Key Takeaways:

- Insurance claims automation agents require a multi-agent architecture combining rules, LLMs, document AI, and predictive ML.

- Graph analytics and computer vision support fraud detection while human approval governs all consequential claim decisions.

- Guidewire, Duck Creek, Majesco, ACORD, payment, fraud, and evidence integrations are core production requirements.

- NAIC, state DOI, HIPAA, ERISA, and audit requirements are non-negotiable compliance architecture considerations.

- How Intellivon builds claims automation agents where authority expands by claim type, value, confidence, and reversibility.

Insurance claims travel through more than ten distinct stages from first notice of loss to payment. Agentic claims processing starts with a triage layer that routes each claim to the right agent automatically. That layer scores each claim for complexity, fraud risk, and line of business before routing it. From there, separate agents handle FNOL intake, coverage verification, document processing, and settlement.

The triage layer determines the straight-through processing rate, not the individual claim agents themselves. Without it, every claim goes through the same processing path regardless of complexity or fraud risk. Currently, only 7% of claims pass through complete straight-through processing without human involvement. At the same time, AI-powered triage consequently pushes that rate to 70-90% for straightforward claims within the same portfolio.

Intellivon builds claims automation agents for carriers and TPAs where compliance and cycle time both matter. The approach therefore always starts with triage architecture before individual claim processing agents are built. Accordingly, this blog covers triage design, fraud detection, document processing, settlement automation, and regulatory compliance.

What are Insurance Claims Automation Agents?

Insurance claims automation agents are self-directed software systems that handle an insurance claim from start to finish. Instead of relying on manual data entry, these smart agents use goal-oriented language models and specific software tools to read documents, check policy rules, and spot fraud patterns automatically.

Consequently, they speed up payouts while keeping data secure. Finally, they work independently within strict safety boundaries and immediately hand off complex issues to human adjusters when necessary.

What Agentic Claims Processing Automates

Agentic claims processing uses goal-directed software agents to interpret claim information, select tools, complete multi-step work, communicate with other agents, and escalate decisions under predefined authority.

It extends beyond robotic process automation (RPA) because the workflow does not require every document variation and exception path to be coded in advance.

1. Rules-Based Automation, Copilots, and Claims Agents Are Different

| Capability | RPA | Predictive AI | Claims Copilot | Agentic Claims Platform |

| Follows fixed steps | Yes | No | Partly | Partly |

| Interprets unstructured documents | Limited | Model-specific | Yes | Yes |

| Selects tools dynamically | No | No | Limited | Yes |

| Maintains workflow state | Limited | No | User-dependent | Yes |

| Executes approved actions | Yes | Usually no | Limited | Yes |

| Escalates based on risk | Fixed rules | Model score | User-driven | Policy-driven |

2. Bounded Autonomy and Exception Handling

- Bounded Autonomy: Agents independently execute low-risk tasks like collecting missing evidence, validating forms, looking up policy language, and routing work. However, they lack the authority to deny coverage, accuse claimants of fraud, or alter large reserves without human approval.

- Exception Handling: The system creates the highest value when documents are incomplete, data conflicts across sources, or new evidence changes the handling strategy. Consequently, specialized tools like a medical bill review AI agent or a contractor assignment AI agent manage data variations dynamically.

Claims agents should manage variability, not remove controls. Therefore, the first design decision is choosing workflows where autonomy produces measurable value without creating disproportionate claim risk.

Which Claims Workflows Should Insurers Automate First?

Insurers should begin with high-volume claims work that has clear evidence requirements, measurable outcomes, reversible actions, and established escalation paths.

Starting with the most consequential adjudication decision creates unnecessary regulatory, financial, and customer risk.

1. High-Yield Automation Targets

- Omnichannel Intake: An agentic first notice of loss automation platform ingests data across web, email, SMS, and voice, capturing critical data while running immediate duplicate-claim detection.

- Document Validation: Specialized NLP claims document classification tools extract data from ACORD forms, police reports, and medical bills, instantly flagging missing pages or suspicious edits.

- Triage and Assignment: The system uses AI claims triage and routing automation to score probable severity and direct complex claims to senior adjusters within minutes.

- Coverage Verification: A dedicated claims coverage verification AI agent checks limits, deductibles, and exclusions, providing human teams with auditable policy terms and AI extraction agent citations.

- Fraud Development: A predictive claims fraud scoring AI model initiates a human review for anomalies like phantom providers without making automatic, unverified misconduct accusations.

2. Financial and Operational Progression

- Evidence Summarization: The agent condenses thousands of pages of medical records and AI claims processing data into structured summaries.

- Damage & Medical Review: A specialized medical bill review AI agent cross-checks line items against regional cost baselines.

- Reserve & Settlement Range: A case reserve AI recommendation engine calculates financial exposures and proposes approved settlement boundaries.

- Payment & Subrogation: The platform triggers a claims payment AI agent automation workflow and opens a subrogation AI agent recovery file.

The best first use case is not the easiest workflow, but the one with enough volume to prove value and enough control to limit downside. Therefore, prioritizing bounded intake and validation workflows protects the bottom line from processing errors.

Design a Multi-Agent Claims Team

A production claims platform should separate responsibilities across agents with narrow permissions. One general-purpose agent creates weak controls because the same model can collect evidence, interpret coverage, recommend settlement, and trigger payment without meaningful separation of duties.

Consequently, dividing tasks among specialized micro-agents ensures operational safety, higher accuracy, and clean audit logs across the claims lifecycle.

Ultimately, a modular architecture limits risk by restricting what each individual component can execute.

The Specialist Claims Agent Network

- Claims Orchestrator Agent: This central engine opens and maintains the overall claim workflow state. It dynamically assigns tasks to specialist agents, tracks internal dependencies, resolves conflicts, and enforces mandatory human escalation policies when risk thresholds are breached.

- FNOL and Claims Intake Agent: This module handles conversational data capture across digital portals and call centers. It performs immediate policyholder identity checks, flags duplicate submissions, requests missing baseline information, and runs preliminary urgency classifications.

- Document Intelligence Agent: Operating as a claims document AI processing automation layer, this agent handles OCR and document classification. It extracts text line items from complex forms, summarizes medical and legal records, and flags potential visual or textual alterations.

- Coverage Verification Agent: This specialized component acts as a coverage eligibility AI agent to pull policy versions and endorsements. It compares incident facts directly against policy language, identifies gaps, and routes major coverage ambiguities to legal counsel.

- Fraud and Investigation Agent: This engine functions as an autonomous agentic insurance fraud detection platform. It runs real-time network link analysis, queries external industry databases, checks social media footprints, and prepares structured investigation plans for the SIU.

- Damage or Medical Review Agent: This node uses computer vision claims damage assessment models to analyze vehicle or property photos. Concurrently, it runs ICD-10 AI claims coding automation engines to verify medical bill necessity and bill lines.

- Reserve and Settlement Agent: Built on top of a claims reserving AI model development engine, this agent recommends case reserves. It calculates approved settlement ranges, flags hidden severity changes, and routes financial recommendations based on corporate authority limits.

- Communication, Payment, and Recovery Agents: This group manages outbound text notifications and coordinates vendor repairs. Additionally, it configures secure payment processing pipelines and identifies third-party subrogation recovery opportunities.

Blueprint for Autonomous Agent Contracts

To maintain absolute system control, developers must govern every micro-agent via a strict, declarative agent contract.

This architectural framework prevents model drift and ensures that no agent exceeds its operational boundaries.

- Define Objective & Scope: Establish the singular business goal of the agent and restrict its memory access to context-specific variables.

- Lock Schemas & Permitted Tools: Hardcode the exact JSON input/output schemas and specify the precise external APIs or database tools the agent can invoke.

- Set Authority & Confidence Thresholds: Define the maximum financial limit the agent can process and establish mathematical confidence scores required for autonomous action.

- Enforce Prohibitions & Escalation Paths: Explicitly detail prohibited actions and map out direct human-in-the-loop escalation frameworks for anomalies.

Enforcing these boundaries means that agents operate strictly as deterministic utilities within your insurance infrastructure. Therefore, defining explicit agent contracts reduces compliance exposure while accelerating your overall software delivery timeline.

For a deeper breakdown of multi-agent workflow orchestration, see Intellivon’s guide on How to Build Agentic AI for Revenue Cycle Management.

Build the Enterprise Agentic Claims Processing Architecture

The architecture should separate orchestration, claims knowledge, probabilistic models, deterministic rules, business-system tools, human approval, and audit evidence.

This prevents the language model from becoming the source of truth for coverage, payment, compliance, or financial calculations. Consequently, dividing these layers protects systemic data integrity while keeping every automated decision fully auditable.

System Architecture Layer Comparison

| Architectural Layer | Core Technical Component | Primary Operational Role |

| Layer 1: Intake & Ingestion | Kafka event streams, webhooks, telematics data streams | Gathers raw evidence across mobile, voice, email, and external IoT feeds. |

| Layer 2: Canonical Data Model | Unified master data schemas, entity resolution engines | Reconciles conflicting records and creates stable identifiers for tracking. |

| Layer 3: Agent Orchestration | LangGraph orchestration engines, distributed event queues | Manages multi-agent communication, long-running state paths, and human interrupts. |

| Layer 4: Claims Intelligence | Multi-modal LLMs, computer vision engines, predictive models | Processes document text, scores property damage, and calculates reserves. |

| Layer 5: Integration Gateway | Secure API gateways, typed JSON tools, database adapters | Connects agents securely to core platforms like Guidewire and payment rails. |

| Layer 6: Human Workbench | Administrative user interfaces, explainable AI explanations | Presents recommendations, policy citations, and manual override controls. |

| Layer 7: Observability & Governance | Immutable audit logs, MLOps model evaluation tracking | Captures all system states, prompt versions, and human approval paths. |

Separating operational layers ensures your core business systems remain isolated from volatile language model outputs. Therefore, this structured approach eliminates the risk of incorrect claims payouts while keeping the entire process transparent.

This 7-layer design turns unpredictable AI experiments into a stable, carrier-grade software platform. By managing each step independently, your IT organization can easily push updates without breaking active workflows.

Select the Right Models for Each Claims Decision

An insurance claims platform needs several model families because document extraction, fraud detection, coverage retrieval, damage assessment, and reserving are different technical problems. Using one LLM for every task increases hallucination risk, cost, latency, and validation complexity.

Ultimately, pairing specific tasks with specialized models ensures high precision and processing safety.

1. Specialized Model Deployments

- Document Intelligence & NLP: Specialized OCR engines process ACORD forms, bills, and handwritten notes, measuring field-level precision. Meanwhile, LLMs coupled with RAG handle complex policy lookup and medical records AI claims processing text, demanding exact documentation citations.

- Classification & Vision: Gradient-boosted trees execute claims complexity classification, predicting litigation likelihood and driving routing rules. Simultaneously, computer vision engines evaluate drone or mobile media to verify damage type and scan for image reuse fraud.

- Graph, Predictive, & Fixed Rules: Predictive models use historical payments to estimate reserves, while deterministic rules engines handle non-negotiable logic like deductibles and authority limits outside the LLM.

2. Model Selection Framework

| Task | Recommended Model Family | Primary Output | Validation Metric | Required Human Reviewer |

| Doc Extraction | Layout-aware Transformer | Structured JSON data | Field-level Recall | Ops Data Clerk |

| Policy Analysis | Fine-tuned LLM + RAG | Policy rule citations | Hallucination Rate | Coverage Counsel |

| Triage & Routing | LightGBM Classifier | Severity/Complexity score | F1-Score | Claims Manager |

| Fraud Spotting | Graph Neural Network (GNN) | Risk network graph | ROC-AUC | SIU Investigator |

| Damage Valuation | Convolutional Neural Net | Component repairability | Mean Absolute Error | Licensed Appraiser |

| Reserves Setup | Linear/Tree Ensemble | Recommended case reserve | Mean Absolute Error | Actuary / Adjuster |

Deploying the correct model for each specific task keeps your production environment safe from runtime errors. Therefore, combining probabilistic models with rigid, deterministic rules ensures both flexibility and strict compliance.

Integrate Claims Agents With Core Systems

Integration usually creates more development effort than building the conversational agent itself. The platform must retrieve current claim and policy data, call external evidence services, and write approved actions back without creating duplicate claims, payments, reserves, or correspondence.

Ultimately, secure pipelines prevent language models from corrupting systems of record.

Core Ecosystem and Data Source Management

- Core Systems: Platforms connect to Guidewire ClaimCenter, Duck Creek, and Majesco via REST/SOAP APIs, webhooks, or message queues. Guidewire embeds AI for summary and coverage tasks, while Duck Creek offers agentic FNOL applications.

- Data Formats & Fraud Verification: The canonical data model maps schemas directly to ACORD P&C standards across XML and JSON. To detect network fraud, the agent runs real-time queries against Verisk, ISO ClaimSearch, and NICB databases.

- Estimating & Health Stacks: Integrations with CCC Intelligent Solutions, Mitchell, and Solera supply property damage repair metrics. For health portfolios, the system ingests HIPAA-compliant EDI 837/835 streams, FHIR APIs, and ICD-10 clinical coding structures.

Enforcing these strict system barriers ensures that probabilistic AI agents interact safely with rigid enterprise record layers. Therefore, isolating core logic minimizes processing defects while preserving standard carrier transaction metrics.

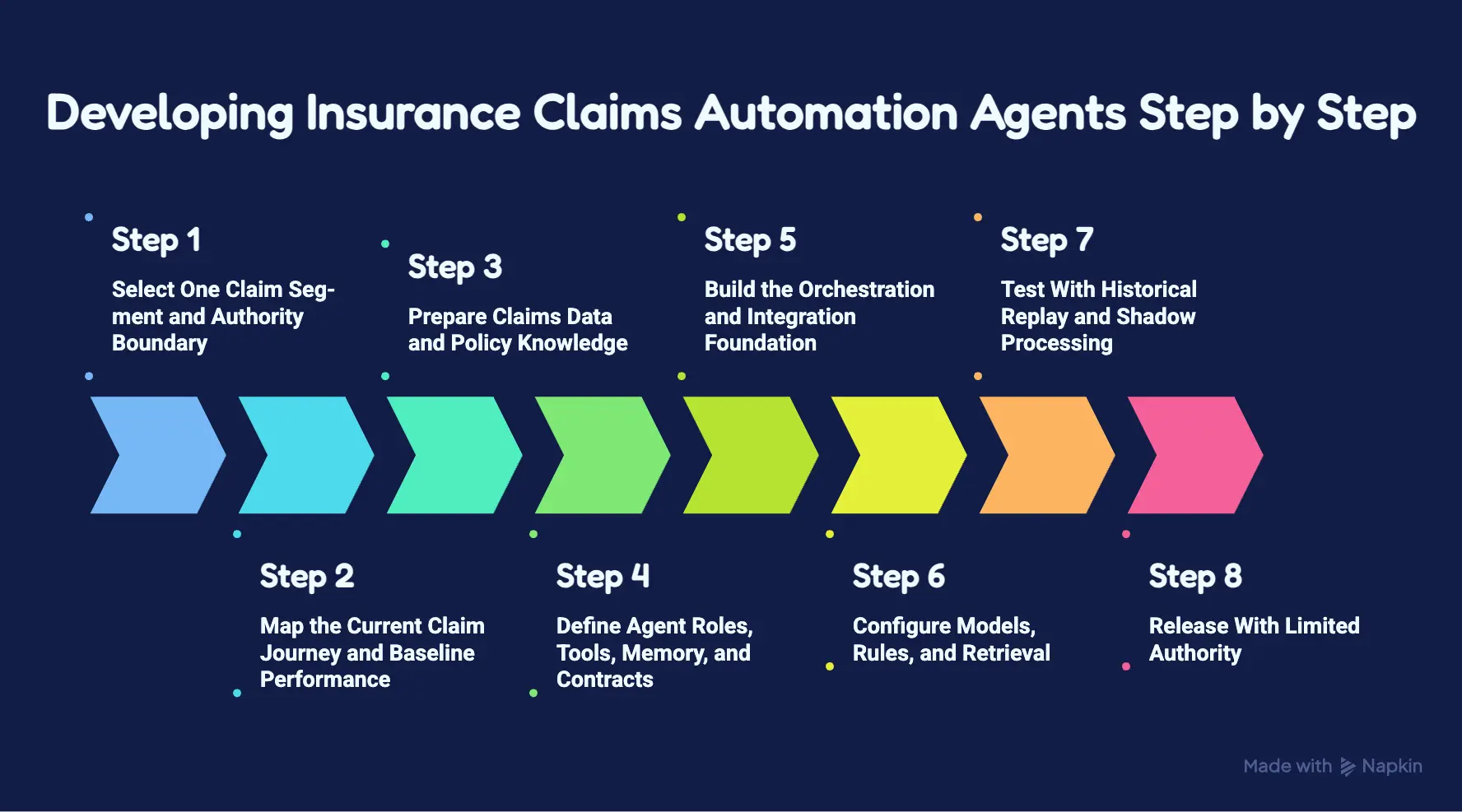

How to Develop Insurance Claims Automation Agents Step by Step

Building carrier-grade agentic claims processing platforms requires a structured, multi-phase rollout plan. Transitioning from basic scripts to self-directed micro-agents demands clear boundaries, metric baselines, isolated testing, and strict integration controls.

For a deeper breakdown of modular software engineering, see our guide on How Do Banks Use Agentic AI for AML Compliance Automation.

Ultimately, executing these steps in sequence protects production systems of record while capturing deep operational value.

Step 1 — Select One Claim Segment and Authority Boundary

To build a secure foundation, engineering leaders must isolate a single claim segment with explicit financial boundaries. Attempting to automate every product line simultaneously increases logic complexity and technical failure rates.

Consequently, selecting a tightly bound line helps teams validate agent performance safely.

- Segment Boundaries: Define the insurance line, claim type, target jurisdictions, claim-value limit, and included digital submission channels.

- Operational Constraints: Explicitly map all excluded claim states, permitted tool actions, and mandatory human review checkpoints.

- Target Artifact: A formalized Scope and Boundary Specification document defining exact API routing gates and dollar limits.

- Intellivon Approach: At Intellivon, we configure clear programmatic guardrails that instantly isolate edge cases, restricting initial agent authority to low-risk lines like low-severity auto glass or travel delays.

Setting these strict operational parameters prevents model sprawl and ensures the core workflow remains highly predictable. Therefore, this containment strategy prepares your technical environment for baseline metrics mapping.

Step 2 — Map the Current Claim Journey and Baseline Performance

Carriers must thoroughly document every manual touchpoint, data source, and processing delay inside the existing workflow journey. Without an objective operational baseline, determining whether autonomous agents are actively reducing expenses remains impossible.

As a result, gathering clear timeline data keeps optimization efforts metric-driven.

- Workflow Mapping: Record every data hand-off, queue duration, decision loop, manual copy-paste action, and regulatory compliance deadline.

- Performance Metrics: Establish clear benchmarks for cost per claim, cycle time, reopen rates, claim leakage, and straight-through processing rates.

- Target Artifact: An As-Is Workflow Blueprint cross-referenced with hard telemetry logs from core management screens.

- Intellivon Approach: We deploy passive monitoring scripts and review database audit trails to construct an unvarnished operational baseline before writing code.

Uncovering hidden process bottlenecks ensures the development team knows exactly where automation yields the highest financial return. Therefore, documenting these friction points provides a clear target for data preparation.

Step 3 — Prepare Claims Data and Policy Knowledge

Building a carrier-grade system requires organizing unstructured files, historical tables, and complex policy terms into clean data formats. Training models on unverified claims history replicates past processing biases and introduces severe hallucination risks.

Consequently, establishing a sanitized, canonical knowledge base ensures predictable inference.

- Knowledge Engineering: Construct a canonical claim schema, define a strict document taxonomy, and gather policy repositories with clear version metadata.

- Data Control: Build a golden evaluation dataset, map known fraud patterns, and apply zero-trust data access rules.

- Target Artifact: A secure, version-controlled vector and relational database layer mapped to industry data specifications.

- Intellivon Approach: We clean and structure legacy carrier data feeds, ensuring that no model accesses final claim outcomes without automated leakage checks.

Sanitizing the underlying data structures ensures that specialized models reason using verified enterprise information. Therefore, this trusted data engine provides the vocabulary necessary to frame explicit agent contracts.

Step 4 — Define Agent Roles, Tools, Memory, and Contracts

Every autonomous micro-agent must operate under a declarative system contract that specifies its exact business permissions. Allowing a single model to browse coverage, alter reserves, and execute payments introduces massive security vulnerabilities.

As a result, strict separation of duties keeps the ecosystem auditable and secure.

- Contract Definition: Specify the unique role, required inputs, typed JSON outputs, permitted tools, and confidence thresholds for every agent.

- Memory Management: Separate factual, long-term claim memory from temporary conversational context to prevent injection errors.

- Target Artifact: A declarative Agent Manifest file enforced via programmatic JSON schema validation rules.

- Intellivon Approach: We code narrow, single-purpose agent wrappers that instantly hand off processing control to human teams whenever confidence scores drop.

Isolating agent authority ensures that no model can execute unauthorized actions within the enterprise environment. Therefore, finalizing these contracts allows developers to construct the underlying graph orchestration fabric.

Step 5 — Build the Orchestration and Integration Foundation

Teams must develop the state machine graph, event queues, and core database adapters required to manage multi-agent communication. Giving language models raw, unrestricted database access can result in corrupted tables and broken transaction records.

Consequently, a typed gateway layer ensures absolute system safety.

- Infrastructure Build: Construct a LangGraph state machine, install event brokers, and build secure API adapters for Guidewire or Duck Creek.

- Core Services: Deploy dedicated human workbench interfaces, notification systems, and immutable transaction logging engines.

- Target Artifact: A containerized Orchestration Backbone running protected middleware components and role-based access tokens.

- Intellivon Approach: We design secure API gateway abstractions that strictly validate every transactional payload before committing it to systems of record.

Isolating execution environments ensures that data transfers remain resilient against service dropouts or transient token timeouts. Therefore, establishing this integration layer allows teams to configure individual intelligence components safely.

Step 6 — Configure Models, Rules, and Retrieval

Engineers must fine-tune specialized layout transformers, computer vision models, and text embedding loops to handle domain tasks.

Validating these systems in isolation often hides complex pipeline errors that only appear when components interact. As a result, checking the end-to-end processing chain prevents downstream degradation.

- Model Configuration: Deploy specialized document extraction networks, RAG semantic searches, predictive fraud models, and deterministic validation rule sets.

- System Calibration: Tune hyperparameters to maximize field-level recall while keeping latency within strict production boundaries.

- Target Artifact: A calibrated, multi-model inference pipeline integrated with hardcoded insurance compliance rules.

- Intellivon Approach: We combine flexible probabilistic models with rigid business rule engines, validating the collective system output against test suites.

Balancing language models with deterministic guardrails ensures the system satisfies both customer experience and regulatory demands. Therefore, verifying the integrated logic prepares the platform for historical replay testing.

Step 7 — Test With Historical Replay and Shadow Processing

Carriers must process thousands of closed, historical claims through the agentic pipeline without altering active production databases.

Running live, unverified models directly in production environments introduces severe financial exposure and compliance risk. Consequently, offline comparison tests help identify edge-case logic mismatches.

- Simulation & Replay: Ingest historical claim data, generate agent recommendations, and compare outputs directly against the original adjuster decisions.

- Shadow Deployment: Route real-time data copies through the agent engine while human adjusters maintain exclusive transaction execution authority.

- Target Artifact: A comprehensive Comparative Performance Report highlighting variance in reserve setup, fraud detection, and cycle times.

- Intellivon Approach: We build isolated shadow environments that mirror live inputs, helping teams track model drift before activating write-back permissions.

Uncovering subtle reasoning variations in a harmless test environment ensures the platform operates safely. Therefore, validating model accuracy under shadow conditions clears the path for a controlled production release.

Step 8 — Release With Limited Authority

The initial production deployment must be restricted to a single territory and low-value losses to monitor real-world performance. Launching an autonomous agent across all markets at once exposes the carrier to massive unexpected systemic risks.

As a result, capping initial authority boundaries protects operational stability.

- Production Launch: Activate the platform for one product in a single region, enforcing low transaction limits and mandatory human verification.

- Operations Monitoring: Track system performance hourly, establish clear incident ownership, and deploy instant global kill switches.

- Target Artifact: A live Production Monitoring Dashboard tracking automated processing rates alongside real-time human override metrics.

- Intellivon Approach: We implement tiered API access keys, ensuring that agents can only execute code after passing programmatic verification gates.

Restricting initial production access allows engineering teams to catch subtle runtime errors before they scale. Therefore, establishing this operational stability provides a safe foundation for feature expansion.

Expanding the system through progressive functional layers ensures that your teams maintain clear visibility over every operational change. Therefore, this structured methodology transforms complex legacy operations into safe, highly automated, agent-driven claims environments.

How Much Does Agentic Claims Processing Development Cost?

Agentic claims processing platform development usually costs $70,000 to $300,000, depending on the number of agents, claim lines, model complexity, core-system integrations, autonomy level, and compliance scope.

Consequently, understanding your precise operational requirements helps lock down budget expectations before writing code.

1. Development Cost by Platform Scope

| Platform Scope | Cost | What It Should Include |

| Focused claims-agent MVP | $70,000–$110,000 | One insurance line, one or two workflows, two to four agents, basic document AI, human review, and two or three integrations. |

| Production single-line platform | $120,000–$210,000 | Four to seven agents, policy RAG, fraud or severity models, core claims integration, approval workbench, monitoring, and audit controls. |

| Enterprise multi-line platform | $220,000–$300,000 | Seven to twelve agents, multiple core systems, computer vision or graph fraud models, cross-line data model, advanced governance, and regional configuration. |

2. Project Capital Allocation by Development Phase

- Discovery & Foundation: Deep workflow discovery and schema mapping cost $7,000 to $15,000, while engineering the baseline claims knowledge structures demands $10,000 to $35,000.

- Orchestration & Integration: Designing the core graph logic and training custom multi-agent processing systems requires $25,000 to $95,000, alongside $15,000 to $70,000 for building core integrations.

- Validation & Operations: Deploying compliance boundaries and automated testing loops costs $8,000 to $40,000, while configuring MLOps pipelines adds $5,000 to $25,000.

These specific phase allocations represent internal resource distributions rather than additional fees added to the total platform budget. Therefore, these figures guide how your implementation team balances engineering hours across the project lifecycle.

3. Timeline, Maintenance, and Team Engineering Requirements

- Project Delivery Timelines: Transitioning a focused MVP into production requires 12 to 16 weeks of development time. Meanwhile, a complete production single-line platform takes 5 to 8 months, and a multi-line enterprise rollout spans 8 to 12 months.

- Ongoing Maintenance Budgets: Annual maintenance costs scale between 15% and 25% of the initial development cost. This baseline budget covers regulatory policy updates, prompt testing, fraud-pattern updates, cloud infrastructure, and evaluation-set expansions.

- Required Engineering Team: Deploying a secure platform requires a cross-functional squad including a claims product owner, an operations specialist, a solution architect, and dedicated AI/ML engineers. Furthermore, data, backend, frontend, MLOps, QA, and compliance leads coordinate to secure the infrastructure.

Investing $70,000 to $300,000 in custom agentic development replaces rigid legacy automation with dynamic, bounded software systems that safely streamline exception handling. Ultimately, this structured capital layout ensures carrier-grade compliance, predictable production rollouts, and measurable reductions in long-term operational leakage.

5 Claims Automation Systems Worth Benchmarking

Analyzing established market platforms provides technical leaders with concrete architecture patterns for building internal systems. Studying these solutions highlights the boundary between off-the-shelf capabilities and the custom work needed to connect agents to specialized pipelines.

Ultimately, mapping these benchmarks helps carriers avoid architectural mistakes and design safe, bounded automation teams.

1. Industry Automation Profiles

- Lemonade AI Jim: Sets the standard for digital intake and low-complexity claims processing. Critically, its rules dictate that the model cannot automatically deny coverage, matching our bounded-autonomy thesis.

- Assured & Shift Technology: Assured demonstrates how to orchestrate multi-line datasets cleanly. Concurrently, Shift Technology highlights that fraud networks require full investigative data contexts, not just simple mathematical scores.

- Tractable & Guidewire ClaimCenter: Tractable proves that computer vision works best as a workflow triage feed rather than a standalone decision-maker. Meanwhile, Guidewire shows that agents should act as intelligent layers around systems of record rather than trying to replace them immediately.

2. Systems Benchmarking Matrix

| Benchmark Platform | Best-Known Capability | Architecture Lesson | What Requires Custom Development |

| Lemonade AI Jim | Conversational FNOL & instant low-risk payouts | Design the user journey and authority limits together. | Enterprise policy mapping & multi-line compliance logic. |

| Assured | Claims intake & structural workflow graph orchestration | Connect AI models to actual backend operational tasks. | Proprietary integration hooks for legacy systems. |

| Shift Technology | Network fraud detection & subrogation risk screening | Fraud models require continuous human expert feedback loops. | Custom multi-channel workflow escalation rules. |

| Tractable | Computer vision damage classification & triage | Visual data must feed downstream liability modules. | Local contractor rate logic & parts availability feeds. |

| Guidewire | Enterprise system of record & financial accounting | Position agents as intelligence layers around the core. | Differentiated agent contracts & orchestrator graphs. |

Benchmarking these commercial engines ensures your engineering squad copies proven design patterns while focusing resources on custom workflows. Therefore, isolating generic features from proprietary business logic maximizes the return on your technical platform investment.

Build Agentic Claims Processing Infrastructure With Intellivon

Intellivon builds custom claims-agent platforms for insurers, TPAs, MGAs, insurtech companies, and claims service providers that need more control than a generic claims copilot can provide.

- Workflow Mapping: Map FNOL, coverage, investigation, reserving, settlement, payment, and recovery workflows into unified systems.

- Orchestration Engineering: Build multi-agent orchestration with restricted tools, human approvals, evidence traces, and model monitoring.

- System Integration: Integrate Guidewire, Duck Creek, Majesco, ACORD data, fraud services, estimating systems, medical data, and payment infrastructure.

- Production Deployment: Develop production-ready AI using document intelligence, RAG, predictive ML, graph analytics, computer vision, MLOps, and secure cloud architecture.

Generic software forces your operational reality into pre-built templates. Therefore, partnering with Intellivon delivers an enterprise-grade automation engine designed around your unique authority boundaries, compliance frameworks, and legacy systems.

Conclusion

In summary, moving toward an agentic model allows carriers to scale processing capacity safely without sacrificing control. Consequently, dividing responsibilities among bounded micro-agents prevents financial leakage while maintaining strict regulatory compliance.

Therefore, the transition requires a deliberate, step-by-step rollout that begins with isolated workflows and clear authority limits. Ultimately, this structured engineering approach transforms unpredictable AI tools into a dependable, carrier-grade enterprise infrastructure.

FAQs

Q1. Can an AI Agent Approve or Deny Insurance Claims Without a Human?

A1. Low-risk approvals and payments can be automated within defined limits. However, coverage denials, high-severity claims, fraud allegations, medical necessity disputes, litigation, and material reserve changes should require qualified human review. Consequently, human oversight protects the organization from compliance exposure while maintaining high customer service standards during complex disputes.

Q2. Should an Insurer Build or Buy Claims Automation Software?

A2. Buy when workflows are standard and existing modules meet most requirements. Conversely, choose to build when custom integrations, proprietary claim rules, operating differentiation, data-control requirements, or cross-system orchestration make standard software restrictive. Ultimately, custom building preserves your unique competitive advantage and protects proprietary carrier workflows.

Q3. What Is a Realistic Straight-Through Processing Rate?

A3. Do not promise a universal percentage because rates vary by target line. Instead, set the target to the eligible claim segment. For instance, a narrow, low-severity segment can achieve high automation. Meanwhile, bodily injury, litigation, coverage disputes, and large losses should remain human-led to prevent systemic payment leakage.

Q4. Can One Platform Support P&C, Health, Life, and Specialty Claims?

A4. The orchestration, security, audit, and integration foundation can be shared across teams. Nevertheless, each insurance line still needs separate evidence models, policy logic, approval rules, specialist workbenches, compliance requirements, and evaluation datasets. Therefore, a modular platform layout remains essential for supporting highly varied multi-line portfolios.

Q5. Can an AI Agent Negotiate Claim Settlements With Policyholders?

A5. It can present pre-approved offers and handle narrow negotiation ranges for eligible claims. Furthermore, these transactions must stay within strict authority limits. However, bodily injury, disputed liability, represented claimants, vulnerable customers, and high-value settlements require qualified human oversight to ensure legal compliance and fair outcomes.

To Sum It Up

- A general claims bot creates weaker controls than several agents with narrow jobs, permissions, and escalation rules.

- Straight-through processing should be measured by eligible claim segment, not advertised as one platform-wide percentage.

- A coverage agent should never return a decision without identifying the applicable policy version and supporting language.

- The cost increase from $110,000 to $300,000 usually comes from integrations, governance, computer vision, and multi-line complexity rather than LLM usage.

- Claims autonomy should expand according to evidence quality, financial authority, reversibility, and operational performance.