Key Takeaways:

- Legacy backends consume 70% of tech budgets on maintenance, leaving no capacity for real-time AI decisioning at modern transaction volumes.

- Scalable AI payment backends need event-driven processing, stateless services, horizontal scaling, and queue-based handling working as one infrastructure layer.

- AI operates across pre-authorization scoring, dynamic routing, fraud detection, smart retries, and merchant risk monitoring in under 200 milliseconds.

- Model selection differs by function: XGBoost for fraud, reinforcement learning for routing, LSTMs for behavior, and isolation forests for anomaly detection.

- How Intellivon builds scalable AI payment backends your enterprise fully owns, with microservices architecture, compliance-ready data handling, and agentic payment controls built in.

When a payment system works well, the backend is hidden from view. Transactions clear, fraud decisions happen in real time, authorization logic runs smoothly, and every team, risk, compliance, finance, and operations gets what they need without issues. This result does not occur by chance. Instead, it comes from an AI backend designed correctly from the beginning.

For large companies, the backend is where AI can perform at scale or quietly fail under stress. It is also where data pipelines supply real-time models, where delays can affect whether a fraud decision is made before or after a transaction clears, and where compliance rules about data residency, auditability, and model governance must be built in, and not added on later. Getting this part right decides what the business can actually do with AI, both now and as volumes increase and new markets emerge.

At Intellivon, we create AI backends for payment systems that have little room for mistakes and high operational demands. In this blog, we will discuss the infrastructure choices, data architecture patterns, and scalability factors that companies must address when building an AI backend that payment operations can rely on.

Why Do Payment Firms Need AI Backends Now?

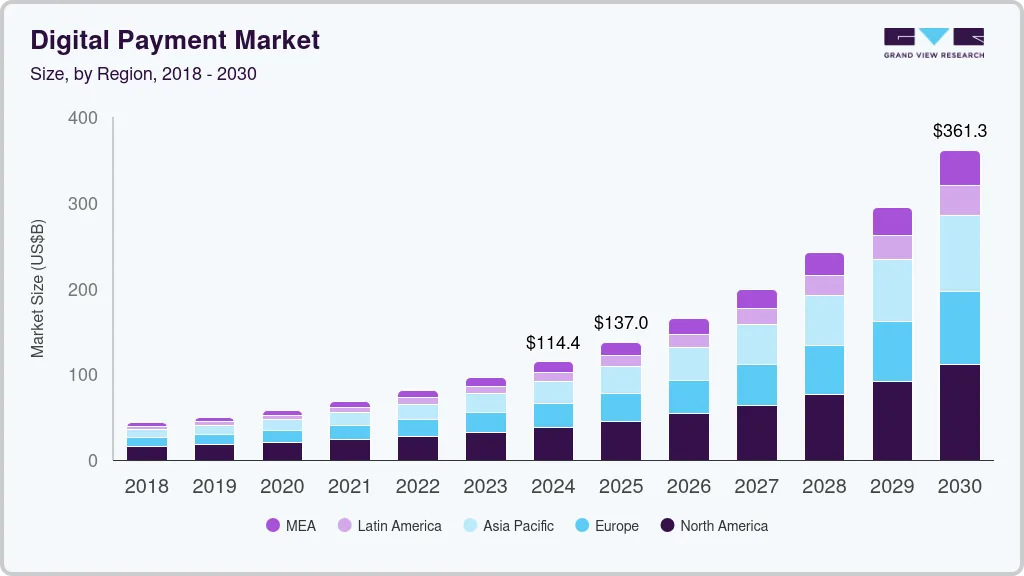

The global digital payment market was valued at USD 114.41 billion in 2024 and is projected to reach USD 361.30 billion by 2030, growing at a CAGR of 21.4%. That kind of trajectory happens in markets that are restructuring.

For anyone looking to build or invest in a payment platform today, the infrastructure decisions made now will determine how much of that growth they are positioned to capture.

Furthermore, legacy systems now consume nearly 70% of technology budgets just for basic maintenance. This financial drain prevents firms from innovating while their competitors adopt agile, AI-driven architectures. Therefore, shifting to AI is a strategic necessity.

1. Rising transaction volumes

Real-time payment transactions are projected to hit 428 billion annually by 2026. This surge is driven by platforms like India’s UPI. UPI now processes over 13 billion monthly transactions. Static backends struggle to handle these elastic demand spikes without significant latency.

Consequently, scaling now requires predictive resource allocation that only an AI-driven backend can provide. In addition, AI allows for seamless handling of high-frequency micro-transactions.

2. Real-time fraud pressure

Financial fraud losses reached a staggering $12.5 billion in 2024. This was a 558% increase over five years. Modern scammers use AI to launch sophisticated attacks. These attacks bypass traditional rule-based filters.

Therefore, enterprises must deploy deep learning models that analyze behavior in milliseconds. Waiting for post-transaction reviews is no longer a viable strategy for protecting capital. However, AI can block suspicious activity before the money leaves the account.

3. Smarter payment routing needs

Hidden inefficiencies and failed settlements cost fintechs up to 1.5% of their annual revenue. Traditional routing is often rigid. It fails to account for real-time bank health or fluctuating interchange fees.

However, AI orchestration can determine the most cost-effective path for every specific transaction. This optimization directly recovers lost margins and improves successful settlement rates. Thus, smarter routing transforms a cost center into a profit driver.

4. Demand for agentic payment flows

The industry is shifting from simple automation to autonomous, agentic payment systems. These systems can self-correct when a transaction fails. They automatically renegotiate routing during downtime. Business leaders need these “self-healing” backends to maintain 99.99% uptime.

Without this intelligence, operational overhead will continue to stifle your ability to scale globally. Therefore, agentic flows represent the next frontier of operational efficiency.

5. Limits of legacy payment cores

Most legacy cores were built for batch processing. They cannot handle the rich data required by ISO 20022 standards. These aging systems create integration bottlenecks. They delay new product launches by months.

Transitioning to an AI-native backend removes these technical debts. It allows you to process contextual data at high speeds. This speed is required for modern, instant cross-border transfers. Consequently, replacing legacy cores is the only way to stay competitive.

Modern payment firms must choose between evolving with AI or facing obsolescence. An intelligent backend ensures your platform remains profitable while handling unprecedented global demand.

What Is An AI Backend For Payment Systems?

An AI backend for payment systems is the foundational infrastructure layer that powers intelligent decision-making across the entire payment stack. It is where machine learning models are trained, deployed, and served in real time, handling everything from fraud detection and risk scoring to transaction routing and compliance monitoring.

Unlike a standard payment backend that processes requests and returns responses, an AI backend continuously learns from transaction data, adapts to emerging patterns, and feeds intelligence into every layer of the payment system that depends on it.

Where Does AI Fit Inside Payment Architecture?

Building a scalable AI fintech backend requires placing intelligence at every critical junction. Modern systems move beyond simple “if-then” logic. They use neural networks to evaluate transactions as they happen. Consequently, every payment becomes an opportunity to optimize for speed and cost.

This placement ensures that your infrastructure can handle millions of concurrent requests. In addition, it creates a robust layer that protects your capital from market volatility. Therefore, AI becomes the central nervous system of your entire financial operation.

1. Transaction scoring before authorization

The first point of contact is the pre-authorization layer. Here, the backend calculates a risk score for the incoming request.

- Behavioral analysis: It checks if the user’s current session matches their history.

- Device fingerprinting: The system identifies the hardware to stop automated bot attacks.

- Fund prediction: It estimates the likelihood of a successful bank response.

- Instant filtering: High-risk requests are blocked before they hit the gateway. This proactive approach saves you from unnecessary processing fees. Furthermore, it preserves your reputation with acquiring banks.

2. Dynamic routing across gateways

Smart routing is the core of any scalable AI fintech backend. The system chooses the best bank for each transaction in real-time.

- Success optimization: It selects gateways with the highest current uptime.

- Cost management: The AI finds the path with the lowest interchange fees.

- Regional logic: Transactions stay within specific jurisdictions to meet local laws.

- Load balancing: Traffic is spread across providers to prevent system crashes. Therefore, your platform remains operational even during bank outages. This strategy directly maximizes your successful transaction volume.

3. Fraud detection during payment flow

Detection must happen within milliseconds of a live payment. The AI monitors for subtle signals that human analysts might miss. It tracks navigation speed and unusual purchase patterns across the network.

However, it does this without adding friction for legitimate users. This balance is critical for maintaining high conversion rates at checkout. Consequently, your enterprise stays secure while your customers enjoy a fast experience.

4. Smart retries for failed payments

A failed payment does not have to be a lost sale. AI identifies which declines are due to temporary technical issues.

- Code intelligence: The backend reads error codes to determine the cause.

- Perfect timing: It schedules retries for when bank systems are most stable.

- Gateway hopping: The system re-attempts the payment through a different provider.

- Resource efficiency: It stops retries on hard declines like “stolen card.” In addition, these automated workflows reduce the need for manual customer support intervention.

5. Merchant and customer risk signals

The architecture continuously scans for long-term risks across your platform. It looks for spikes in chargebacks or suspicious merchant payout patterns. By analyzing these signals, the AI can freeze risky funds before they leave the ecosystem.

This protects you from massive losses in the event of a merchant default. Therefore, risk management shifts from a reactive chore to a proactive advantage.

Implementing AI at these touchpoints ensures your platform is ready for global scale. It removes the bottlenecks that typically slow down enterprise financial growth.

What Makes A Payment Backend Scalable?

Building a scalable AI fintech backend hinges on decoupling every part of the transaction lifecycle.

This elasticity ensures that your costs stay aligned with your actual revenue. In addition, it prevents a single point of failure from taking down your entire network. Therefore, scalability is the foundation of long-term operational stability and profit growth.

1. Event-driven payment processing

In an event-driven model, the system reacts to specific triggers instead of following a rigid sequence. For example, a “payment initiated” event triggers the fraud check and routing engines simultaneously.

- Asynchronous flows: Tasks run in parallel to reduce the total processing time.

- Loose coupling: Changing one service does not break the rest of the stack.

- Real-time updates: Webhooks push status changes to merchants without constant polling.

- Audit trails: Every event creates a permanent record for compliance and debugging. Consequently, your backend can process thousands of events per second without bottlenecking the CPU.

2. Stateless payment services

A scalable AI fintech backend must treat every request as an independent unit. Stateless services do not store user session data on the local server. Instead, they pull the necessary context from a distributed cache like Redis.

This approach allows any server in your cluster to handle any incoming request. Furthermore, it makes upgrading the system much easier because you can replace individual nodes without losing data. Therefore, your platform gains the flexibility needed for rapid global expansion.

3. Horizontal scaling across workloads

Vertical scaling has a hard ceiling and high costs. Horizontal scaling allows you to add more low-cost instances to handle growing traffic.

- Auto-scaling groups: The system automatically adds servers during peak shopping holidays.

- Workload isolation: You can scale the fraud engine independently from the reporting tool.

- Resource efficiency: You only pay for the computing power you are currently using.

- Global distribution: Deploy instances closer to your users to reduce network latency. In addition, this strategy ensures that your infrastructure grows in lockstep with your user base.

4. Queue-based transaction handling

Traffic spikes can easily overwhelm a database if requests hit it all at once. Use message queues like Kafka or RabbitMQ to buffer incoming transaction data. This protects your core services from being flooded during high-velocity events.

The backend processes messages at its own pace while maintaining a smooth experience for the end user. However, the system still confirms the receipt of the request to the merchant immediately. Consequently, you maintain high availability even during extreme load conditions.

5. Resilient failover and recovery

Scalability is useless if the system cannot recover from a localized crash. Modern backends use multi-region deployments to ensure constant availability. If one data center goes dark, traffic automatically shifts to a healthy region.

- Health checks: The system constantly monitors the “heartbeat” of every service.

- Circuit breakers: It stops sending requests to a failing service to prevent a total crash.

- Data replication: Financial records are mirrored across multiple zones in real-time.

- Instant recovery: Automated scripts restart failed processes without human intervention. Therefore, your enterprise can confidently guarantee 99.99% uptime to your high-value clients.

A scalable backend turns infrastructure into a competitive advantage. It allows you to enter new markets and handle massive volumes without rebuilding your technology.

Core Features Of An AI Payment Backend

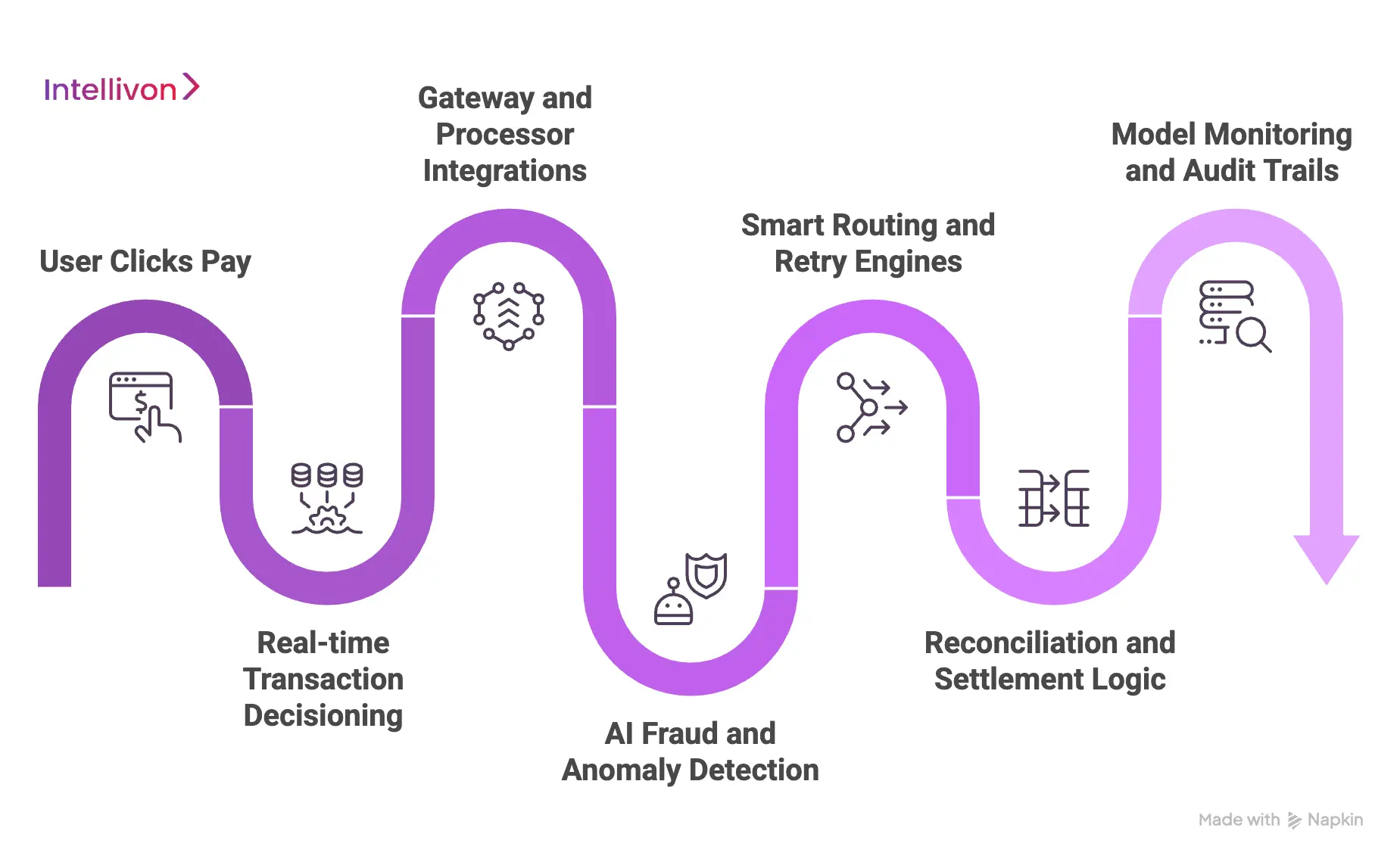

A robust, scalable AI fintech backend must provide more than just a connection to a bank. It acts as an intelligent middleware that manages the entire lifecycle of every transaction. This includes everything from the moment a user clicks “pay” to the final bank reconciliation.

Furthermore, these features must be built as modular services to allow for easy updates. This flexibility ensures your platform can adapt to new payment methods or regulations. Consequently, your architecture remains future-proof while delivering immediate value to your bottom line.

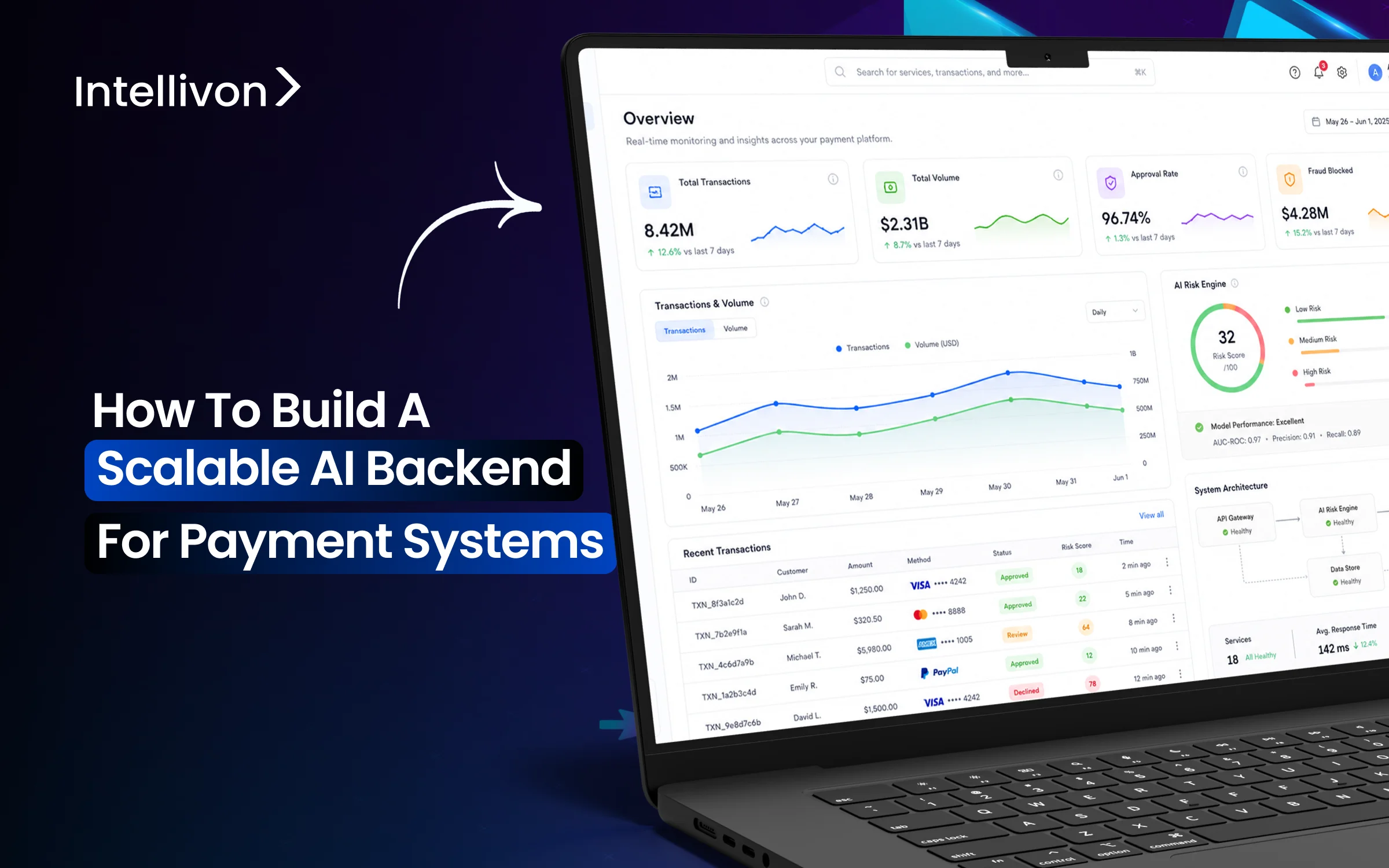

1. Real-time transaction decisioning

Speed is the most critical factor in modern digital commerce. Your backend must make complex decisions in under 200 milliseconds.

- Contextual evaluation: The system analyzes the user, amount, and merchant history instantly.

- Pre-authorization checks: It verifies account standing before engaging the gateway.

- Latency management: Optimized code ensures that AI logic does not slow down the checkout.

- Elastic throughput: The decision engine scales up to handle thousands of requests per second. Therefore, customers enjoy a seamless experience that feels instantaneous.

2. Gateway and processor integrations

A scalable AI fintech backend serves as a unified entry point for multiple financial networks. It simplifies the complexity of managing different APIs and data formats.

- Universal API: Developers use one set of tools to access dozens of global banks.

- Tokenization services: Sensitive card data is replaced with secure tokens for safety.

- Protocol translation: The system converts modern JSON requests into legacy banking formats.

- Multi-currency support: It handles foreign exchange calculations and settlements automatically. In addition, this abstraction layer allows you to swap providers without changing your front-end code.

3. AI fraud and anomaly detection

Legacy fraud rules are too rigid for today’s sophisticated cyber-attacks. Modern backends use machine learning to identify patterns that indicate a high risk of chargebacks.

- Velocity tracking: The system flags a sudden burst of transactions from a single IP.

- Geographic profiling: It detects unusual cross-border activity that deviates from normal behavior.

- Supervised learning: Models are trained on millions of historical fraud cases to improve accuracy.

- Anomaly alerts: The AI triggers manual reviews for transactions that look suspicious but are not certain. However, it does this while maintaining low false-positive rates to avoid blocking legitimate customers.

4. Smart routing and retry engines

Failed transactions represent a massive source of leaked revenue for most fintechs. An intelligent backend uses data to ensure every payment finds the path of least resistance.

- Performance routing: It automatically sends traffic to the gateway with the highest success rate.

- Adaptive retries: The system waits for the perfect millisecond to re-attempt a soft decline.

- Failover logic: If a primary processor goes down, the system shifts traffic in real-time.

- Fee-based optimization: It prioritizes the routing path that costs your business the least. Consequently, you recover lost sales and improve your overall authorization percentages.

5. Reconciliation and settlement logic

Managing the books is often the most labor-intensive part of running a payment platform. AI automates the matching of gateway reports with your internal ledger.

- Automated matching: The system identifies discrepancies between expected and actual deposits.

- Fee calculation: It tracks every cent of interchange and processing fees for transparency.

- Dispute management: AI helps categorize and respond to chargebacks more efficiently.

- Payout orchestration: It manages the timing and logic of merchant settlements across regions. Therefore, your finance team can focus on strategy instead of manual data entry.

6. Model monitoring and audit trails

In a regulated industry, you must be able to explain why an AI made a specific decision. Your backend needs a comprehensive logging system for every model output.

- Explainable AI: The system records the features that led to a fraud score or a route.

- Drift detection: It monitors if model performance is degrading over time as markets change.

- Version control: You can roll back to a previous model if a new update causes issues.

- Full audit logs: Every transaction has a detailed history for compliance and regulatory reviews. In addition, this transparency builds trust with auditors and high-value enterprise partners.

These features provide the technical foundation for a truly global financial enterprise. They turn your payment infrastructure into a self-optimizing asset that grows with your business.

How To Design The Backend Architecture?

Building a scalable AI fintech backend involves a modular approach where each layer serves a distinct purpose. This design prevents the system from becoming a rigid monolith that is difficult to update.

Each layer communicates through secure protocols to maintain data integrity and regulatory compliance. Consequently, your platform remains resilient against both traffic spikes and security threats. Therefore, a structured architecture is the most critical investment for long-term technical debt reduction.

1. API gateway for payment requests

The gateway acts as the secure front door for every transaction entering your ecosystem. it manages authentication, rate limiting, and initial request validation before any processing begins.

- Kong or NGINX: Used for high-performance traffic management and load balancing.

- AWS API Gateway: Provides managed scaling and integrated security features.

- Auth0 or Okta: Handles sophisticated identity management and OAuth flows.

- gRPC: Enables low-latency communication between the gateway and internal services. In addition, this layer protects your internal services from malicious external traffic.

2. Microservices for payment modules

Isolating specific functions into microservices allows you to scale and update components independently. For instance, the ledger service can scale separately from the notification service.

- Go (Golang): Chosen for its superior concurrency handling in financial applications.

- Docker and Kubernetes: Used for containerization and automated service orchestration.

- Spring Boot: Provides a robust framework for building secure, enterprise-grade Java services.

- Istio: Manages a service mesh for secure inter-service communication and observability. Therefore, your development team can deploy updates faster without risking the entire system.

3. Streaming layer for real-time events

A streaming layer ensures that data moves instantly between services without creating bottlenecks. It allows for asynchronous processing of tasks like fraud checks and ledger updates.

- Apache Kafka: The industry standard for high-throughput, fault-tolerant event streaming.

- Confluent: Provides an enterprise-grade distribution of Kafka with enhanced monitoring.

- Amazon Kinesis: A managed service for real-time data processing at scale.

- RabbitMQ: Used for complex message routing and task queuing between services. Consequently, your backend can handle massive transaction bursts with zero data loss.

4. Feature store for AI signals

The feature store is the bridge between your raw data and your machine learning models. It provides a centralized repository of pre-calculated signals used for real-time decision-making.

- Feast: An open-source feature store that manages data for model training and serving.

- Tecton: A fully managed enterprise feature platform for production-grade AI.

- Redis: Serves as the low-latency online store for sub-millisecond feature retrieval.

- Pinecone: A vector database used for complex pattern matching in fraud detection. This layer ensures your AI models always have access to fresh, accurate data points.

5. Decision engine for payment actions

The decision engine is the “brain” that orchestrates the logic for routing, fraud, and retries. It combines hard business rules with predictive outputs from your AI models.

- TensorFlow Serving: Used for deploying high-performance machine learning models in production.

- Python (FastAPI): A high-speed framework for serving AI model predictions.

- Drools: A powerful rules engine for managing complex business logic and compliance.

- PyTorch: Often used for developing and running deep learning fraud detection models. In addition, this setup allows for rapid A/B testing of different routing strategies.

6. Data warehouse for reporting

The data warehouse stores historical transaction data for long-term analysis and regulatory reporting. It allows your business team to run complex queries without slowing down the live payment flow.

- Snowflake: A cloud-native warehouse that scales storage and compute independently.

- Google BigQuery: Enables serverless, highly scalable analysis of petabytes of data.

- Amazon Redshift: A fast, fully managed data warehouse for enterprise-level reporting.

- dbt (data build tool): Used for transforming raw data into clean, actionable insights. Therefore, your leadership team can make data-driven decisions based on real-time financial trends.

This architecture provides the reliability and speed required by modern enterprises. It creates a foundation that supports both current operations and future AI-driven innovations.

Which AI Models Power Payment Systems?

Modern payment backends rely on a diverse ensemble of machine learning models. These models work in parallel to evaluate risk and optimize costs for every transaction.

Consequently, enterprise leaders must understand which models drive specific business outcomes within their stack. Therefore, a multi-model strategy is the most effective way to build a resilient and intelligent financial platform.

1. Fraud risk scoring models

These models are the primary defense against unauthorized transactions and identity theft. They must process hundreds of variables in milliseconds to assign a risk probability.

- XGBoost: Highly effective for tabular data and identifying complex fraud patterns.

- Random Forest: Provides excellent stability and handles missing data points well.

- LightGBM: Optimized for speed and low memory usage in high-volume environments.

- Neural Networks: Used for capturing non-linear relationships in massive datasets. In addition, these models are constantly retrained to adapt to evolving criminal tactics.

2. Payment failure prediction models

Predicting a failure before it happens allows the backend to take preemptive action. These models analyze historical gateway performance and card-specific success rates.

- Logistic Regression: Useful for binary classification tasks like “success” or “fail.”

- Decision Trees: Help map out the specific conditions that lead to transaction declines.

- CatBoost: Handles categorical data like bank names and merchant IDs without extensive preprocessing.

- K-Nearest Neighbors (KNN): Identifies similar past transactions to predict the current outcome. This foresight allows the system to choose a more reliable routing path immediately.

3. Merchant risk intelligence models

Enterprises must monitor the health of the merchants using their platform to avoid credit risk. These models look for sudden shifts in volume or rising chargeback trends.

- Time-Series Analysis (ARIMA/Prophet): Predicts future transaction volumes and detects deviations.

- Isolation Forests: Specifically designed to find outliers in merchant behavior.

- Support Vector Machines (SVM): Effective for classifying merchants into different risk tiers.

- Bayesian Networks: Help model the causal relationships between market events and merchant stability. Consequently, you can adjust payout schedules or reserve requirements based on real-time risk scores.

4. Customer behavior models

Understanding how a legitimate customer typically acts helps reduce friction for “good” users. These models create a unique behavioral profile for every account holder.

- Recurrent Neural Networks (RNNs): Analyze the sequence of actions a user takes over time.

- LSTMs: Excellent for remembering long-term habits while identifying short-term anomalies.

- Clustering (K-Means): Groups users by spending habits to detect sudden, uncharacteristic purchases.

- Deep FM: Combines low-order and high-order features for better personalized risk assessment. Therefore, you only trigger multi-factor authentication when the behavior significantly deviates from the norm.

5. Routing optimization models

The goal here is to find the most cost-effective and reliable path for the money. These models function like a GPS for the global financial network.

- Reinforcement Learning (RL): The model learns the best routing strategies through constant trial and error.

- Linear Programming: Optimizes for specific constraints like cost or settlement time.

- Genetic Algorithms: Useful for finding optimal solutions in complex, multi-gateway environments.

- Gradient Boosting Machines: Predict the most likely successful gateway for specific card types. In addition, these models can automatically react to bank outages faster than any human operator.

6. Anomaly detection models

Anomaly detection focuses on finding “unknown unknowns” that traditional fraud models might miss. It identifies patterns that simply do not fit the established baseline of the network.

- Autoencoders: A type of neural network that learns to compress and reconstruct normal data.

- One-Class SVM: Identifies data points that fall outside the boundary of normal transactions.

- Local Outlier Factor (LOF): Measures the local density deviation of a specific transaction.

- Gaussian Mixture Models: Model the distribution of normal traffic to find statistical outliers. However, these models require careful tuning to ensure they do not flag legitimate market growth as a threat.

The right mix of models ensures your backend is both defensive and offensive. It protects your capital while simultaneously finding new ways to increase your operational margins.

How To Make AI Payments Secure And Compliant?

Modern payment systems must balance aggressive automation with strict regulatory adherence. You cannot simply layer AI over a weak security framework. Instead, security must be baked into every microservice and model training loop.

Consequently, your backend becomes a fortress that supports global growth without compromising integrity. Therefore, focusing on compliance is a strategic move that builds long-term enterprise value.

1. PCI DSS-ready data handling

Any scalable AI fintech backend must meet the highest standards for Payment Card Industry Data Security Standards (PCI DSS). This involves isolating the environment where sensitive cardholder data is processed.

- Network Segmentation: Keeps payment data physically and logically separate from the rest of the business.

- Encrypted Storage: Ensures that any stored data is unreadable to unauthorized parties.

- Vulnerability Management: Regularly scans the backend for potential entry points.

- Formal Security Policies: Establishes clear protocols for how data is handled by employees. In addition, these practices simplify the auditing process for your compliance team.

2. Tokenization and encryption layers

Tokenization replaces sensitive data with a unique, non-sensitive identifier called a token. This process ensures that your AI models never actually “see” a customer’s real credit card number.

- AES-256 Encryption: The gold standard for protecting data while it is at rest.

- TLS 1.3: Secures data while it is moving between the customer and the backend.

- Hardware Security Modules (HSM): Physical devices that manage and protect digital keys.

- Format Preserving Encryption: Keeps data in a usable format for AI without exposing the secret. Therefore, a data breach would only reveal useless tokens rather than valuable financial information.

3. Role-based access and approvals

Security is often compromised by internal human error rather than external attacks. Implementing strict access controls ensures that staff only see the data they need for their specific job.

- Least Privilege Principle: Users get the minimum level of access required for their tasks.

- Multi-Factor Authentication (MFA): Requires at least two forms of ID for all system logins.

- Just-In-Time Access: Grants temporary permissions that expire after a specific time.

- Multi-Party Approvals: Requires two different managers to authorize high-value changes or payouts. Consequently, you minimize the “blast radius” of any single compromised internal account.

4. Data residency and retention controls

Global payments mean dealing with diverse laws like GDPR in Europe or CCPA in California. Your scalable AI fintech backend must know exactly where data is stored and when to delete it.

- Geofencing: Ensures data stays within the geographic borders required by local laws.

- Automated Purging: Deletes user data automatically once the legal retention period ends.

- Right to Erasure: Provides tools to quickly remove a customer’s information upon request.

- Data Masking: Hides personal details during the AI model training process. In addition, these controls help you avoid the heavy penalties associated with international data privacy violations.

5. Explainable AI decision logs

Regulators now require firms to explain why an automated system rejected a transaction or flagged a merchant. You cannot hide behind a “black box” algorithm in the financial world.

- Feature Attribution: Records which data points had the most influence on a specific AI score.

- Audit-Ready Reports: Generates logs that prove your models are not biased against specific groups.

- Model Versioning: Tracks exactly which version of an algorithm made a decision in the past.

- Reason Codes: Provides clear explanations that customer service teams can share with users. However, this transparency must be maintained without slowing down the real-time processing speed.

Compliance is the ultimate shield for your innovation. By building these security layers into your backend, you create a platform that is ready for the most regulated markets in the world.

How To Integrate With Existing Payment Stacks?

Building a scalable AI fintech backend often involves working alongside systems that are decades old. The goal is to create a modern orchestration layer that communicates with legacy cores without friction.

Consequently, your enterprise gains the benefits of innovation without the chaos of a total “rip-and-replace” project. Therefore, seamless integration is the most practical path toward financial modernization.

1. Mapping current payment workflows

Before writing a single line of code, you must document every touchpoint in your existing money movement process. This visibility is essential for identifying where AI can provide the most immediate impact.

- Data Silo Audit: Locate where transaction history and customer metadata are currently stored.

- Latency Benchmarking: Measure the current time taken for authorization and settlement.

- Failure Point Analysis: Identify which gateways or banks have the highest decline rates.

- Dependency Mapping: Understand how your current ledger interacts with external reporting tools. In addition, this map helps your team ensure that no critical compliance steps are missed during the upgrade.

2. Connecting gateways and processors

Your new backend must act as a universal translator for all your existing banking relationships. It should consolidate multiple disparate APIs into a single, clean data stream.

- Adapter Pattern: Create custom code modules that bridge the gap between AI and legacy APIs.

- Unified Schema: Standardize all incoming transaction data into a common format for the AI.

- Credential Vaulting: Securely manage API keys and certificates for all your current processors.

- Webhooks Integration: Set up real-time listeners to capture status updates from external banks. Therefore, your internal teams can manage all financial flows through one central, intelligent dashboard.

3. Building APIs around legacy systems

Legacy cores are often rigid and difficult to access directly. The solution is to build a modern API wrapper that exposes the necessary functions to your AI engine.

- RESTful Envelopes: Wrap old SOAP or file-based protocols in modern, easy-to-use APIs.

- Shadow Ledgers: Maintain a real-time digital twin of your legacy ledger for faster AI processing.

- Throttling Controls: Ensure the AI does not overwhelm older systems with too many requests.

- Error Translation: Map cryptic legacy error codes into actionable data for your retry engine. Consequently, you unlock the power of your existing data without needing to rebuild the core banking logic.

4. Migrating without payment downtime

Zero downtime is the gold standard for any enterprise-grade financial migration. You can achieve this by running your new backend in parallel with your old one.

- Canary Deployments: Route a tiny percentage of traffic to the AI backend to test performance.

- Blue-Green Switching: Maintain two identical environments to allow for instant failover if issues arise.

- Database Synchronization: Keep your new and old databases in perfect sync during the transition.

- Phased Rollouts: Move one merchant or one region at a time to contain any potential risks. In addition, this cautious approach builds confidence among your stakeholders and high-value clients.

5. Testing routing before rollout

Simulation is the safest way to ensure your AI routing logic actually improves your bottom line. Use historical data to “replay” past transactions through the new intelligent engine.

- Backtesting Engines: Compare AI routing decisions against the actual paths taken in the past.

- Load Testing: Simulate extreme traffic spikes to see how the integrated stack handles the pressure.

- Regression Suites: Ensure that new AI features do not break existing settlement or reporting logic.

- A/B Testing Loops: Run two different routing models simultaneously to see which performs better. However, you must ensure that all test data is properly anonymized to maintain security.

A well-executed integration turns your legacy systems into a source of strength rather than a limitation. It allows you to leverage your existing data to fuel the AI models of the future.

How To Build For Agentic Payments?

Building a scalable AI fintech backend for agentic flows means enabling software to spend money on behalf of users. Unlike simple automation, AI agents make subjective decisions based on changing market conditions.

This transformation allows businesses to automate procurement, treasury management, and even customer refunds without human intervention. Consequently, your architecture becomes a truly autonomous financial operating system.

1. Agent authorization and consent flows

Agents need a specialized way to prove they have the right to move funds. Standard passwords are insufficient for software that might need to execute thousands of micro-payments.

- OAuth for Agents: Uses scoped tokens that define exactly what an agent can and cannot do.

- Cryptographic Keys: Employ unique digital signatures for every agent-led request.

- Time-Bound Consent: Limits the agent’s power to a specific window of time.

- Revocation Endpoints: Provides an instant “kill switch” to stop an agent if it malfunctions. In addition, these flows must be user-friendly so non-technical owners can easily manage permissions.

2. Mandate-based payment approval

Instead of approving every single dollar, users set broad mandates that guide the agent’s behavior. The scalable AI fintech backend then enforces these rules in real-time.

- Variable Recurring Payments: Allows agents to pull different amounts based on usage.

- Smart Contracts: Use programmable logic to trigger payments only when conditions are met.

- Dynamic Mandates: Adjusts spending limits based on the agent’s recent performance.

- Conditional Logic: For example, “Buy more inventory only if the price is below $50.” Therefore, you maintain control over the “what” and “why” while the agent handles the “when.”

3. AI agent identity verification

You must be able to verify that a payment request came from a trusted AI and not a malicious bot. This involves creating a “Know Your Agent” (KYA) protocol similar to traditional banking.

- Agent Fingerprinting: Identifies the specific model version and source code of the agent.

- Behavioral Baselines: The AI backend flags if an agent starts acting outside its usual patterns.

- Reputation Scoring: Tracks the history of an agent to determine its reliability.

- Verified Registries: Uses centralized databases to confirm the identity of third-party agents. Consequently, your platform remains secure even in a world of millions of autonomous actors.

4. Limits, controls, and spend rules

The backend must act as a rigid guardian to prevent an agent from draining an account during an error. These controls are the most important part of an agentic, scalable AI fintech backend.

- Daily Velocity Limits: Caps the total amount an agent can spend in 24 hours.

- Merchant Whitelisting: Restricts the agent to specific, pre-approved vendors.

- Balance Thresholds: Stops all agent activity if the account balance hits a certain level.

- Step-Up Alerts: Requires a human to approve any transaction that exceeds a specific value. However, these rules must be flexible enough to allow the agent to function without constant interruptions.

5. Audit trails for agent-led payments

If an agent makes a mistake, you need a forensic record of why it chose to spend that money. Traditional logs are not enough; you need the reasoning behind the action.

- Inference Logging: Records the specific prompt or data point that triggered the payment.

- Chain-of-Thought Logs: Tracks the internal logic steps the AI agent followed.

- Immutable Ledgers: Uses blockchain-inspired technology to ensure logs cannot be altered.

- Dispute Resolution Packs: Automatically compile all evidence needed if a payment is contested. In addition, these trails are vital for proving to regulators that your autonomous systems are under control.

Building for agents is about building trust. When your infrastructure can safely manage autonomous money, you unlock a new level of scale that was previously impossible.

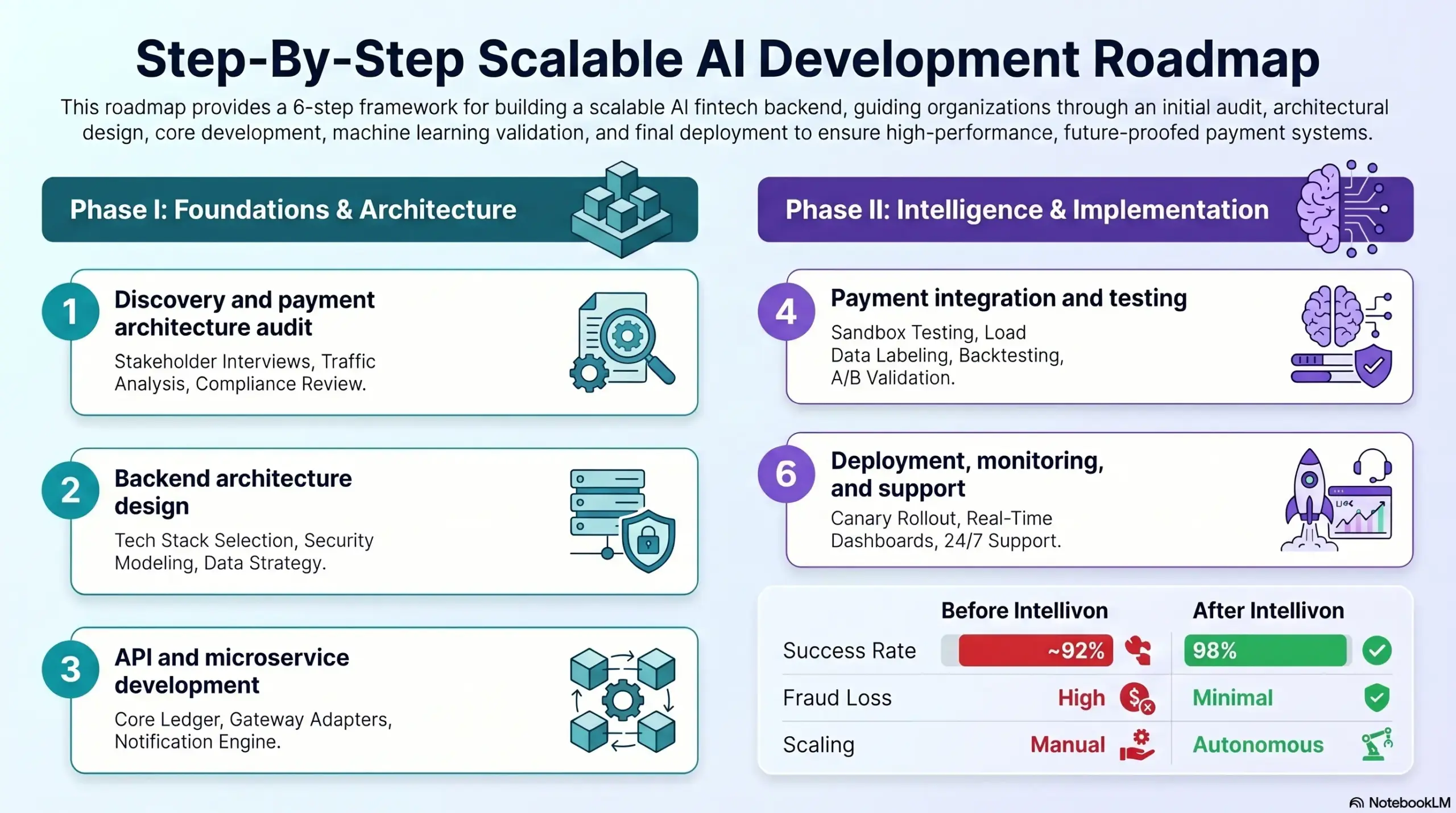

Step-By-Step Scalable AI Development Roadmap

A successful transition to an intelligent financial infrastructure requires a disciplined, multi-phase approach. Our process at Intellivon ensures that every technical decision aligns with your long-term business goals.

Building a scalable AI fintech backend is a journey from legacy constraints to autonomous efficiency. We follow a rigorous framework designed to mitigate risk while maximizing performance.

Therefore, following a proven roadmap is the safest way to future-proof your payment business.

1. Discovery and payment architecture audit

The first step is a deep dive into your existing technical landscape. We identify bottlenecks and security gaps that could hinder your future growth.

- Stakeholder Interviews: We align with your CFO and CTO on key performance indicators.

- Traffic Analysis: We study your peak volume patterns to design for elastic scaling.

- Compliance Review: Our team ensures your data handling meets local and global standards.

| Feature | Legacy Audit | Intellivon AI Audit |

| Focus | Maintenance | Optimization |

| Goal | Patching Gaps | AI Readiness |

| Output | Status Report | Integration Blueprint |

2. Backend architecture design

We create a customized blueprint for your scalable AI fintech backend. This stage focuses on decoupling services to ensure that a failure in one area does not stop the money flow.

- Tech Stack Selection: We choose the best languages and databases for your specific volume.

- Security Modeling: We design the tokenization and encryption layers from the ground up.

- Data Strategy: We plan how real-time events will flow into your AI feature store.

In addition, we prioritize low-latency designs that ensure sub-second transaction responses.

3. API and microservice development

Our engineering team builds the core modules that will power your financial transactions. We use a microservices approach to allow for independent scaling of each feature.

- Core Ledger: Developing the immutable record-keeping system for every cent moved.

- Gateway Adapters: Building secure bridges to your existing processors and banks.

- Notification Engine: Ensuring real-time webhooks keep your merchants informed.

Consequently, your backend becomes a flexible ecosystem rather than a rigid block of code.

4. AI model training and validation

We develop and fine-tune the machine learning models that provide the “intelligence” in your stack. This involves using your historical data to teach the system how to spot fraud and optimize routes.

- Data Labeling: Identifying successful and fraudulent transactions to train the models.

- Backtesting: Running the models against past data to verify their predictive accuracy.

- A/B Validation: Testing different algorithms to find the most profitable configuration.

Therefore, your AI is battle-tested before it ever touches a live customer transaction.

5. Payment integration and testing

Testing in a fintech environment must be exhaustive. We simulate millions of transactions to ensure the system remains stable under extreme market pressure.

- Sandbox Testing: Validating all API calls in a secure, non-live environment.

- Load Testing: Pushing the architecture to its breaking point to find and fix bottlenecks.

- Edge Case Analysis: Testing how the system handles rare errors like network timeouts.

In addition, we conduct rigorous security audits to ensure your data remains impenetrable.

6. Deployment, monitoring, and support

The final phase is a controlled rollout that ensures zero downtime for your active users. Once live, our autonomous monitoring tools keep a constant eye on system health.

- Canary Rollout: Gradually shifting traffic to the new backend to monitor performance.

- Real-Time Dashboards: Providing your team with a clear view of success rates and costs.

- 24/7 Support: Ensuring expert help is always available to manage your global operations.

| Metric | Before Intellivon | After Intellivon |

| Success Rate | ~92% | >98% |

| Fraud Loss | High | Minimal |

| Scaling | Manual | Autonomous |

Our process is designed to turn your vision into a high-performance reality. We handle the technical complexity so you can focus on expanding your market share.

Conclusion

Building a scalable AI backend is a necessity for surviving today’s massive transaction surge. Modernized systems recover lost revenue through smarter orchestration and real-time reliability. Therefore, your enterprise requires a platform that prioritizes high-stakes architectural stability.

Moving beyond legacy constraints ensures your operations remain profitable even during peak demand. This strategic shift transforms your technical foundation into a powerful engine for long-term global expansion.

Why Build Your AI Payment Backend With Intellivon?

Building a scalable AI backend for payment systems requires more than connecting models to transaction data. It needs a secure payment intelligence layer where transaction processing, fraud scoring, routing logic, risk controls, compliance workflows, and real-time monitoring work together without slowing down payment performance.

At Intellivon, we build AI-ready backend systems for fintech platforms, PSPs, digital banks, marketplaces, SaaS businesses, lenders, insurers, and enterprises that need payment infrastructure built for high volume, low latency, and intelligent decision-making.

A. Designing Backend Architecture For High-Volume Payments

Payment systems need a backend architecture that can handle speed, reliability, and risk at the same time. We design scalable backend foundations that support transaction processing, AI scoring, payment orchestration, and operational visibility from day one.

- Microservices for transaction, fraud, routing, and reconciliation workflows

- Event-driven architecture for real-time payment data movement

- API-first backend design for gateways, PSPs, and internal systems

- Horizontal scaling to handle transaction spikes and peak payment loads

This gives your payment system a backend that can grow without creating performance bottlenecks.

B. Building Real-Time AI Decision Engines

AI payment systems must make decisions while the transaction is still active. We build real-time decision engines that score payments, detect fraud, recommend routing actions, trigger retries, and escalate risky transactions instantly.

- Low-latency scoring APIs for fraud, risk, and payment failures

- Rules engines that combine AI outputs with business logic

- Decision workflows for approve, block, retry, route, or review actions

- Feedback loops that improve model performance over time

This helps your backend support intelligent payment decisions without delaying authorization or checkout completion.

C. Creating Secure Payment Data Pipelines

AI models are only as strong as the payment data behind them. We build secure data pipelines that collect, clean, enrich, and move transaction signals from gateways, processors, issuer responses, fraud tools, dispute systems, and customer behavior sources.

- Real-time event streams for transaction and gateway activity

- Data enrichment for issuer, device, customer, and merchant signals

- Tokenized and encrypted payment data flows

- Structured datasets for fraud, routing, recovery, and analytics models

This gives your AI backend the data foundation it needs to make accurate decisions at scale.

D. Scaling Fraud, Risk, And Routing Workflows

A scalable AI backend must support multiple payment workflows without forcing every decision into one model. We build modular systems where fraud scoring, risk checks, routing decisions, failed payment recovery, and chargeback signals operate as connected backend services.

- Fraud scoring services for live transaction risk

- Smart routing logic across gateways, PSPs, acquirers, and rails

- Failed payment recovery workflows for subscriptions and recurring billing

- Chargeback and dispute intelligence for payment operations teams

This allows your payment backend to expand AI use cases without rebuilding the entire system each time.

Build Your AI Payment Backend With Intellivon

If your payment system needs to support higher transaction volume, smarter fraud decisions, better routing, faster recovery, and stronger operational control, Intellivon can help you build the backend infrastructure behind it.

Contact Intellivon to discuss your payment backend architecture, AI use cases, scalability goals, and the infrastructure your platform needs to process payments securely at scale.

FAQs

Q1. What makes an AI backend scalable for payment systems?

A1. A scalable AI payment backend can handle high transaction volume, real-time scoring, fraud checks, routing decisions, retries, and monitoring without slowing payment performance. It usually needs microservices, event streams, queue systems, cloud infrastructure, and strong failover logic.

Q2. How can AI make payment backends more intelligent?

A2. AI helps payment backends score fraud risk, predict failed payments, route transactions, detect anomalies, automate reviews, and improve approval rates. Instead of only processing transactions, the backend starts making smarter decisions across risk, performance, and revenue recovery.

Q3. Will AI affect payment backend latency?

A3. AI can affect latency if it is poorly designed. A production-ready backend uses low-latency APIs, cached signals, timeout rules, fallback paths, and asynchronous processing where needed. This keeps AI decisions fast enough for live payment flows.

Q4. What security is needed for an AI payment backend?

A4. An AI payment backend needs tokenization, encryption, API security, access controls, audit logs, PCI-aware data flows, and model monitoring. These controls protect sensitive payment data while keeping fraud, routing, and risk decisions traceable for compliance teams.