Key Takeaways:

- AI AML investigation software connects transaction data, KYC records, screening findings, and SAR workflows together.

- ML-based risk prioritization, entity resolution, and graph analytics convert raw alerts into structured investigation cases.

- RAG-grounded investigation summaries and SAR drafts support analysts while humans retain all escalation decisions.

- SAR confidentiality, audit controls, FinCEN, and FFIEC requirements are non-negotiable compliance architecture requirements.

- How Intellivon designs and implements AI AML investigation platforms costing $60,000 to $450,000 depending on scope.

Fintech companies build AI AML investigation systems by stacking three layers on top of existing transaction monitoring infrastructure. Those layers are ML alert scoring, graph analytics, and LLM-generated case summaries. Together, they replace the manual data pull, case building, and SAR drafting that slow every compliance team at scale.

Without a self-improving feedback loop in the scoring model, the platform can automate false positives but cannot reduce them. But when investigator decisions feed back into the scoring model as training data, the system gets better with every case it closes. That is how institutions detected 2 to 4 times more genuine suspicious activity and built a program that examiners can actually defend.

Intellivon has built AI AML investigation systems for fintech companies for over ten years, always examination-ready. That means audit trail design, model explainability, and workflow documentation go into the build before training begins, not after. This post covers model selection, graph analytics, LLM integration, workflow design, and development cost by phase, so you leave with a complete build picture.

What Is AI AML Investigation Software for Fintechs?

AI AML investigation software is a controlled case platform that helps fintech compliance teams review suspicious activity after an alert is generated. It gathers transaction records, customer risk information, screening findings, and connected-party evidence into one interface.

Therefore, you must realize this system is not limited to detecting suspicious payments. It actively supports the critical financial crime investigation workflow required after an initial warning appears.

For example, the software automatically retrieves deep merchant context, pulls past KYC/EDD records, connects crypto wallets, and surfaces adverse-media findings.

Furthermore, it automates investigation case summarization and prepares regulatory reporting investigation narrative drafts while maintaining an immutable audit history.

System Capabilities for Fintech Architecture

| System Capability | What It Means for a Fintech Buyer |

| Alert investigation workspace | Analysts can examine risk signals inside a structured case rather than across disconnected tools. |

| Evidence consolidation | Customer, transaction, screening and relationship data become available in one review path. |

| AI-supported analysis | Models may prioritize risk, reveal networks or prepare grounded summaries. |

| Human decision controls | Compliance reviewers retain responsibility for closure, escalation and SAR filing decisions. |

| Regulatory documentation | The platform preserves case reasoning, approvals, reporting status and audit history. |

Core Infrastructure Differentiation

Consequently, you should never view this technology as a direct replacement for transaction monitoring. The clear operational differences between these two systems are broken down in the table below:

| Architectural Component | Transaction Monitoring System | AI AML Investigation System |

| Primary Function | Generates or prioritizes raw risk signals. | Manages the evidence, analysis, and documentation. |

| Operational Workflow | Flags basic threshold or rule violations. | Coordinates the controlled decision workflow that follows those signals. |

| Regulatory Alignment | Serves as the initial alert mechanism. | Protects your compliance audit trail with absolute FFIEC examination readiness (Source: [FFIEC, Suspicious Activity Reporting Examination Procedures]). |

Ultimately, the platform does not decide that suspicious activity exists simply because an alert appears. Instead, it gives qualified reviewers the evidence, analysis, and human-in-the-loop investigation review controls needed to reach and document that decision.

Why Fintechs Need AML Investigation Software After Alerts

Fintech companies increasingly need investigation infrastructure because transaction monitoring creates risk signals, while qualified reviewers still need to establish what happened, which parties are connected, why the behaviour matters, and whether reporting is required.

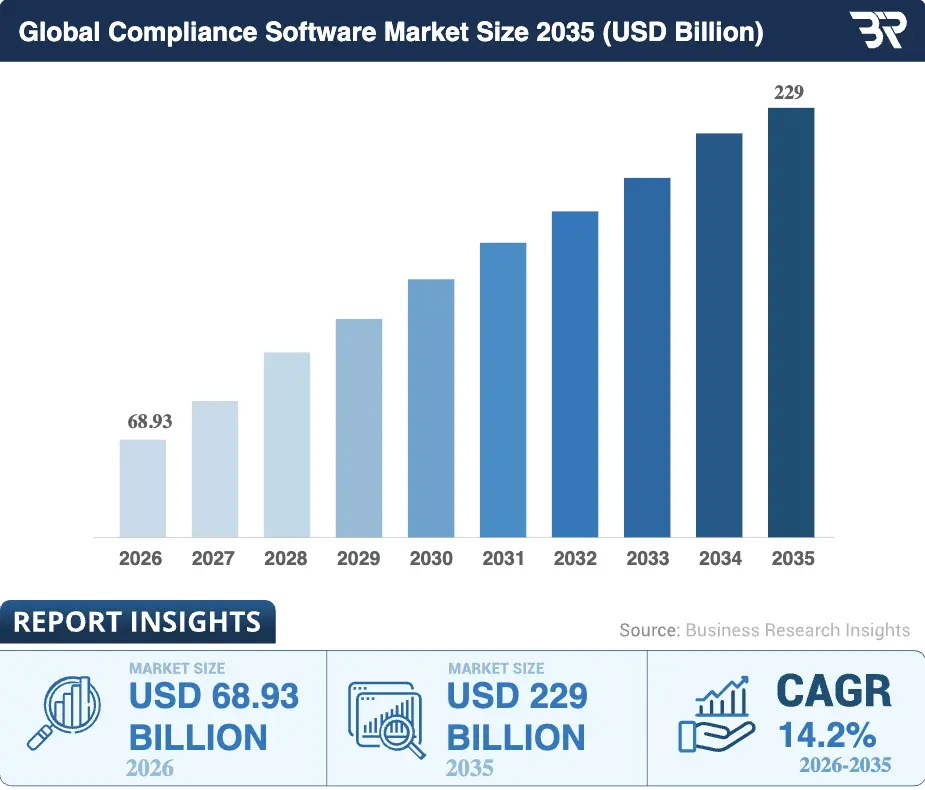

At the same time, the global market for specialized financial compliance software is growing rapidly at an accelerating compound annual growth rate (CAGR). According to sector reports, the broader regulatory and compliance software market is valued at approximately $68.93 billion in 2026 and is on track to experience steady double-digit expansion over the next decade. Digital payments, real-time transfers, embedded finance, and digital assets widen the evidence required for each decision.

1. Resolving Neobank Multi-Entity Context

Neobanks must quickly combine data from diverse internal platforms and external banking partners to build a single profile. This data integration allows your compliance team to evaluate risks across multiple accounts simultaneously:

- Sponsor-Bank Data: Merges internal ledger balances with external custodial records.

- Account Relationships: Links primary checking profiles to secondary digital wallets.

2. Tracking Real-Time Payment Payouts

High-velocity payment platforms require instant context regarding where funds are moving across the network. Because real-time payment AML threats move in seconds, analysts need automated evidence gathering:

- Merchant Profiles: Track sudden spikes in merchant transaction volumes.

- Counterparty Tracking: Pinpoints the ultimate destination of cross-border wire transfers.

3. Mapping Crypto Wallet Fund Flows

Crypto platforms face unique fintech-specific AML challenges due to the pseudonymous nature of blockchain transactions. Therefore, your workspace must pull live distributed ledger data directly into the active case:

- Wallet Exposure: Measures direct interaction with high-risk mixing services.

- Blockchain Analytics: Visualizes complex fund hops across public networks.

4. Gathering Fragmented Identity Context

Analysts frequently spend hours manually opening separate tools to check background information on flagged customers. Consequently, consolidating these fields accelerates your financial crime investigation workflow:

- KYC/EDD Records: Pulls original onboarding documents and enhanced diligence notes.

- Sanctions Screening: Surfaces real-time hits from global OFAC watchlists.

5. Standardizing the Final Documentation Path

Writing summaries for thousands of alerts creates an operational logjam that delays regulatory deadlines. Automation fixes this bottleneck via:

- Investigation Case Summarization: Generates consistent evidence profiles automatically.

- SAR Narrative Drafts: Structures legal-grade summaries for final human review.

Moving From Raw Signals to Controlled Compliance Actions

Therefore, engineering and product teams must realize that a monitoring engine and a case management system AML platform are entirely separate technological layers. This centralized approach ensures you can streamline your financial crime investigation workflow without losing visibility or compromising sensitive user data.

Ultimately, a fintech firm commissioning this custom platform is not simply purchasing another basic alert dashboard. Instead, you are commissioning a controlled, legally compliant framework to move from raw data signals to supported outcomes for suspicious activity investigations (FinCEN SAR Filings by Industry).

What AI AML Investigation Software Must Do After an Alert

AI AML investigation software should convert a risk signal into a reviewable investigation case. It must assemble customer context, transaction history, linked entities, screening results, supporting evidence, analyst activity, reporting status, and decision history in one controlled workflow, while leaving regulatory judgment and filing approval with qualified compliance reviewers.

Therefore, this layout ensures that your engineering and compliance operations remain unified under a single, highly scannable platform layer.

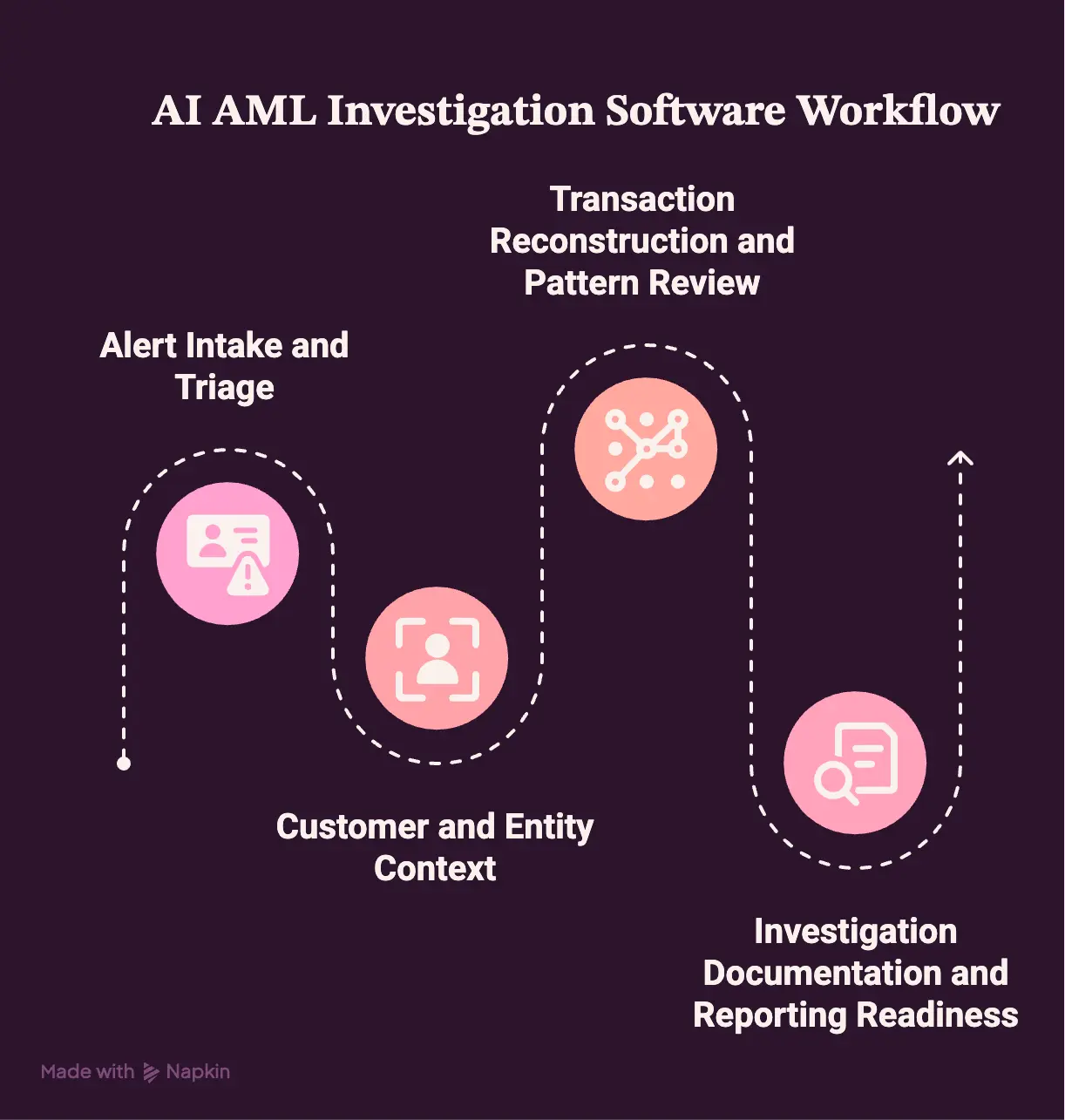

1. Alert Intake and Triage

The ingestion engine acts as the primary gatekeeper by swallowing risk signals from multiple disconnected compliance pipelines. Your automated architecture must route these triggers directly into an intelligent alert triage system:

- Core Event Triage: Consolidates standard transaction monitoring alerts alongside direct fraud or mule-account referrals.

- Identity & Screening Matches: Flags complex OFAC hit investigation records and matches high-risk individuals via your automated PEP investigation workflow.

- Web3 Security Ingestion: Captures native blockchain-risk alerts for digital-asset products to handle complex transaction monitoring alert reviews seamlessly.

2. Customer and Entity Context

Once an alert enters the active workspace, the system must build a clear operational picture around the flagged account entity. This automated profile collection shortens review times by standardizing data visibility:

- Onboarding Verification Logs: Pulls historic KYC and KYB records alongside complete CDD and EDD history.

- Risk Categorization Profiles: Speeds up your customer risk profile building process by reviewing beneficial ownership and past organizational structures.

- Remediation Tracking History: Surfaces prior internal investigations and connected account branches through an integrated KYC remediation workflow.

- Diligence Automation Pipelines: Maximizes operational speed by routing complex background information through custom CDD investigation automation and EDD investigation workflow modules.

3. Transaction Reconstruction and Pattern Review

Compliance operators cannot waste time manually mapping ledger movements or tracing currency links across separate bank networks. Accordingly, the system rebuilds payment paths to expose illicit transfer patterns:

- Movement Pattern Analysis: Connects payment timelines, channel types, and exact wire transfer investigation paths.

- Layering and Structuring Alerts: Pinpoints hidden structuring investigation patterns and tracks rapid layering detection events.

- Flow Graph Analytics: Automatically maps complex counterparty interactions by executing unified payment pattern analysis across diverse fiat and crypto wallet channels.

4. Investigation Documentation and Reporting Readiness

The final phase of the investigation must turn collected data into auditable proof that satisfies federal examiners. Automated text drafting reduces manual writing strain while preserving complete regulatory transparency:

- Dossier Assembly Packs: Powers fast investigation case summarization by collecting and indexing transaction files automatically.

- Regulatory Text Assistance: Speeds up your SAR narrative generation and cuts manual writing overhead using private LLM blocks.

- Filing Compliance Frameworks: Enhances your broad regulatory reporting investigation path through complete case documentation automation tools.

Ultimately, the platform creates measurable enterprise value only when AI-supported outputs remain traceable to source evidence and reviewer actions. That creates the central buyer question: what must an AI-prepared case file prove before anyone relies on it?

Intelligent investigation software turns raw risk triggers into comprehensive, audit-ready case files by automating data collection, tracing transaction webs, and drafting compliant narrative records under human control.

For a deeper breakdown of the upstream monitoring layer that creates these initial investigation signals, see our guide on How To Build an AI-Powered Transaction Monitoring System.

What Evidence Must an AI AML Case File Include?

A fintech company should not rely on an AI-prepared AML case file unless it proves five things: who was investigated, what activity occurred, why the behaviour required scrutiny, which evidence supports that reasoning, and which qualified reviewer approved the outcome. Even though AI may organise case material and draft explanations efficiently, real regulatory accountability must remain completely visible.

Ultimately, the fintech is not commissioning a narrative generator. It is commissioning a case system that must connect each material conclusion to verified evidence and accountable review. Consequently, this architecture directly ensures your operations are completely prepared for external audits.

Core Case File Evidence Requirements

| Evidence Requirement | What the Platform Must Capture | Why the Buyer Should Require It |

| Subject identity and relationships | Customer, business, account, merchant, beneficial owner, beneficiary, wallet and linked-entity records | Establishes exactly who the case concerns |

| Activity timeline | Transactions, timestamps, channels, amounts, counterparties and payment paths | Shows what happened and when |

| Risk explanation | Triggered alerts, typologies, sanctions findings, unusual behaviour and connected-party risk | Explains why the activity required review |

| Source evidence | Transaction rows, KYC/KYB records, graph links, screening records, documents and approved research | Prevents unsupported AI reasoning |

| Decision accountability | Analyst actions, reviewer edits, escalation path, filing outcome and audit history | Demonstrates who owned the decision |

Safe Integration Rules for AI and RAG Workflows

Because large language models can occasionally invent details or hallucinate facts, you must implement strict technical guardrails. A retrieval-augmented generation case research workflow may assist your compliance analysts with summaries, or SAR drafts only when:

- Evidence Constraints: Data retrieval is strictly limited to permitted case evidence records.

- Traceable Assertions: All material assertions inside the text are dynamically linked to verified financial logs.

- Version Governance: Every generated output is stored and versioned to prevent hidden data overwrites.

- Change Logging: All analyst adjustments and reviewer edits are documented in an investigation audit trail.

- Filing Validation: The final regulatory filing authority remains entirely human-controlled.

By integrating these specific RAG pipeline compliance documents into your platform, you can confidently run generative AI SAR drafting modules without introducing regulatory blind spots. Ultimately, this clean traceability gives the platform its core investigative value, while access controls determine whether that evidence can be used safely.

An AI-generated report is only as valuable as the underlying proof it links to. True compliance requires a system that ties every single summary sentence directly back to an immutable transaction record.

How AI AML Platforms Protect Confidential SAR Data

An AI AML investigation platform must distinguish between underlying investigation evidence and SAR-confidential information. Transaction facts, customer data, and relationship evidence may support legitimate investigation workflows, while SARs, draft filing materials, and information revealing whether a SAR exists require tightly controlled access, logging, and disclosure restrictions.

Consequently, this architectural barrier prevents devastating, illegal leaks of sensitive federal compliance data across your enterprise.

1. Investigation Evidence and SAR Information Are Not Identical

Fintech platforms must implement distinct data-handling pipelines depending on the specific compliance asset class. The clear security boundaries required across the system architecture include:

| Information Type | Example | Platform Handling Requirement |

| Underlying case evidence | Transactions, customer records, beneficial ownership, screening findings, graph relationships | Permissioned investigation access |

| AI-prepared case analysis | Summaries, chronology, risk explanation, and retrieved evidence | Controlled review and version history |

| SAR-confidential information | Filed SAR, draft linked to filing status, decision revealing whether a SAR exists | Restricted access, logging and disclosure controls |

| Supporting SAR documentation | Evidence that assisted the filing decision | Confidential treatment where it indicates SAR existence; retention controls |

2. LLM Access and Platform Security Controls

To preserve strict compliance, your engineering team must implement a rigorous zero-trust architecture fintech blueprint. This strategy applies deep technical constraints to model processing:

- Model Context Limits: Large language models must only retrieve underlying case evidence rows, entirely omitting active filing status.

- Narrative Isolation: All text drafts must be completely isolated inside data encryption investigation platform environments.

- Logging and Redaction: The platform enforces role-based access control investigation rules and masks identifying data before any external API calls.

Ultimately, these combined boundaries ensure complete audit trail immutability across engineering, compliance, and sponsor-bank users.

3. Retention Requirements Affect Storage Architecture

The delivered platform must support retention of SARs and supporting documentation for the applicable required federal period. Storage architectures require searchable evidence lineage and controlled disclosure pathways to satisfy strict banking rules.

Furthermore, these repositories must operate under tight international data silos to maintain compliance with federal cross-border guidelines.

A platform may help investigate suspicious activity only if it also protects whether and how that activity became a SAR matter. Once data-access boundaries are clear, leaders can evaluate which technology should support each investigation task.

How AI Supports Human-Led AML Investigation Decisions

An AI AML investigation platform should assign technology according to decision risk. Machine-learning models can prioritize alerts and identify unusual behavior. Graph analytics can reveal linked parties and fund movement. LLM workflows can retrieve and summarize evidence. Compliance reviewers must retain closure, escalation, SAR approval, and filing responsibility.

Therefore, you should think of AI as an analytical assistant that uncovers hidden patterns rather than an independent decision-maker.

While algorithms handle the heavy data sorting, your human team maintains full oversight of the financial crime investigation workflow.

1. Technology-to-Decision Mapping Matrix

To make this architecture easy to understand, the table below breaks down exactly which technology component handles each task, alongside the specific decision that must remain under human control:

| Investigation Need | Suitable Component | Output the Platform Provides | Decision That Remains Human-Owned |

| Alert prioritization | Rules plus ML risk scoring | Ranked case queue and risk indicators | Threshold approval and case review |

| Behavior-pattern analysis | Typology rules and anomaly models | Structuring, velocity, or unusual-payment signals | Determining investigation relevance |

| Connected-party review | Entity resolution and graph analytics | Relationship map, ownership path, or wallet link | Confirming material relationship risk |

| Sanctions and PEP review | Screening engine with matching rules | Potential hit and supporting context | Clearing or escalating the match |

| Document and adverse-media review | NLP retrieval workflow | Relevant evidence extracts | Assessing credibility and relevance |

| Investigation summary | RAG-grounded LLM | Evidence-cited chronology and summary | Editing and approving case reasoning |

| SAR narrative preparation | Controlled generative AI workflow | Draft narrative linked to evidence | Filing decision and final approval |

| Regulatory submission | Permissioned workflow integration | Submission-ready case record | Authorized reporting action |

2. Critical Model Risk and Governance Requirements

Furthermore, enterprise buyers must realize that different AI models require entirely separate testing and validation frameworks. For instance, you will use traditional statistical methods for your underlying risk scoring model investigation pipeline. However, the regulatory landscape for newer generative systems has recently shifted.

Specifically, the OCC’s revised model-risk guidance issued on April 17, 2026, explicitly states that generative AI and agentic AI models are outside the scope of that formal guidance because these technologies are novel and rapidly evolving.

Therefore, your product teams should implement distinct internal controls to handle a modern LLM for investigation narratives module safely. These separate engineering guardrails must include:

- Evidence Grounding: Enforcing strict mathematical grounding to tie all text summaries back to source logs.

- Factual Review Controls: Mandating side-by-side verification panels to check for text hallucinations.

- Output Audit Logging: Saving all raw prompts, model parameters, and human edits to an immutable history.

Ultimately, this dual-governance design ensures your core predictive engines pass standard model validation AML audits while keeping your language models safely contained.

Architecture of AI AML Investigation Software for Fintechs

A fintech-grade AI AML investigation platform requires connected layers for financial data, identity resolution, case orchestration, relationship analysis, evidence retrieval, AI-supported documentation, human decisions, and security governance. Together, these layers allow compliance teams to understand suspicious activity while preserving the evidence and approval history behind each outcome.

For a deeper breakdown of compliance requirements across AI fintech infrastructure, see our guide on What Compliance Is Needed for AI Fintech Infrastructure?.

1. Modular Platform Layers and Procurement Value

| Platform Layer | What Intellivon Would Build or Configure | Buyer Value |

| Transaction and customer-data layer | Connections to payments, wallets, ledgers, KYC/KYB, CDD and EDD data | Gives investigators complete customer and activity context |

| Entity-resolution layer | Matching across customers, accounts, merchants, beneficiaries, owners and wallets | Reveals connected exposure hidden across records |

| Alert and case-orchestration layer | Alert intake, assignment, enrichment, queueing, escalation and review states | Turns signals into controlled case workflows |

| Graph investigation layer | Relationship views, ownership mapping, counterparty paths and fund-flow links | Supports layering, shell-company and connected-wallet analysis |

| Evidence and retrieval layer | Approved document, transaction and policy retrieval with record citations | Grounds summaries and case reasoning |

| LLM-supported workspace | Structured case summaries, chronologies and SAR draft support | Reduces repetitive documentation while preserving review |

| Human decision and reporting layer | Approval steps, case dispositions, filing workflow and continuing activity | Keeps regulatory authority accountable |

| Security and governance layer | RBAC, encryption, immutable logs, model monitoring, and retention controls | Protects sensitive case data and audit defensibility |

2. Graph and Entity Intelligence

Fintech platforms must deploy an advanced entity resolution fintech framework to expose hidden relationships across multiple customer files. This graph database infrastructure maps identical device IDs, shared banking routes, and recurring beneficial ownership investigation links:

- Network Mapping: Conducts automated network analysis and financial crime lookups to flag shell company identification risks.

- Link Analysis Pipelines: Executes fast link analysis and financial crime steps to locate matching beneficiary clusters and hidden structuring patterns.

- Graph Monitoring Guardrails: Implements specialized graph analytics AML investigation modules only when the underlying dataset justifies validation costs.

Consequently, engineers should avoid complex graph neural network transaction analysis models unless high transaction volumes require automated multi-hop processing.

3. Evidence and LLM Workspace

The platform connects verified evidence repositories directly to a private large language model environment via secure pipelines. This integration accelerates your core workflow without risking data exposure:

- Evidence Grounding: Pulls real-time transaction history records into a closed RAG system to draft clear chronologies.

- Version History Tracking: Logs all manual investigator edits alongside the primary AI-generated report summaries.

- Access Control Isolation: Enforces strict role barriers to keep confidential SAR filing data hidden from unauthorized internal eyes.

Ultimately, your core architecture should be judged by whether it creates a complete, controlled case record rather than another disconnected compliance tool.

Top 5 AI AML Investigation Platforms for Fintechs

Existing AI AML platforms show that modern investigation technology now extends beyond alerts into case workflows, relationship analysis, evidence packaging, reviewer support, and reporting readiness.

These market benchmarks help fintech leaders understand expected industry capabilities. However, a custom internal platform becomes relevant when their products, engineering integrations, ownership model, or investigation controls require a tailored architecture.

Market Capability Benchmarks

To benchmark your internal requirements, product leads can analyze the distinct architectural approaches deployed across the compliance ecosystem:

| Platform Example | Publicly Described Capability to Reference | Buyer Lesson for an Internal Custom Platform |

| HAWK | AML investigative agent supporting data gathering, case summaries, typology identification, and SAR narrative drafting (Hawk AI, 2026) | Investigation assistance requires evidence visibility and human control, not only faster output. |

| Unit21 | AI-powered case management, graph analysis, QA oversight, privacy controls, and human-in-the-loop audit history (Unit21, 2026) | Workflow orchestration and regulator-ready accountability belong in the platform scope. |

| C3 AI | Intelligent case recommendations, network link analysis, KYC context, model evidence packages and data lineage (C3 AI, 2026) | Prediction performance must connect to interpretable evidence. |

| Google Cloud AML AI | Risk scoring, explainability and investigator-prioritisation guidance (Google Cloud, 2026) | Risk scores should guide investigation priority, not replace investigation decisions. |

| Tookitaki | AI-supported transaction monitoring, screening, customer due diligence and AML investigation workflows (Tookitaki, 2026) | Coverage across customer and transaction risk sources remains important for fintech programmes. |

Consequently, analyzing these market benchmarks shows that an enterprise compliance platform must serve as a comprehensive evidence aggregator rather than a generic alert queue.

While pre-built vendors offer rigid, standard templates, a custom internal application matches your specific API structure, proprietary database pipelines, and sponsor-bank logging duties.

Compliance Controls Fintech Leaders Must Expect in the Platform

An AI AML investigation platform should support documented alert review, responsible SAR decisions, timely filing, continuing-activity monitoring, evidence retention and restricted access to sensitive reporting information.

For U.S.-connected fintech programmes, the relevant control expectations include FinCEN requirements, FFIEC examination procedures and any sponsor-bank governance obligations.

Therefore, engineering and product teams must embed hard regulatory boundaries directly into the application’s core code logic rather than treating security controls as optional user preferences.

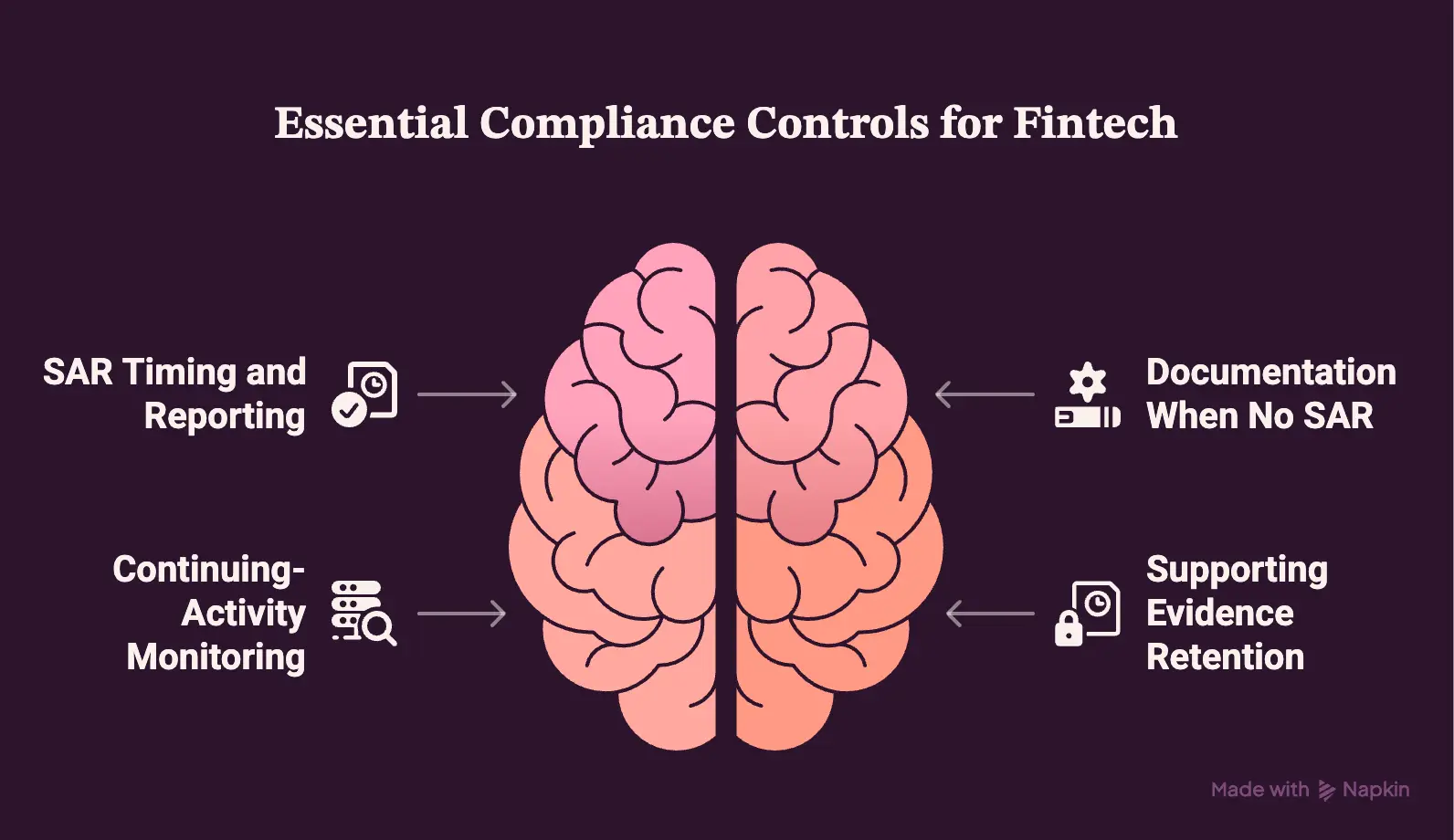

1. SAR Timing and Reporting Controls

Operating within strict banking rules means your system architecture must actively enforce chronological regulatory deadlines. The platform case engine manages reporting timelines through highly visible tracking metrics:

- Deadline Countdown Logs: Automatically tracks the mandatory 30-day filing deadline after initial detection of facts forming a basis for a SAR.

- Extension Buffer Management: Flags an automatic 60-day extension state inside the workflow queue specifically where no clear suspect is identified.

- Narrative Version Verification: Preserves a complete text approval history whenever an operational lead modifies an automated draft.

Consequently, user access rules prevent unauthorized employees from altering filing states or viewing confidential submission queues without permissioned credentials.

2. Documentation When No SAR Is Filed

A useful enterprise compliance platform must preserve defensible non-filing decisions, not only support successful filings. When an analyst decides an alert does not point to true money laundering, the system must enforce strict validation documentation before closure:

- Evidence Record Freezing: Locks all transaction rows, external KYC verifications, and graph pathways linked to the review instance.

- Mandatory Rational Input: Restricts the user dashboard from closing an event until the reviewer inputs a clear, structured non-filing reason.

- Future Trigger Links: Automatically establishes a conditional monitoring benchmark to reconnect the account history if matching risks reappear later.

Ultimately, keeping these clear records protects your platform from retroactive regulatory penalties during unexpected state and federal compliance examinations.

3. Continuing-Activity Monitoring

When a suspicious activity report is successfully submitted, the regulatory obligation does not simply terminate. Instead, your internal workflow software must establish a structured cadence to track ongoing transaction patterns:

- Follow-Up Review Scheduling: Configures an automatic 90-day alert review trigger to inspect the subject’s subsequent payment behaviors.

- Cross-Case Entity Linking: Automatically attaches historical case files to new incoming risk signals involving identical beneficial owners.

- Restricted Prior Referencing: Permits authorized compliance officers to view past SAR numbers while shielding those text folders from general platform users.

As a result, your compliance department receives clear filing reminders, ensuring the fintech remains aligned with ongoing federal reporting requirements.

4. Supporting Evidence Retention

The delivered enterprise platform must support the retention of SARs and supporting documentation for the full legally mandated period. Your database infrastructure should prioritize long-term preservation and controlled access paths:

- Secure Electronic Isolation: Encrypts and stores official submission files within separate, single-tenant cloud database perimeters.

- Authorized Request Lineage: Provides a clean extraction engine to safely package transaction records for law enforcement agencies.

- Audit Trail Ingestion Logs: Saves a permanent history of every internal data export or file review action across the organization.

Therefore, this rigorous storage design guarantees that your broader compliance program maintains perfect audit defensibility during annual structural reviews. AI can assist investigation work only when the delivered platform also preserves reporting discipline, evidence retention, and human accountability.

For a deeper breakdown of AI-supported AML research, reporting preparation and governance workflows, see our guide on How Can Banks Develop an AI AML Compliance Copilot?.

Integrations Required for Complete AML Investigations

A fintech investigation platform can only explain suspicious activity when it securely connects the systems that hold customer identity, money movement, relationship data, screening findings and reporting outcomes. The required integration set differs for neobanks, payment platforms, embedded finance providers and crypto exchanges, but missing evidence sources weaken case quality.

Therefore, your product leads must treat integration depth as a core functional requirement during the initial procurement phase rather than a minor configuration task.

1. Unified Compliance Integration Matrix

To ensure absolute coverage across your payment rails, an API-based AML investigation architecture maps directly to several primary internal and external data environments:

| Integration Category | What It Contributes | Relevant Fintech Environment |

| Transaction ledger and payment rails | Amounts, timestamps, channels, beneficiaries, merchant payouts and fund movement | Neobanks, payment platforms, embedded finance |

| Core banking and sponsor-bank systems | Account context, handoff records, reporting responsibility and review status | BaaS and sponsor-bank programmes |

| KYC, KYB, CDD and EDD tools | Identity, beneficial ownership, customer risk and remediation history | All regulated fintech products |

| Sanctions, OFAC and PEP screening | Hit candidates, review status and risk context | Payments, banking, wallets and cross-border products |

| Adverse-media and OSINT tools | External risk indicators and enhanced investigation evidence | Higher-risk customer reviews |

| Case management and filing systems | Escalations, approvals, SAR status and continuing-review history | U.S.-connected compliance programmes |

| Blockchain analytics | Wallet attribution, digital-asset exposure and fund-flow tracing | Exchanges, stablecoin providers and crypto products |

2. Core Infrastructure and Financial Ledger Connectivity

Building a resilient neobank AML investigation interface or a high-capacity payment platform AML dashboard requires deep core banking integration and fintech hooks.

This connection directly streams real-time database inputs from your primary ledgers straight into the case orchestration queues:

- Ledger Field Syncing: Matches direct debit rows, bank routing paths, and embedded finance AML metadata instantly.

- Sponsor-Bank Handshaking: Automates verification logs to let external bank partners audit case files safely.

Consequently, having a robust API-based AML investigation structure prevents your reviewers from wasting time cross-checking mismatched ledger statements across separate compliance instances.

3. Web3 Security and Digital Asset Intelligence

Crypto exchanges, wallet providers, and modern stablecoin platforms must deploy a specialized digital asset AML investigation layer to track decentralized fund hops.

For that reason, engineers must link the core compliance dashboard to leading public ledger data providers:

- Chainalysis Integration: Hooks into systems like Chainalysis KYT via API to pull real-time wallet attribution and trace transaction flows down to specific public nodes (Chainalysis KYT Software, 2026).

- TRM Labs Integration: Establishes webhooks with platforms like TRM Labs Transaction Monitoring to capture granular, cross-chain smart contract data and flag advanced obfuscation signatures automatically (TRM Transaction Monitoring, 2026).

Furthermore, these tools feed live crypto transaction investigation logs directly into standard case views, letting analysts track illicit currency mixing risks in real time.

4. External Risk and Identity Verification Pipelines

To round out your broad financial crime investigation workflow, your development team should connect advanced background verification APIs. These automated searches enrich cases with third-party verification records without manual human clicking:

- Identity Dossier Mapping: Merges basic onboarding records with ongoing sanctions list screening updates.

- Background Search Automation: Deploys adverse media search automation modules to aggregate news files and calculate risk scores.

- Open-Source Intelligence Tracking: Gathers digital footprints using open source intelligence OSINT tools to verify high-risk merchant ownership details.

Ultimately, this integration depth determines how complete the investigator’s case view becomes and materially affects development cost. That is why commissioning cost must be assessed against evidence and workflow scope, not a generic feature list.

An AML tool cannot function in a vacuum. Therefore, true operational efficiency relies on deep API links that stitch core banking ledgers, identity tools, and blockchain trackers into a single screen.

AI AML Investigation System Development Cost

Commissioning custom AI AML investigation software typically costs $60,000–$120,000 for an assistant MVP, $120,000–$280,000 for a production platform, and $280,000–$450,000+ for a graph-enabled system. This price range scales based on case orchestration, entity graphs, evidence controls, sponsor-bank workflows, or blockchain intelligence required by your infrastructure.

1. Cost by Commissioned Platform Scope

The total financial investment is directly tied to the level of system capability and data connectivity your compliance program requires:

| Platform Scope | Estimated Cost | What the Fintech Receives |

| Focused investigation-assistant MVP | $60,000–$120,000 | Evidence retrieval, alert enrichment, case summaries, controlled narrative support and reviewer workflow |

| Production fintech investigation platform | $120,000–$280,000 | Case management, integrations, risk scoring, entity context, reporting controls, audit history and monitoring |

| Advanced internal investigation platform | $280,000–$450,000+ | Graph analytics, blockchain intelligence, sponsor-bank workflows, multi-product coverage, advanced LLM controls and multi-region requirements |

2. Cost by Development Component

Engineering budget allocations must be carefully itemized across the core software components to ensure smooth delivery:

| Development Component | Estimated Cost Range | Scope Included |

| Investigation and compliance-scope assessment | $8,000–$18,000 | Alert categories, product rails, reviewer roles, decision boundaries and reporting obligations |

| Case workspace and evidence architecture | $10,000–$25,000 | Investigator views, evidence panels, case history, approval states and audit design |

| Data integration and normalisation | $15,000–$55,000 | Ledgers, KYC/KYB, screening, sponsor-bank systems and adverse-media sources |

| Risk scoring and prioritisation models | $15,000–$55,000 | Typology logic, behavioural scoring, explainability and threshold review |

| Entity resolution and graph investigation | $15,000–$70,000 | Ownership mapping, counterparty links, wallet paths and network analysis |

| LLM and evidence-grounded narrative support | $12,000–$50,000 | RAG, case summaries, SAR draft assistance, citations and factuality controls |

| Security, confidentiality and audit controls | $15,000–$55,000 | RBAC, encryption, SAR restrictions, retention controls and audit logging |

| Validation, pilot rollout and monitoring | $10,000–$40,000 | Testing, reviewer checks, model monitoring and production acceptance |

| Crypto or multi-jurisdiction expansion | $35,000–$120,000+ | Blockchain intelligence and regional compliance logic |

3. Ongoing Maintenance Cost

Annual maintenance generally requires 18%–25% of the original development investment to preserve system integrity. These recurring costs go directly toward integration maintenance, security controls, model monitoring, and continuous LLM evaluation.

Furthermore, this resource pool handles necessary evidence and retention controls, screening updates, regulatory workflow changes, and analyst feedback and QA loops.

For a deeper budget breakdown of a narrower AI-supported AML investigation and reporting capability, see our guide on AI AML Compliance Copilot Development Cost.

Build AI AML Copilot Platforms With Intellivon

An AI AML copilot must do more than summarize alerts. It must help investigators retrieve evidence, understand transaction risk, review customer context, prepare defensible case narratives, and move cases forward without taking final compliance authority away from qualified officers.

Intellivon builds these platforms around governed intelligence, secure data access, clear human controls, and production-ready oversight.

1. AML Workflows Designed Around Investigator Decisions

An effective copilot begins with the work AML teams complete every day. Intellivon designs platforms around alert triage, case review, KYC/CDD verification, entity investigation, escalation preparation, and SAR drafting support. Each capability helps analysts work faster while keeping material decisions within controlled review workflows.

- Alert triage support with evidence-backed risk context.

- KYC, CDD, EDD, and beneficial ownership review assistance.

- Transaction pattern summaries across accounts and counterparties.

- Case disposition support with analyst approval checkpoints.

- Controlled SAR narrative drafting without automated filing authority.

2. Connected Evidence Across AML Data Systems

A copilot cannot assist investigators using incomplete transaction data. It needs governed access to the systems that contain customer identity, payment activity, screening results, earlier alerts, related entities, and review history. Intellivon builds the integration layer that brings this evidence into one investigation-ready workflow.

- Core banking data for customer accounts and activity history.

- Payment data across ACH, wires, cards, and real-time transfers.

- KYC, CIP, CDD, EDD, and ownership records.

- Sanctions, PEP, adverse media, and watchlist screening inputs.

- Existing transaction monitoring and case-management workflows.

- Prior disposition, escalation, and SAR review history.

3. Copilot Intelligence Built for AML Investigation Depth

AML teams need more than a generic chatbot connected to documents. Intellivon can combine transaction monitoring intelligence, entity resolution, graph analytics, grounded retrieval, and structured case support so investigators can examine risk from both transaction-level and relationship-level views.

- Transaction monitoring context for triggered alerts and scenarios.

- Entity resolution across linked customers, accounts, and counterparties.

- Graph analytics for network activity and layered transaction patterns.

- RAG-based retrieval from approved policies and case evidence.

- Evidence-linked summaries that show where each finding originated.

- Structured outputs for consistent analyst review and escalation.

4. Human-Controlled Decisions for Sensitive Compliance Actions

A compliance copilot should assist judgment, not silently replace it. Intellivon structures authority boundaries so the system can find information, organize evidence, draft explanations, and recommend actions while compliance officers retain ownership of escalation, closure approval, and SAR filing decisions.

- Investigator approval required for material case dispositions.

- Human control retained for SAR review and final filing decisions.

- Exception routing for unusual, high-risk, or incomplete cases.

- Reviewer override capture for continuous quality monitoring.

- Clear separation between copilot recommendation and officer decision.

- Full action history for internal review and regulatory examination.

5. Auditability, Governance, and Production Monitoring Built In

AML copilots operate inside regulated workflows, so every recommendation must remain reviewable after deployment. Intellivon designs platforms with the oversight controls needed to track system behavior, investigate errors, manage AI changes, and support compliance teams as governance expectations evolve.

- Version-controlled models, prompts, policies, and workflow rules.

- Traceable sources behind case summaries and draft narratives.

- Role-based access for analysts, reviewers, and compliance officers.

- Audit logs for retrieval, recommendations, approvals, and overrides.

- Model and response-quality monitoring after production release.

- Validation records for internal governance and examination readiness.

6. Enterprise AI Capability Applied to Fintech Compliance

Intellivon brings together enterprise AI development, LLM engineering, machine learning, MLOps, financial-data pipelines, secure integrations, and compliance workflow design. This matters because an AML copilot is not a standalone interface. It is a governed intelligence layer that must operate safely across existing banking and fintech systems.

Intellivon Capability Indicators:

- 500+ successful AI-driven projects delivered.

- 11+ years of industry experience.

- 200+ dedicated AI experts.

- Enterprise AI capability across LLMs, predictive risk models, MLOps, AI governance, KYC systems, and transaction-data pipelines.

- Fintech AI experience across compliance automation, fraud checks, risk intelligence, and financial workflow support.

Your AML team needs a copilot that reduces manual investigation effort while preserving accountability for sensitive compliance decisions.

Intellivon helps you build an AI AML copilot platform that connects the right evidence, supports the right workflows, records every material action, and remains governed from pilot to production.

Conclusion

Building a custom AI AML investigation platform transforms compliance from a manual tracking burden into a precise, automated operation. By integrating graph intelligence for identity mapping, predictive models for triage, and safe language models for drafting, fintechs eliminate operational bottlenecks while ensuring absolute regulatory readiness.

Ultimately, success depends on tracing every automated conclusion back to source evidence, keeping qualified human reviewers firmly in control of all final decisions.

Things To Know About AI AML Investigation Software

Q1.How much does fintech AML investigation system development cost?

A1. Commissioning custom software requires separate investment tiers based on your operational scale and technical architecture needs. A focused investigation-assistant MVP costs $60,000–$120,000, while a production fintech platform ranges from $120,000–$280,000. Additionally, an advanced graph-enabled or crypto-aware system costs $280,000–$450,000+.

Q2. Can an LLM AML investigation system build accurate SAR narrative drafts without making filing decisions?

A2. Yes, a properly integrated large language model can safely generate preliminary text drafts without exercising final regulatory authority. To achieve this, your engineering teams must ensure the system extracts data solely from permitted case evidence and dynamically cites supporting financial database records.

Q3. How should fintechs validate AI-generated investigation summaries?

A3. Validating platform outputs requires distinct testing pipelines depending on whether you are evaluating statistical models or generative text components. Your predictive risk-scoring models require rigorous historical back-testing, operational threshold reviews, feature explainability logs, and continuous data drift monitoring

Q4. Can AI automatically close low-risk AML alerts?

A4. Autonomous alert closure introduces much higher compliance risks than standard evidence gathering or basic case summarization. Consequently, your product leads should only implement automated dismissal rules under highly narrow behavior criteria with fully documented exception parameters.

Q5. Can an AI investigation platform share case evidence with a sponsor bank or another institution?

A5. The underlying transaction logs, customer identity files, and network relationship maps can be securely shared with external banking partners under strict programmatic access controls. This cooperative data exchange seamlessly supports authorized inter-bank communication, such as eligible USA PATRIOT Act Section 314(b) collaboration workflows.