Key Takeaways:

-

Agentic lending platforms fall into custom builders, bank control planes, orchestration overlays, and specialist platforms.

-

Autonomy boundaries, decision-model explainability, LOS integrations, and fair-lending testing are critical evaluation criteria.

-

ECOA adverse-action support, 2026 model-risk governance, and core banking integrations define regulated-industry requirements.

-

Focused custom builds cost $70,000 to $110,000, while multi-product enterprise builds cost $220,000 to $300,000.

-

How Intellivon builds agentic lending platforms where autonomy boundaries, compliance controls, and decision explainability are built in.

Several companies now build agentic lending platforms that handle loans from application through servicing autonomously. These span consumer credit, mortgage origination, small business lending, and commercial loan decisioning. In practice, the evaluation question is whether agents built by these companies make autonomous decisions or simply automate existing steps. That distinction separates platforms that remove manual work from those that just digitize it.

The companies that lead also go beyond origination to cover servicing, collections, and compliance monitoring. That full lifecycle coverage is what separates the strongest platforms from point-solution vendors. ICE data shows integrated agentic lending platforms generate $1,056 more gross profit per loan. Consequently, platform selection directly affects per-loan profitability, not just processing speed.

This guide evaluates the leading agentic lending platform companies by segment, AI architecture, and compliance depth. Accordingly, this blog covers each company by lending segment, AI capabilities, and compliance posture. By the end, every reader knows which platform fits their lending segment and whether to buy or build.

What Makes an Agentic Lending Platform Different From an AI LOS?

An agentic lending platform does more than predict credit risk or automate isolated data entry tasks. This infrastructure maintains workflow state, retrieves context, chooses permitted tools, executes multi-step actions, observes outcomes, and escalates exceptions.

On the other hand, an AI-enabled loan origination system (LOS) often contains predictive scoring or document extraction features without providing this autonomous orchestration layer.

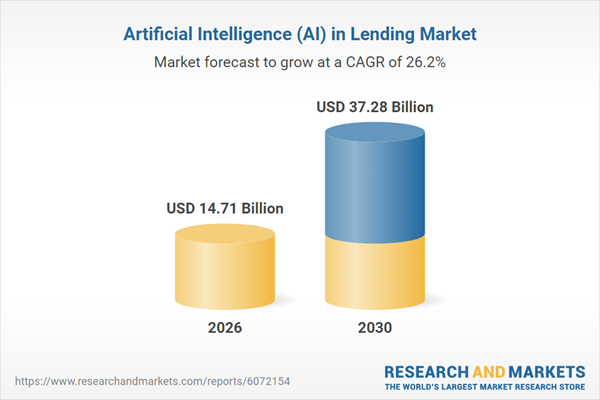

Driven by the rapid adoption of intelligent risk automation and multi-agent workflows, the global artificial intelligence in lending market size is experiencing exponential growth. The sector is growing from $11.63 billion in 2025 to $14.71 billion in 2026, exhibiting an impressive compound annual growth rate (CAGR) of 26.5%.

1. The Four Capabilities Required for Genuine Agentic Lending

An agentic lending platform must possess four distinct capabilities to move beyond basic automation:

- Perception: Ingesting and structuring unstructured applications, bank statements, bureau files, open-banking data, and internal policy records.

- Reasoning: Evaluating the gathered context against strict credit guidelines to determine the next permitted compliance action.

- Execution: Calling approved internal or external APIs, creating workflow tasks, requesting missing evidence, or updating the core system of record.

- Observation: Verifying the result of each executed action to decide whether to proceed, retry a failed call, or escalate to a human underwriter.

This separation guarantees that every action taken by the software agents is traceably logged for compliance audits. Consequently, financial institutions can safely deploy these systems without risking unmonitored decision-making.

2. What Should Not Be Labelled an Agentic Lending Platform

Many legacy software vendors apply the AI label to tools that lack true operational autonomy. The following software tools should not be confused with true agentic infrastructure:

- A standard credit score or a probability-of-default model.

- A standalone document extraction API or OCR tool.

- A customer-facing borrower chatbot or basic interface assistant.

- Robotic Process Automation (RPA) bots or hardcoded rule engines that cannot handle variance.

- A passive credit memo generator.

- A conventional LOS with an integrated AI copilot that requires constant human prompting.

3. A Practical Five-Level Lending Autonomy Scale

Evaluating modern lending software requires a structured framework to measure the precise level of authority granted to the artificial intelligence.

This five-level scale helps technology leaders determine the operational boundaries of any vendor platform.

| Autonomy Level | Platform Authority | Production Example |

| Level 0: No Authority | Search and summarization only. | Finding specific clauses in a commercial loan agreement. |

| Level 1: Assistance | Extracts data or drafts narrative text. | Auto-filling an application screen from a scanned tax return. |

| Level 2: Recommendation | Proposes conditions or next steps. | Suggesting specific clearing conditions based on bureau alerts. |

| Level 3: Bounded Execution | Requests documents and runs system checks. | Automating open-banking verification and chasing missing statements. |

| Level 4: Controlled Decisioning | Approves predefined low-risk cases. | Auto-approving small business loans that match strict risk parameters. |

| Level 5: Unrestricted Autonomy | Fully independent system operation. | Not suitable or permitted for regulated production lending. |

A vendor platform should not receive a high agentic score merely because the software utilizes a large language model. The scoring must measure what the platform can execute independently, what it cannot do, and how each action receives explicit digital authority.

Therefore, assessing these platforms requires a standardized evaluation methodology to separate superficial features from production-ready infrastructure.

How We Evaluated the Top Agentic Lending Platform Companies

The ranking should evaluate enterprise usefulness rather than brand size or marketing language. Each company receives a weighted assessment across orchestration, compliance, integrations, lending coverage, deployment control, and ownership.

A vendor may rank highly for one lending segment without qualifying as the best platform for every institution. Consequently, the scoring prioritizes architectural separation and control layers over superficial artificial intelligence features.

1. Editorial Ranking Scorecard

To provide technology decision-makers with a standard evaluation metric, we utilize a structured breakdown.

This table ensures that the core operational requirements of production-grade software are accurately weighed.

| Evaluation Category | Weight | Questions to Answer |

| Agent architecture and orchestration | 20% | Does it support state, tools, multiple agents, retries, and escalation? |

| Compliance and model-risk controls | 20% | Can it prove policy, model, data, and reason-code lineage? |

| Lending workflow coverage | 15% | Origination only, or underwriting, closing, servicing, and monitoring? |

| Integration depth | 15% | LOS, core, bureau, open banking, CRM, servicing, and document systems? |

| Explainability and evidence | 10% | Can reviewers reconstruct each decision and action? |

| Segment suitability | 10% | Consumer, mortgage, SMB, commercial, construction, or embedded lending? |

| Deployment, ownership, and TCO | 10% | SaaS, private cloud, custom deployment, code ownership, and exit rights? |

2. Evidence Standards Used for the Ranking

Our research prioritizes verifiable structural facts over vendor-reported marketing metrics. Specifically, we focus our analysis on five specific data sources:

- Current official product documentation: Examining the underlying software architecture, including exposed APIs and developer toolkits.

- Named workflows and integrations: Verifying production connections to major bureaus, credit networks, and core systems.

- Published implementation evidence: Analyzing active enterprise deployments, such as Blend’s production rollout of its Autopilot pre-underwriting assistant across 25,500 active mortgage loans.

- Regulatory and technical documentation: Reviewing compliance logging frameworks, model risk management (MRM) policies, and audit trail architectures.

- Customer or operator discussions: Gathering direct feedback from financial institution CTOs and credit officers who run these platforms daily.

Do not rank companies based only on generic “AI-powered” positioning. Instead, the scoring engine demands concrete proof of how an autonomous system interacts with existing infrastructure. This disciplined approach eliminates vendors that merely wrap basic LLMs without engineering a true control layer.

3. Why G2 and Analyst Ratings Need Context

Traditional technology review platforms and analyst magic quadrants group products under traditional loan origination, loan management, and commercial lending categories. Consequently, these aggregated ratings can indicate user experience quality or customer support responsiveness, but they cannot verify advanced multi-agent orchestration.

- Categorization limits: Reviews group tools by legacy categories, missing how well a platform handles multi-agent orchestration or autonomous underwriting controls.

- Missing modern standards: Conventional ratings overlook crucial open standards like the Model Context Protocol (MCP), which gives agents secure, programmatic access to the underlying lending stack.

- Demo vs. production: Relying solely on standard vendor marketplaces carries the risk of licensing software that looks functional in a demo but fails strict bank compliance reviews.

This framework prevents custom builders, legacy LOS vendors, independent document tools, and underwriting-model providers from being treated as identical products. The ranking can now explain what each company actually supplies to an enterprise financial institution.

This analytical clarity allows us to review the leading market players based on their true operational capabilities.

Top 10 Companies Building Agentic Lending Platforms in 2026

When choosing a lending platform, you have two core choices: hire an expert team to build exactly what you need, or license software that is already built. This list details both paths to help your institution make a clear, strategic decision.

Intellivon and Idea Usher occupy the top ranks because they specialize in custom enterprise software development. We build the core processing engine, the visual employee interfaces, and the strict security rules from scratch based on your specific lending criteria. The other eight companies on this list offer “off-the-shelf” software platforms.

These pre-built products are generally faster to set up initially, but they give you less control over how the software functions under the hood.

Vendor Landscape Table

| Rank | Company | Category | Best Fit |

| 1 | Intellivon | Custom builder | Banks need a fully tailored system |

| 2 | Idea Usher | Custom builder | Fintechs building new apps |

| 3 | Backbase | Banking OS | Banks are connecting many old systems |

| 4 | UiPath | Automation overlay | Banks wanting to keep their current LOS |

| 5 | Taktile | Underwriting agent | Business lending teams |

| 6 | Abrigo | Risk platform | Community banks |

| 7 | Built | Real estate platform | Construction lenders |

| 8 | EnFi | AI credit analyst | Commercial banks |

| 9 | Jifiti | Embedded finance | Merchants and retail finance |

| 10 | Zest AI | Underwriting model | Consumer lenders |

1. Intellivon: Best for Fully Custom Lending Systems

Intellivon designs and builds custom software platforms from the ground up for commercial banks, mortgage lenders, and credit unions. Instead of selling a generic subscription, we act as a technical engineering partner to create a proprietary system that your business fully owns.

This custom development approach completely removes long-term software licensing fees and vendor roadblocks.

- What they do: They connect your existing bank systems, such as core databases and credit bureaus, to independent AI agents. These digital workers read complex documents, cross-check financial rules, and run risk analyses.

- Why they’re good: You receive an enterprise platform tailored strictly to your bank’s exact credit policies. Every automated calculation and decision generates a traceably logged audit trail to ensure easy regulatory reviews.

- The Catch: It is not an instant software download. Your executive and credit teams must participate in deep discovery, process mapping, and testing cycles to launch the platform.

The engineering framework separates your credit rules from the underlying AI logic to keep operations completely predictable. Consequently, software agents only execute tasks within strict, pre-approved boundaries.

This protective design gives financial institutions a safe, scalable way to modernize operations without exposing themselves to unexpected credit risks.

2. Idea Usher: Best for Custom Lending Apps

Idea Usher focuses on full-stack software development with a heavy emphasis on mobile application engineering and modern consumer user experiences.

They specialize in building clean, intuitive front-end interfaces for digital neobanks, loan marketplaces, and fast-growing fintech startups.

- What they do: They build user-facing mobile apps, customer application portals, and the background logic required to verify user data.

- Why they’re good: They move quickly from early visual wireframes to final software deployment. Their code ensures that online applicants can upload documents and verify their eligibility with minimal friction.

- The Catch: They excel at customer-facing interfaces, but institutions with complex bank-level risk controls must actively design the backend safety rules.

Their core development methodology prioritizes borrower onboarding, digital document collection, and quick credit eligibility workflows. By connecting these modern user frontends to standard databases, they help lenders convert more applicants in real time.

Therefore, they are an excellent fit for firms looking to attract digital-native borrowers who demand fast mobile interactions.

3. Backbase: Best for a Bank-Wide “Control Plane”

Backbase provides an enterprise-wide engagement banking operating system that unifies disconnected banking systems into a single user interface.

The software functions as a translation layer that sits comfortably above legacy core banking engines, customer relationship management (CRM) platforms, and origination systems.

- What they do: They combine all employee screens and customer web channels onto a single semantic data infrastructure.

- Why they’re good: Employees no longer have to log into multiple separate systems to review a single loan application. It creates a centralized runtime where digital agents and human staff pull from the exact same customer file.

- The Catch: Implementing this software is a major strategic decision that reshapes how your entire bank operates, requiring long-term commitment.

The software utilizes a specialized security tool called a Decision Token. This tool automatically creates an unchangeable digital log showing exactly which policy rule, evidence file, or employee authorized an action.

As a result, your risk management teams gain total visibility over both automated and human workflows without slowing down daily lending production.

4. UiPath: Best for Automating Old Systems

UiPath delivers an enterprise process orchestration framework that helps banks automate tasks without replacing their current software platforms.

The technology acts as a digital workspace overlay that interacts with systems through standard APIs and direct user-interface emulation.

- What they do: Their software bots log into legacy systems like Encompass or nCino to copy data, calculate financial ratios, and sort incoming files.

- Why they’re good: You keep your existing software investments completely intact. The automation handles the repetitive data entry work so your human staff can focus on evaluating complex credit files.

- The Catch: UiPath provides the execution framework but does not supply built-in credit intelligence. Your institution must still author and manage all credit policies.

The platform excels at managing workflows that involve a mix of human staff, legacy software bots, and modern conversational tools. For example, a bot can automatically ingest an application file, run debt-to-income calculations, and route the case directly to an underwriter if an exception occurs.

This flexible setup allows banks to increase processing speed without undergoing a risky core system replacement.

5. Taktile: Best for Business Lending

Taktile offers a dedicated low-code credit decisioning platform optimized for small-to-medium businesses (SMB) and complex commercial underwriting workflows. The platform is built so that credit risk managers can adjust lending rules directly without needing a software engineer to write code.

- What they do: Their system automatically reads business financial statements, calculates corporate health metrics, and runs corporate identity checks.

- Why they’re good: It simplifies the process of evaluating a business by pulling real-time data from open-banking networks and corporate tax registries.

- The Catch: The software is highly optimized for onboarding and credit decisioning, meaning it does not handle long-term loan servicing or collection tasks.

The platform provides a highly visual workspace where risk teams can drag and drop new criteria into their credit models.

For instance, you can easily set up an automated rule that instantly approves an SMB loan if its real-time cash flow matches your safety criteria. This layout reduces the time required to update lending guidelines from months to a few hours.

6. Abrigo: Best for Community Banks

Abrigo creates lending, risk management, and financial crime compliance software engineered specifically for community financial institutions.

The platform focuses heavily on maintaining regulatory safety while preserving the personal relationships that local banks rely on.

- What they do: They manage the full lifespan of a loan, from the initial pipeline opportunity through formal underwriting, closing, and portfolio administration.

- Why they’re good: The software includes pre-packaged compliance guardrails tailored to regional banking regulations, ensuring your files stay audit-ready.

- The Catch: Their brand-new agentic platform experience is in its early rollout phase for 2026, meaning buyers should request a live production demonstration.

The platform aims to reduce manual data entry across the lifecycle of a loan by utilizing continuous information validation checks. By checking incoming property values and credit files against active profiles, the software keeps the loan moving forward safely.

Consequently, local credit teams can spend less time filling out compliance forms and more time serving local borrowers.

7. Built: Best for Construction Loans

Built delivers a niche vertical lending platform designed to automate the complex process of construction finance and real estate draw management. The software focuses entirely on mitigating physical asset risks during active building projects.

- What they do: The platform automatically reads construction draw requests, cross-references builder invoices, and checks local inspection data.

- Why they’re good: It ensures that money is only disbursed to contractors when construction milestones are physically verified, preventing overfunding errors.

- The Catch: This software is highly specialized for real estate finance, making it completely unsuitable for retail credit cards or auto loans.

The software architecture includes a specialized draw agent that ingests unstructured budget sheets and matches them against signed lien waivers. This automated review process protects the lender from funding projects that have legal or structural issues.

Because it handles the heavy lifting of document matching, real estate risk teams can manage much larger construction portfolios with fewer administrative errors.

8. EnFi: Best for Commercial Credit Analysis

EnFi operates an AI-native commercial credit platform that serves as a digital assistant workforce for institutional and corporate lenders.

The software is engineered to handle the highly variable and unstructured documentation common in corporate finance.

- What they do: Their software agents read through massive corporate financial packages, spread financial data, and highlight hidden asset risks.

- Why they’re good: It cuts down the hours commercial credit analysts spend reading documents by automatically generating structured credit memos.

- The Catch: They are a growing specialist firm focused entirely on large corporate credit, so they do not offer consumer retail lending tools.

The platform uses a multi-agent framework where distinct digital workers focus on specific parts of a commercial file. One agent might parse tax histories, while another analyzes overall industry trends to flag emerging market risks.

This specialized layout allows regional banks and private equity funds to evaluate complex commercial deals with institutional-grade speed.

9. Jifiti: Best for “Embedded” Lending

Jifiti provides white-labeled embedded finance infrastructure that lets traditional banks place their loan options directly inside a retail merchant’s checkout page. The platform focuses on point-of-sale integration and smooth transaction routing.

- What they do: They act as the secure data connection between a bank’s credit engine and a retailer’s point-of-sale shopping cart.

- Why they’re good: They make it simple to launch “Buy Now, Pay Later” or business procurement programs under your own brand across global retail networks.

- The Catch: You must still carefully configure your bank’s compliance rules, as Jifiti manages the retail connection rather than the underlying credit policy.

The platform uses standardized communication protocols to ensure that consumer shopping carts can speak to bank ledgers instantly. When a shopper requests financing, the system routes the data, secures the approval, and handles the merchant settlement within seconds.

This capability allows traditional lenders to compete directly with modern fintech firms right at the point of sale.

10. Zest AI: Best for Credit Scoring

Zest AI specializes in machine-learning credit underwriting software that helps lenders construct more accurate and inclusive risk models.

The platform replaces rigid legacy credit scorecards with advanced, explainable mathematical modeling.

- What they do: They analyze your historical lending data to build a custom credit scoring model tailored to your specific borrower base.

- Why they’re good: Their advanced math helps lenders safely approve thin-file borrowers while lowering overall portfolio default rates.

- The Catch: This is strictly a credit scoring and risk modeling engine, not a complete multi-agent loan origination or servicing workspace.

The platform places an absolute focus on fair-lending laws and model explainability. Every single automated approval or denial comes with mathematically sound reason codes that satisfy strict regulatory expectations.

Therefore, by running automated checks against disparate impact, the software helps consumer lenders expand their credit operations safely and equitably.

No single company on this list represents a universal market leader because these products solve completely different infrastructure problems. A bank-wide control plane, an automated process overlay, a specialized construction tool, and a custom development engagement are not interchangeable technology purchases.

Therefore, your choice must align perfectly with the specific credit product you offer and the level of software ownership your business requires.

Which Agentic Lending Platforms Fit Each Lending Segment?

Platform fit depends more on the lending product than on the vendor’s general AI capabilities. Consumer lending prioritizes high-volume decisioning and fraud controls.

Commercial lending requires document interpretation and analyst workflows. Mortgage platforms need disclosure, eligibility, property, and closing integrations.

Construction lenders require draw and collateral workflows. Therefore, aligning specific software layouts with asset classes prevents severe deployment friction.

1. Consumer Lending, Personal Loans, BNPL, and Credit Cards

High-volume credit products require split-second fraud verification and dynamic risk pricing infrastructure. When selecting the best autonomous consumer lending platform vendors, institutions must balance instant execution with strict model safety.

- Taktile: Optimizes configurable credit workflows by letting risk managers alter decision rules instantly without writing new code.

- Zest AI: Deploys highly tailorable machine-learning underwriting models that safely increase approval rates for thin-file applicants.

- Jifiti: Delivers white-labeled embedded financing directly into merchant point-of-sale systems using standard data routing.

- Backbase: Provides the broader bank orchestration plane needed to connect these front-end consumer applications to legacy bank accounts.

- Intellivon: Designs proprietary multi-product platforms for enterprises that need completely custom automated decisioning logic without software licensing overhead.

For a deeper breakdown of building specialized, secure consumer workflows, see our guide on How to Develop Agentic Loan Decisioning Platforms.

2. Mortgage and HELOC Origination

Residential real estate lending demands deep document verification and rigid adherence to changing federal consumer laws. To rank among the top agentic mortgage lending platform companies, software must securely bridge complex property evaluation databases with core bank ledgers.

- UiPath: Automates workflow orchestration around existing mortgage LOS products, interacting smoothly with software like Encompass or Empower to cut data entry time.

- Intellivon: Engineers fully custom mortgage workflows and advanced model governance frameworks, ensuring that automated verification processes create crystal-clear regulatory evidence.

- Backbase: Unifies bank-wide origination coordination to ensure that retail borrowers and underwriting staff pull data from identical loan context profiles.

- Built: Operates as a highly targeted solution only where construction-to-permanent loan administration or specialized builder draw management is required.

3. Small Business, SBA, and Equipment Finance

Commercial business lending features highly unstructured documentation, including variable tax records and specialized equipment invoices. Consequently, selecting the top agentic small business lending platform companies requires tools that can interpret irregular commercial profiles.

- Taktile: Builds responsive SMB underwriting agents that extract financial statement data and verify corporate entity records.

- EnFi: Deploys automated credit analyst agents that parse balance sheets and generate comprehensive initial credit summaries.

- Abrigo: Focuses heavily on relationship and community banking workflows, helping regional lenders manage their small business portfolios safely.

- Jifiti: Facilitates embedded B2B financing options directly within wholesale checkout networks and corporate procurement channels.

- Custom Platforms: Allow institutions to build unique cash-flow underwriting engines that score businesses based on real-time transaction data rather than outdated tax files.

4. Commercial, CRE, and Construction Lending

Large-scale corporate and commercial real estate (CRE) finance involves huge capital amounts and deeply customized credit agreements. These intricate financial structures require role-based digital agents that can coordinate multiple validation steps over long deal lifecycles.

- EnFi: Automates intensive credit analyst workflows, reading hundreds of pages of corporate documentation to summarize latent asset risks.

- Built: Leads the vertical field in construction finance, matching draw requests against physical inspection data and signed contractor lien waivers.

- Abrigo: Supplies deep pipeline tracking and risk administration software designed specifically for commercial bank lending operations.

- Backbase: Coordinates operations across fragmented bank systems to maintain a single, clean view of corporate relationship exposure.

- Intellivon: Constructs complex multi-agent underwriting and portfolio monitoring platforms, allowing commercial credit teams to completely own their underlying software intellectual property.

5. Adjacent Vendors That Belong in the Stack, Not the Ranking

Evaluating the modern fintech market requires drawing an honest line between completely autonomous operating environments and specialized software components. Many valuable industry tools serve as critical building blocks within your technical stack, but they should not automatically be classified as complete agentic platforms.

- LOS and Digital Incumbents: Platforms like nCino, Blend, Amount, MeridianLink, Temenos, Finastra, FIS, Fiserv, Jack Henry, and ICE Mortgage Technology act as essential systems of record rather than autonomous agent coordinators.

- Decisioning and Risk: Providers such as Provenir, Scienaptic, Upstart, Pagaya, and Zest AI serve as specialized scoring intelligence layers that sit within a larger workflow engine.

- Document, Fraud, and Data: Utilities like Ocrolus, Inscribe, Plaid, Finicity, and traditional credit bureaus function as data pipes that feed essential customer files into your system.

- Servicing and Collections: Systems including LoanPro, Peach Finance, Sagent, and standard servicing platforms handle backend payment ledgers after the loan has closed.

These components work best when organized by a central orchestration engine. Understanding how these pieces connect helps technical decision-makers design a clear implementation blueprint.

The 7 Layer Enterprise Agentic Lending Platform Architecture

A production agentic lending platform needs seven separable layers: user experience, identity and data ingestion, orchestration, policy and decisioning, AI models and tools, enterprise execution, and governance.

Therefore, separating these layers prevents an LLM from becoming the credit policy engine, system of record, and compliance authority at the same time.

Architectural Blueprint Matrix

To help engineering teams map these dependencies, the table below breaks down the technical responsibilities of each individual layer within the system stack.

| Layer | Primary Function | Core Components Included | Technical Design Pattern |

| 1. Experience Layer | Human-in-the-loop interfaces | Borrower portals, broker portals, underwriter workspaces, compliance queues. | Single-page apps connecting to orchestration APIs. |

| 2. Foundation Layer | Identity, data, and document ingestion | KYC checks, bureau reports, open-banking pipes, document extraction APIs. | Asynchronous ingestion queues with data extraction. |

| 3. Orchestration Layer | Multi-agent state and workflow routing | Workflow graphs, persistent state machines, tool permissions, human interrupts. | State machine patterns separating logic from execution. |

| 4. Decision Control | Deterministic credit policy and rules | Eligibility rules, credit policies, pricing boundaries, adverse-action maps. | Strictly outside the LLM using executable rules engines. |

| 5. AI and Tool Layer | Specialized models and calculators | Default models, cash-flow scorers, LLMs, policy RAG, calculation tools. | Microservices run isolated analytical tasks. |

| 6. Integration Layer | Enterprise system execution | Core banking, legacy LOS, CRM, e-signature, disbursement networks. | Secure API gateways with circuit breakers. |

| 7. Governance Layer | AgentOps, audit, and compliance | Model registries, prompt versioning, decision evidence logs, drift alerts. | Immutable event ledgers for compliance record-keeping. |

Key Architectural Takeaways

- Policy isolation is mandatory: Keeping deterministic credit criteria entirely outside of large language models prevents unpredictable decision-making and ensures strict compliance with fair-lending laws.

- Auditability drives long-term value: A microservices layout allows independent logging of data inputs, agent tool selections, and final system executions, creating a transparent audit trail for regulators.

The platform architecture must explicitly assign core operational authority to the immutable policy and governance layers rather than relying on the conversational fluency of a language model. Therefore, the next step in system design requires examining how to select and deploy the correct class of machine learning models within this architecture.

For a deeper structural review of how to decouple these complex layers using clean cloud infrastructure, see our comprehensive blueprint on Custom Agentic Lending Platform Architecture.

Compliance Controls Every Agentic Lending Platform Must Prove

An agentic lending platform must prove why a decision occurred, which policy applied, which data and model versions were used, what the agent executed, and who approved any exception.

Logging the final outcome alone is insufficient because regulators and internal reviewers need the complete decision and action path.

1. ECOA and Regulation B Adverse-Action Reasons

The CFPB states that ECOA and Regulation B requirements apply regardless of model complexity. Therefore, a creditor cannot use a technology that prevents it from identifying accurate reasons for adverse action.

Your platform must map model outputs directly to clear, ranked reason codes and prevent generic or approximate explanations from being generated.

2. Fair-Lending Testing and FCRA Data Controls

Lenders must run continuous protected-class outcome testing and enforce proxy methodology governance to ensure fair pricing.

Additionally, you need clear data provenance, permissible-purpose controls, and automated dispute workflows to verify that alternative data satisfies all FCRA guidelines.

3. SR 26-2 Model Risk Management

The Federal Reserve issued SR 26-2 in 2026 to govern model inventories, change controls, and conceptual soundness. This framework officially replaced the legacy SR 11-7 agentic lending model compliance rules.

The current rules mandate risk-based monitoring and clear management oversight for all complex quantitative systems.

3. Mortgage-Specific Controls

For residential real estate, the platform architecture must explicitly automate HMDA data capture and TRID disclosure timing clocks.

Furthermore, the system must hardcode qualified mortgage calculations and ability-to-repay reviews directly into its rule layers to handle regional licensing differences.

4. Agent Action Governance

Autonomous systems require strict action permissions, versioned policies, and immutable evidence bundles to record every single tool execution.

However, human override capabilities, dual approvals for large credit limits, and emergency suspension switches must be built directly into the codebase.

For a deeper breakdown of governed financial agents, see our guide on How to Build AI Agents for Banking Compliance and AML.

How Much Does Agentic Lending Platform Development Cost?

Custom agentic lending platform development usually costs $70,000 to $300,000, depending on the number of lending products, agents, AI models, integrations, regulatory controls, user interfaces, and deployment environments included.

When planning software capital deployment, institutions must separate up-front engineering fees from ongoing operational platform expenses.

Cost by Platform Scope

To help financial technology leaders outline initial software capitalization budgets, the table below provides average pricing benchmarks based on project scope.

| Platform Scope | Cost Range | Typical Inclusions |

| Focused MVP | $70,000–$110,000 | One lending product, 2–3 agents, limited integrations, final human approval loop. |

| Production Single-Product Platform | $120,000–$210,000 | Integrated loan origination, autonomous underwriting, compliance logging, and core database pipes. |

| Multi-Product Enterprise Platform | $220,000–$300,000 | Multiple asset classes, complex legacy integrations, advanced MLOps infrastructure, private deployment. |

1. Development Phase Breakdown

Constructing a tailored system requires distributing the total engineering budget across specific milestones. At the same time, the final total aligns directly with the overall $70,000–$300,000 project band:

- Discovery and compliance mapping: $5,000–$15,000

- Architecture and data foundation: $10,000–$30,000

- Orchestration and agent development: $25,000–$90,000

- AI models and decision controls: $20,000–$65,000

- Integrations, security, and validation: $15,000–$70,000

- Deployment and production monitoring: $5,000–$30,000

Ongoing Operating and Maintenance Costs

Launching the software platform initiates the operational maintenance cycle. Lenders should budget roughly 15%–25% of the initial build cost annually to cover continuous system optimization.

This recurring budget funds essential cloud infrastructure, large language model inference volume, strict policy rule updates, and unexpected third-party vendor API changes.

Furthermore, regular security penetration tests, independent model validation updates, and automated algorithmic bias reviews are required to preserve bank compliance standings.

How to Implement an Agentic Lending Platform Without a Rip-and-Replace

A focused agentic lending platform pilot usually takes 10–16 weeks. A production single-product rollout takes five to eight months, while a multi-product enterprise programme can take eight to twelve months.

The safest path starts with one portfolio, one decision boundary, and one measurable operational bottleneck.

Phase 1 — Define the Portfolio and Autonomy Boundary

First, we isolate a specific loan product, borrower population, geography, and acquisition channel to test the automation safely. During this phase, we establish clear decision types, human review escalation thresholds, and strictly prohibited agent actions.

How we build it: We hard-code an immutable permission matrix into the orchestration layer. This code ensures the software agent cannot independently authorize high-risk exceptions or modify interest rates.

Phase 2 — Map Policy, Data, and System Dependencies

Next, we document your exact credit policies, permitted lending exceptions, and regulatory adverse-action reason codes. We then map all active data sources, legacy risk models, and target Loan Origination System (LOS) landing states.

How we build it: We construct dedicated data connectors that link your existing systems of record to our secure environment without disturbing your day-to-day transaction ledgers.

Phase 3 — Build One Complete Agent Chain

Rather than launching many disconnected agents, we assemble one single, highly focused workflow loop. Popular starting chains include automated application completion, document verification, or commercial credit memo creation.

How we build it: We code a structured multi-agent workflow where an intake agent passes clean text directly to a verification agent, creating a strict linear chain of custody.

Phase 4 — Run in Shadow and Assist Modes

Before going live, the agent chain runs silently in the background on real incoming applications. We track processing times, false escalations, tool failures, and cost differences per application file.

How we build it: We deploy a side-by-side dashboard where human underwriters review the agent’s calculations and recommendations before any data is written back to production.

Phase 5 — Release Bounded Execution

Once shadow testing matches your accuracy targets, we grant the platform bounded execution authority. The system automatically handles low-risk tasks with clear reversal procedures, such as chasing missing bank statements.

How we build it: We lock final loan approvals, pricing exceptions, and adverse declines behind mandatory manual sign-offs. The agent prepares the file, but a human operator clicks the final button.

Phase 6 — Expand by Decision Type

Finally, we scale the platform by adding new credit products or advanced autonomous roles. This expansion occurs gradually to preserve institutional safety.

How we build it: We duplicate the verified microservices stack for the next asset class, adjusting the core rule parameters while retaining the validated governance framework.

Build an Enterprise Agentic Lending Platform With Intellivon

Build an enterprise agentic lending platform with Intellivon when standard lending products cannot support your credit policy, agent boundaries, model governance, integrations, or deployment requirements. Here is why:

- Architecture-first development: Engineering multi-agent orchestration, workflow state, isolated policy services, immutable evidence storage, secure APIs, and event-driven execution loops.

- Lending AI: Custom credit-risk models, advanced cash-flow underwriting, document intelligence, policy RAG, fraud detection, and automated credit memo generation.

- Compliance controls: Hardcoded ECOA reason mapping, fair-lending testing, SR 26-2 model governance, traceably logged audit evidence, and mandatory human approval checks.

- Enterprise integration: Safe connections to legacy LOS, core banking engines, credit bureaus, open banking, CRM, KYC/AML platforms, servicing pipelines, and document systems.

- Production operations: Comprehensive MLOps, AgentOps, system observability, instant rollback, penetration security testing, drift monitoring, and cost controls.

- Delivery depth: Backed by more than 500,000 engineering hours, an elite team of ex-MAANG talent, and a proven track record of constructing regulated AI and fintech systems.

Intellivon stands out because we provide complete technology ownership without recurring subscription fees or software vendor lock-ins.

With over 11 years of specialized domain expertise and 500+ successful enterprise deployments, we translate complex credit guidelines into practical, audit-ready code built to work in production.

Conclusion

Licensing off-the-shelf software often locks your bank into rigid vendor features and unpredictable monthly fees. When you build a custom agentic lending platform with a dedicated engineering partner, you own your entire system, all the way from the core code to the credit risk models and audit trails.

This direct approach allows your team to safely automate heavy loan workflows, cut operational costs, and satisfy strict compliance rules without forcing a risky replacement of your current legacy databases.

FAQs

Q1. Which Are the Best Agentic AI Lending Platform Companies in the USA?

A1. There is no universal winner. Consequently, Intellivon and Idea Usher suit custom development, whereas Backbase handles bank-wide orchestration. Meanwhile, UiPath serves lenders, keeping their current LOS. Finally, Taktile and Zest AI optimize credit decisioning, while Abrigo, Built, and EnFi target specific community, real estate, or commercial segments.

Q2. How Long Does Agentic Lending Platform Implementation Take?

A2. A controlled pilot normally takes 10–16 weeks. Furthermore, moving a single product to full production deployment requires 5 to 8 months. Eventually, multi-product enterprise rollouts take eight to twelve months. Therefore, you should validate outcomes in shadow mode before releasing bounded production authority.

Q3. Can an Agentic Lending Platform Replace an Existing LOS?

A3. Usually, it should not replace the LOS during the first release. Instead, the agentic layer coordinates documents, models, and workflows while the LOS remains the system of record. True replacement becomes reasonable only when legacy architecture completely blocks API connectivity, product configurations, or reliable real-time data retrieval.

Q4. Is Custom Development Better Than Licensing an Agentic Lending Vendor?

A4. Choose custom development when your unique credit policy or workflow design creates a true strategic advantage. Conversely, off-the-shelf SaaS works well when target workflows are standard and setup speed matters most. Alternatively, a hybrid layout allows you to use your working LOS while building proprietary orchestration logic.

To Sum It Up

- A credit model, chatbot, or document extractor does not become an agentic lending platform until it can coordinate controlled actions across a complete workflow.

- The strongest vendor depends on whether the lender needs custom infrastructure, a bank-wide control plane, an LOS overlay, or a specialist underwriting capability.

- SR 11-7 was superseded by SR 26-2 in April 2026, so current vendor evaluations must use the revised model-risk framework.

- Full lending autonomy is weaker than bounded autonomy when decisions involve incomplete evidence, policy exceptions, or adverse-action obligations.

- Custom agentic lending platform development should remain within $70,000–$300,000 for the scope defined in this post.