the checkout and the AI engine.

- Asynchronous Data Flows: Using tools like Kafka allows the system to decouple the immediate payment response from the background analytical tasks. This ensures the customer never waits for the machine learning model to update its internal logs.

- Event Sourcing: Every transaction becomes an event that can be replayed. This is vital for auditing or retraining models on historical data to fix past routing errors.

- Real-Time Analytics: Stream processing enables the system to detect regional bank outages the moment they happen, rather than waiting for an end-of-day report.

3. In-memory caching for sub-100ms decisions

Speed is the primary metric for payment success because every millisecond of delay increases the risk of a timeout or a frustrated customer.

- Redis and Memcached: Storing frequently accessed data like provider health scores and exchange rates in memory allows the AI to make decisions in under 100 milliseconds.

- Latency Reduction: By avoiding slow disk reads, the routing engine can evaluate dozens of gateways and cost variations without the user noticing a pause.

- Dynamic Refresh: The cache is updated in the background as new signals come in, ensuring the AI always works with the most current environmental data.

4. Horizontal scaling across regions and workloads

Enterprises operating globally must ensure that their payment infrastructure is as close to the customer as possible.

- Regional Clusters: Deploying routing nodes across multiple geographic zones reduces the physical distance data must travel, further cutting down on latency.

- Load Balancing: Traffic is distributed across hundreds of smaller instances rather than one large server. This ensures that a surge in North American traffic does not impact European processing.

- Elasticity: The infrastructure automatically expands during peak sales events like Black Friday and shrinks during quiet periods to optimize operational costs.

5. Backpressure handling in high-volume pipelines

When a downstream bank or gateway slows down, the routing system must protect itself from being overwhelmed by its own traffic.

- Flow Control: The architecture includes mechanisms to slow down or queue requests when internal buffers reach capacity. This prevents a complete system crash during extreme congestion.

- Circuit Breakers: If a specific gateway fails repeatedly, the system automatically trips the circuit and stops sending traffic there until the provider is healthy again.

- Graceful Degradation: During times of intense stress, the system can prioritize high-value transactions while temporarily moving low-priority tasks to a slower queue.

6. Fault tolerance and failover design patterns

In the world of payments, even five minutes of downtime can result in millions of dollars in lost revenue and damaged brand trust.

- Active-Active Redundancy: Running multiple live environments simultaneously ensures that if one data center goes dark, the other takes over the entire workload instantly.

- Automated Rollbacks: If a new AI model begins making poor routing decisions, the system can automatically revert to a stable rule-based version within seconds.

- Self-Healing Nodes: The infrastructure monitors the health of every individual service and automatically restarts or replaces any component that shows signs of instability.

Core Architectural Comparison: Speed and Reliability

| Component | Function | Enterprise Value |

| Kafka Streams | Real-time data movement | Prevents data loss during peak volume |

| In-Memory Cache | Sub-100ms data retrieval | Ensures a seamless customer checkout |

| Circuit Breakers | Gateway failure isolation | Protects the system from downstream outages |

| Regional Clusters | Geographic proximity | Minimizes latency for global transactions |

A well-engineered architecture ensures that the intelligence of the system is never hindered by the limitations of the hardware it runs on.

What Features Define a High-Performance System?

Building an intelligent payment routing system requires more than accurate models. The underlying feature set determines whether the system performs reliably at scale, across rails, and under real operating pressure.

1. Multi-Rail Routing Across Cards, RTP, and Wallets

Payment environments today span multiple rails simultaneously. Cards, real-time payment networks, and digital wallets each carry different processing rules, settlement timelines, and fee structures. A high-performance system routes across all of them from a single decisioning layer.

The engine identifies the payment method first. It then selects the most suitable rail based on cost, speed, and approval probability. Therefore, businesses avoid locking customers into a single processing path.

2. Real-Time Retry and Intelligent Fallback Logic

Declines happen even on well-optimized systems. However, a decline does not have to mean a lost transaction. Intelligent fallback logic automatically retries the transaction through an alternative gateway when the primary route fails.

This capability alone recovers a significant share of revenue that static systems permanently lose.

3. Cost-Aware Routing Across Multiple Providers

Processing fees vary across providers, card types, and transaction categories. Over high volumes, even small fee differences compound into substantial costs. Cost-aware routing evaluates available fee structures in real time before assigning a gateway.

The system balances cost against approval likelihood simultaneously. Furthermore, the engine factors in FX spreads for cross-border transactions, ensuring the business captures the most favorable processing cost available at that moment.

4. Latency-Aware Decision Optimization Systems

Routing speed directly affects customer experience. A system that takes too long to assign a route introduces friction at the most sensitive point in the payment flow. Latency-aware optimization ensures the routing decision itself adds no meaningful delay to the transaction.

The engine pre-computes performance scores for connected gateways continuously. As a result, the system delivers routing decisions well within the sub-100 millisecond threshold that modern payment flows require.

5. Integrated Fraud and Risk Signal Handling

Fraud detection and routing logic should not operate as separate systems. When they do, fraud signals often arrive too late to influence the routing decision. An integrated approach feeds risk scores directly into the routing engine before a gateway is selected.

High-risk transactions route through pathways with stronger verification controls automatically. In addition, the system adjusts routing behavior based on live fraud pattern data from external consortium feeds.

Together, these features determine whether a routing system simply moves transactions or actively optimizes every one of them for approval, cost, speed, and security simultaneously.

How Do AI Routing Models Work in Practice?

AI routing models do not operate as a single algorithm, making isolated decisions. They work as a coordinated system where different model types handle different aspects of the routing problem.

Understanding how each model contributes helps clarify why intelligent routing consistently outperforms rules-based alternatives.

1. Supervised Models for Approval Prediction

Supervised learning forms the foundation of most routing engines. These models train on labeled historical data, specifically past transactions with known outcomes such as approved, declined, or flagged.

The model learns which gateway and route combinations produce the best approval rates for specific transaction profiles.

During live routing, the model scores each available gateway against the incoming transaction. It then ranks options by predicted approval probability.

2. Reinforcement Learning for Route Optimization

Supervised models predict outcomes based on historical patterns. Reinforcement learning goes further by optimizing routing decisions through continuous experimentation.

The model treats routing as a sequential decision problem, where each choice generates feedback that shapes the next decision.

The engine receives a reward signal when a transaction approves and a penalty signal when it declines or incurs unnecessary cost. Consequently, the model gradually learns which routing strategies produce the best outcomes across different transaction types and market conditions.

3. Ensemble Models for Higher Decision Accuracy

Single models carry blind spots. A supervised model optimized for approval rates may underweight cost signals. A cost-focused model may miss nuanced fraud indicators.

Ensemble models address this by combining multiple specialized models into a single, unified decision.

Each model in the ensemble evaluates the transaction from its area of focus. The ensemble layer then aggregates these scores using a weighted combination.

4. Real-Time Inference vs Batch Training Trade-offs

Routing engines require real-time inference. Every transaction needs a routing decision within milliseconds of initiation. However, training new models on fresh data is computationally intensive and cannot happen at the same speed. This creates a deliberate separation between inference and training cycles.

The live inference engine runs pre-trained models continuously against incoming transactions. Meanwhile, a separate training pipeline processes accumulated outcome data on a scheduled cycle, ranging from hourly to daily depending on volume.

5. Explainability Requirements in Financial Systems

Financial regulators expect institutions to explain automated decisions clearly. A routing engine that cannot articulate why it selected a specific gateway creates compliance exposure. Explainability modules generate human-readable reason codes for every routing decision the system makes.

These outputs identify which variables carried the most weight in a specific decision. For example, a decision log might indicate that gateway selection was driven primarily by issuer-level performance history and real-time latency data.

Together, these model types work in combination to deliver routing decisions that are accurate, adaptive, cost-aware, and fully defensible under regulatory scrutiny.

How Do You Handle Global Payment Complexity?

Operating across multiple markets introduces layers of complexity that a single routing configuration cannot address. Each region carries its own processing norms, regulatory requirements, and issuer behaviors.

Therefore, global payment systems require routing logic that adapts intelligently to each market in which it operates.

1. Cross-Border Routing Across Multi-Region Systems

Cross-border transactions introduce latency, currency risk, and compliance variables simultaneously. The routing engine evaluates all three before assigning a gateway.

Local acquiring generally produces stronger approval rates than routing cross-border through a single international processor. Consequently, the system prioritizes regional processing wherever available.

2. FX Optimization and Currency Conversion Logic

Currency conversion costs accumulate quickly at scale. The routing engine compares live FX spreads across available providers before selecting a conversion path.

This ensures each cross-border transaction captures the most favorable rate at that moment. Furthermore, the system factors settlement currency preferences to minimize downstream conversion costs for the business.

3. Data Residency and Regional Compliance Handling

Several jurisdictions require transaction data to remain within specific geographic boundaries during processing. The routing engine applies these residency constraints automatically before gateway selection.

Therefore, no transaction routes through a processor that would create a data sovereignty violation. In addition, regional compliance rules such as Strong Customer Authentication in Europe apply dynamically based on the transaction’s origin and destination.

4. Managing Multiple Acquirers and Gateways

Relying on a single acquirer creates concentration risk. Intelligent routing distributes transaction volume across multiple acquirers based on performance, cost, and regional strength. As a result, no single provider failure disrupts the entire payment flow.

The system also balances volume across providers to maintain favorable commercial terms with each.

5. Regional Issuer Behavior and Success Patterns

Issuers in different regions authorize transactions differently. A routing strategy optimized for European issuers may perform poorly with Southeast Asian banks.

The engine maintains regional issuer performance profiles and adjusts gateway selection accordingly. Consequently, approval rates improve across every market the business operates in without manual reconfiguration.

Together, these capabilities allow a single routing system to operate intelligently across global markets while respecting the commercial, regulatory, and technical constraints unique to each region.

How to Build an AI Routing System Step by Step?

Building a payment engine that thinks in real time requires more than just a smart model. It requires a resilient, high-throughput infrastructure that can process complex logic without introducing latency into the checkout flow.

1. Stateless vs stateful routing service design

The foundation of a modern routing engine often rests on a stateless architecture to ensure maximum agility and reliability.

- Stateless Benefits: By treating each request as an independent event, the system can scale instantly to handle traffic spikes. This design prevents a single failure from cascading through the entire payment pipeline.

- Managing State: While the routing service itself remains stateless, it pulls necessary context from external distributed databases. This allows the system to remember previous attempts without being tethered to a specific server.

- Simplified Updates: Developers can deploy new routing logic or AI models to stateless clusters without disrupting active transactions, which is critical for 24/7 global operations.

2. Stream processing with Kafka or similar systems

Handling millions of transactions requires a robust messaging backbone to ensure data flows smoothly between the checkout and the AI engine.

- Asynchronous Data Flows: Using tools like Kafka allows the system to decouple the immediate payment response from the background analytical tasks. This ensures the customer never waits for the machine learning model to update its internal logs.

- Event Sourcing: Every transaction becomes an event that can be replayed. This is vital for auditing or retraining models on historical data to fix past routing errors.

- Real-Time Analytics: Stream processing enables the system to detect regional bank outages the moment they happen, rather than waiting for an end-of-day report.

3. In-memory caching for sub-100ms decisions

Speed is the primary metric for payment success because every millisecond of delay increases the risk of a timeout or a frustrated customer.

- Redis and Memcached: Storing frequently accessed data like provider health scores and exchange rates in memory allows the AI to make decisions in under 100 milliseconds.

- Latency Reduction: By avoiding slow disk reads, the routing engine can evaluate dozens of gateways and cost variations without the user noticing a pause.

- Dynamic Refresh: The cache is updated in the background as new signals come in, ensuring the AI always works with the most current environmental data.

4. Horizontal scaling across regions and workloads

Enterprises operating globally must ensure that their payment infrastructure is as close to the customer as possible.

- Regional Clusters: Deploying routing nodes across multiple geographic zones reduces the physical distance data must travel, further cutting down on latency.

- Load Balancing: Traffic is distributed across hundreds of smaller instances rather than one large server. This ensures that a surge in North American traffic does not impact European processing.

- Elasticity: The infrastructure automatically expands during peak sales events like Black Friday and shrinks during quiet periods to optimize operational costs.

5. Backpressure handling in high-volume pipelines

When a downstream bank or gateway slows down, the routing system must protect itself from being overwhelmed by its own traffic.

- Flow Control: The architecture includes mechanisms to slow down or queue requests when internal buffers reach capacity. This prevents a complete system crash during extreme congestion.

- Circuit Breakers: If a specific gateway fails repeatedly, the system automatically trips the circuit and stops sending traffic there until the provider is healthy again.

- Graceful Degradation: During times of intense stress, the system can prioritize high-value transactions while temporarily moving low-priority tasks to a slower queue.

6. Fault tolerance and failover design patterns

In the world of payments, even five minutes of downtime can result in millions of dollars in lost revenue and damaged brand trust.

- Active-Active Redundancy: Running multiple live environments simultaneously ensures that if one data center goes dark, the other takes over the entire workload instantly.

- Automated Rollbacks: If a new AI model begins making poor routing decisions, the system can automatically revert to a stable rule-based version within seconds.

- Self-Healing Nodes: The infrastructure monitors the health of every individual service and automatically restarts or replaces any component that shows signs of instability.

Core Architectural Comparison: Speed and Reliability

| Component | Function | Enterprise Value |

| Kafka Streams | Real-time data movement | Prevents data loss during peak volume |

| In-Memory Cache | Sub-100ms data retrieval | Ensures a seamless customer checkout |

| Circuit Breakers | Gateway failure isolation | Protects the system from downstream outages |

| Regional Clusters | Geographic proximity | Minimizes latency for global transactions |

A well-engineered architecture ensures that the intelligence of the system is never hindered by the limitations of the hardware it runs on.

How Will AI Change Payment Routing in the Future?

Payment routing is moving from reactive optimization toward fully autonomous decision-making. The systems being built today are laying the foundation for networks that require minimal human oversight and continuously improve on their own.

1. Autonomous Agent-Driven Payment Decisions

AI agents are beginning to initiate and manage payments independently. These agents evaluate routing options, select providers, and execute transactions without waiting for human input. This shift moves routing from a background process into an active, self-directed operation.

Consequently, businesses will process payments faster and with greater precision across complex multi-rail environments.

2. AI-Native Payment Orchestration Platforms

Legacy orchestration platforms bolt AI onto existing infrastructure. The next generation builds AI into the core decisioning layer from the start. AI-native platforms evaluate every routing variable simultaneously rather than processing them sequentially through separate systems.

Therefore, decision quality improves while operational overhead decreases across the entire payment stack.

3. Stablecoin and On-Chain Routing Evolution

Stablecoins and blockchain-based settlement rails are entering enterprise payment flows. Routing engines will need to evaluate on-chain options alongside traditional card and bank rails.

AI will determine when on-chain routing offers a cost or speed advantage over conventional processors. Furthermore, smart contract-based settlement will introduce programmable routing logic that executes automatically based on predefined conditions.

4. Predictive Liquidity-Aware Routing Systems

Future routing engines will factor real-time liquidity positions into every decision. Rather than simply selecting the fastest or cheapest gateway, the system will evaluate provider settlement capacity before routing.

This prevents transactions from routing into liquidity-constrained pathways during peak periods. As a result, settlement reliability improves even when payment volumes surge unexpectedly.

5. Self-Optimizing Global Payment Networks

The endpoint of AI routing evolution is a network that optimizes itself continuously. Every transaction outcome feeds back into the system, refining routing logic without human intervention.

These networks adapt to fraud patterns, provider performance shifts, and regulatory changes in real time. Consequently, the gap between current performance and optimal performance narrows with every transaction processed.

Together, these developments point toward a payment infrastructure that operates with greater autonomy, precision, and resilience than anything static routing logic could deliver.

Conclusion

Intelligent payment routing is no longer a backend configuration decision. It is a core business capability that directly affects approval rates, processing costs, compliance posture, and customer experience.

As payment environments grow more complex and global, the gap between static routing logic and AI-driven decisioning will only widen. The businesses that build this infrastructure now will carry a structural advantage that compounds with every transaction they process.

Why Choose Intellivon for AI Routing Systems?

Building an AI-powered payment routing system requires designing a system where every transaction is evaluated in real time across cost, success probability, latency, and risk.

At Intellivon, we build intelligent routing infrastructure where machine learning is embedded directly into the decisioning layer, enabling higher approval rates, lower transaction costs, and seamless payment experiences across global markets.

Our approach ensures your platform operates reliably under real-world conditions, handling high transaction volumes, dynamic provider performance, and cross-border complexity without compromising speed, accuracy, or compliance.

A. Designing Real-Time Routing Decision Architectures

Payment routing is a real-time decision problem. We design systems where every transaction is evaluated and routed within milliseconds during the payment flow.

- Low-latency decision pipelines: Built for sub-200ms routing without impacting checkout experience

- Event-driven systems: Streaming architectures process transaction signals in real time

- Unified decision engines: Cost, success rate, and latency signals converge into one layer

- Inline routing decisions: Route, retry, or failover actions happen instantly

This ensures routing decisions happen within the transaction lifecycle, not after failures occur.

B. Building Multi-Layered AI Routing Systems

Effective routing requires more than a single model. We design layered systems that combine multiple decision strategies for accuracy and resilience.

- Hybrid model architectures: Supervised and reinforcement models optimize routing paths

- Feature-rich pipelines: Transaction, issuer, and provider signals drive decisions

- Adaptive learning systems: Models evolve continuously based on live performance data

- Decision orchestration layers: Rules and ML models work together for control

This allows your system to optimize both success rates and cost efficiency across all payment flows.

C. Embedding Explainability and Compliance Into the Core

Routing decisions impact revenue and compliance. We build systems that are transparent, auditable, and regulator-ready from the start.

- Transaction-level explainability: Every routing decision is backed by interpretable logic

- Continuous audit trails: Full visibility into routing actions and outcomes

- Standards alignment: Designed for PCI DSS, GDPR, and regional compliance

- Access governance: Secure handling of payment and customer data

This ensures your routing system remains compliant without slowing down real-time operations.

D. Integrating Routing Intelligence Across Your Ecosystem

Routing only works when it connects across your entire payment stack. We design integration layers that unify routing intelligence across systems.

- API-first architecture: Seamless integration with gateways, PSPs, and internal systems

- Multi-provider connectivity: Direct integration with acquirers and payment networks

- Unified performance intelligence: Centralized view of routing outcomes and provider metrics

- Phased system evolution: Upgrade routing capabilities without disrupting operations

This allows your routing system to operate as a centralized intelligence layer, not a fragmented set of integrations.

At Intellivon, we help you translate your payment flows, provider ecosystem, and scaling challenges into a clear AI routing architecture and execution roadmap.

Talk to our team to design a payment routing system tailored to your platform and get a detailed project estimate.

FAQs

Q1. What Is Intelligent Payment Routing in Fintech?

A1. Intelligent payment routing is an AI-powered system that evaluates each transaction in real time and selects the optimal processing path automatically. It weighs variables like gateway performance, fraud risk, card type, cost, and compliance requirements simultaneously. The result is higher approval rates, lower processing costs, and faster settlement across every transaction the system processes.

Q2. How Is AI Routing Different From Rule-Based Logic?

A2. Rule-based systems follow fixed conditions set manually and updated infrequently. AI routing evaluates live variables dynamically and learns from every transaction outcome. Therefore, it adapts to shifting provider performance, emerging fraud patterns, and changing market conditions automatically. Rule-based logic optimizes for known scenarios. AI routing optimizes continuously, including for scenarios it has never encountered before.

Q3. What Integrations Are Required to Build It?

A3. A production-grade system requires integrations across payment gateways, acquiring banks, fraud detection tools, AML and compliance data sources, and internal transaction databases. In addition, real-time data pipelines, feature stores, and observability tooling all require a connection. The depth of integration directly determines how accurately and reliably the routing engine performs under live operating conditions.

Q4. How Secure Are AI Routing Systems in Payments?

A4. AI routing systems operate under strict security standards, including PCI DSS compliance, end-to-end encryption, and role-based access controls. Furthermore, integrated fraud signals and real-time risk scoring add an active security layer to every routing decision. Audit logging captures a complete, tamper-evident record of each decision, supporting both regulatory compliance and dispute resolution processes.

Q5. How Much Does It Cost to Build One?

A5. Build costs vary based on system complexity, number of providers, compliance requirements, and transaction volume. A focused MVP typically ranges from $30,000 to $60,000. A full enterprise-grade system with multi-rail routing, continuous model training, and compliance architecture generally ranges from $100,000 to $300,000 and above. Ongoing infrastructure and model maintenance costs should factor into the total investment calculation.