Key Takeaways:

- Legacy gateways use rigid if-then logic that cannot adapt to fraud patterns, false declines, or multi-PSP routing complexity at scale.

- AI adds fraud scoring, smart routing, failed payment prediction, and chargeback intelligence through APIs and middleware without replacing the existing gateway.

- Smart retry logic classifies soft and hard declines separately, predicts optimal retry windows, and triggers backup payment methods before customers notice a failure.

- Integration costs range from $15,000 for a fraud scoring layer to $120,000 and above for a full AI payment decision layer with routing and governance.

- How Intellivon integrates AI into existing payment gateways your enterprise fully owns, with real-time scoring, fallback logic, and compliance-ready audit trails built in.

For large enterprises, the payment gateway is a system that settlement teams, compliance officers, fraud analysts, and many downstream systems rely on every day. Interacting with it carries organizational risk. This is why, as AI capabilities in payments have developed, the main concern is how to do so without disrupting what already works.

The challenge is not whether AI should be part of your payment stack. Competitors are using it to lower fraud losses, increase authorization rates, and reduce operational costs that old rule-based systems cannot handle effectively. The real question is how to incorporate that intelligence into a live, regulated, multi-system environment. A misconfigured integration can lead to a technical error, a failed transaction, a compliance issue, or damage to your reputation.

At Intellivon, we assist enterprises facing this exact challenge, where environments where uptime is essential, compliance is monitored, and the integration cannot interfere with the payment flows crucial to the business. In this blog, we will explore the architectural approaches, integration patterns, and governance factors that enable large enterprises to integrate AI into existing payment gateways without the need to rebuild from the ground up.

Why Payment Gateways Need An AI Upgrade

The payment industry is past the experimentation phase with AI. Across fraud prevention, authorization decisioning, and transaction routing, enterprises that have embedded AI into their payment infrastructure are seeing measurable gains, which leads to lower fraud loss rates, higher approval ratios, and operational costs that legacy rule-based systems could never achieve. The ones that have not are starting to feel the gap.

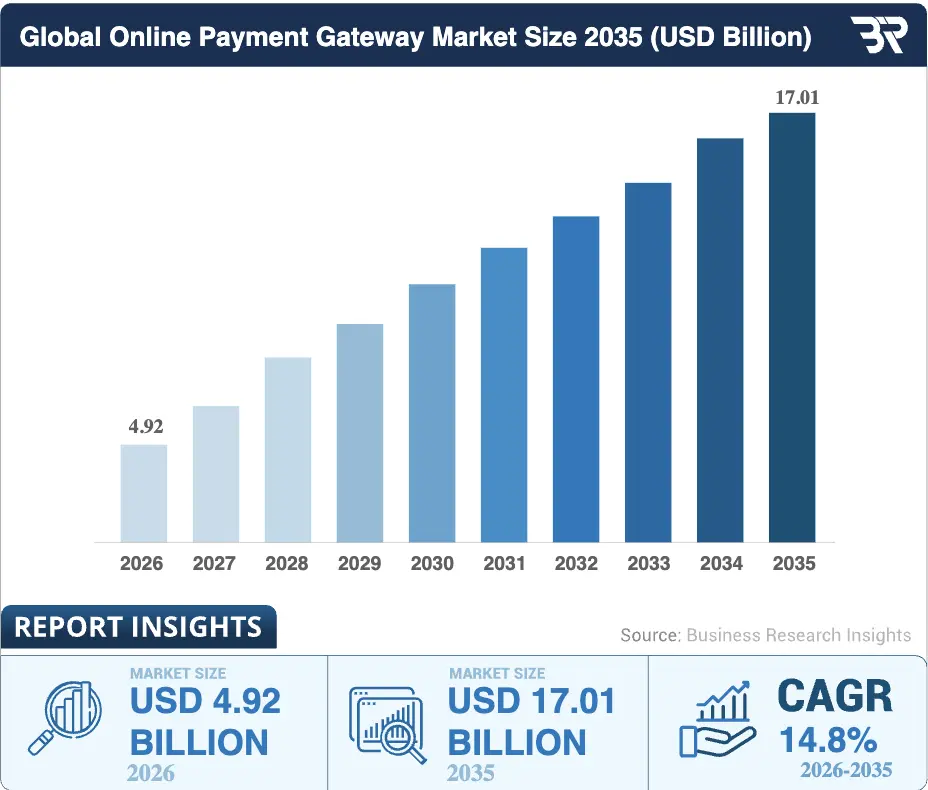

The online payment gateway market is valued at USD 4.92 billion in 2026 and is projected to reach USD 17.01 billion by 2035, growing at a CAGR of 14.8%. The infrastructure layer that moves and secures money is being rebuilt, and the platforms being built today are the ones that will capture that growth.

Existing payment gateways need AI to reduce fraud, improve approvals, route transactions better, recover failed payments, and support real-time risk decisions. Here is why:

1. Payment gateways were not built for AI decisions

Most legacy gateways operate on rigid code written decades ago. These systems use basic “if-then” logic to process every transaction. Consequently, they cannot learn from new data or adapt to shifting market trends. This technical debt prevents enterprises from offering truly personalized checkout experiences.

Furthermore, it limits your ability to respond to complex financial patterns in real time. AI adds a cognitive layer that evaluates every payment contextually.

2. Fraud rules create false declines at scale

Generic fraud filters often treat legitimate customers like high-risk attackers. For example, a customer shopping while traveling may face an immediate block. These false positives cause direct revenue loss and frustrate your most loyal users.

Therefore, relying on static rules actually costs more than the fraud you are trying to prevent. AI uses behavioral analysis to verify identities without adding friction. This ensures that genuine transactions flow through while genuine threats are stopped instantly.

3. Payment failures reduce recurring revenue

Subscription businesses suffer when payments fail due to minor technical glitches. Most gateways simply retry the card at a random time the next day. However, this blind approach often leads to a high rate of permanent churn.

AI analyzes bank response codes and historical data to find the optimal retry window. Because of this, you can recover significant revenue that would otherwise be lost. It turns a passive process into a strategic recovery tool.

4. Multi-PSP setups need smarter routing

Using multiple payment providers is essential for redundancy in large enterprises. However, choosing the right provider for each specific transaction is incredibly difficult. Manual routing rules are too slow to account for real-time downtime or changing fees.

An AI engine evaluates the health of every provider for every single click. It then directs the payment to the most cost-effective and reliable path available. As a result, your success rates stay high regardless of provider performance.

5. Manual reviews slow down payment operations

Human teams cannot manually inspect every flagged transaction in a high-volume environment. This creates massive backlogs that delay order fulfillment and impact the customer experience. In addition, manual reviews are prone to human error and inconsistent decision-making.

AI automates these complex workflows by applying deep learning to your historical data. Therefore, your experts only spend time on the most unusual cases. This increases efficiency while drastically lowering the cost of your payment operations.

Upgrading your gateway is a fundamental business strategy that protects your margins and improves customer retention.

What Does AI Payment Gateway Integration Mean?

AI payment gateway integration means adding fraud scoring, smart routing, risk checks, personalization, monitoring, and automation to existing payment workflows.

AI payment gateway integration means embedding machine learning models and intelligent decisioning capabilities directly into the transaction layer of a payment system.

The result is a payment infrastructure that does not just move money, but actively protects and optimizes every transaction that flows through it.

AI As A Payment Decision Layer

This layer acts as a sophisticated filter between your checkout page and the processing bank. It evaluates the risk and value of every request.

By analyzing millions of past transactions, it predicts the likelihood of a successful and safe completion. This ensures your infrastructure is proactive rather than reactive.

- Real-time Risk Scoring: The system assigns a trust score to every transaction within milliseconds.

- Dynamic Authentication: It decides when to trigger extra security steps like 3D Secure based on risk.

- Behavioral Analysis: The layer tracks how a user interacts with the page to find bot patterns.

- Automated Policy Enforcement: It applies global compliance rules without requiring manual updates from your team.

Therefore, the decision layer transforms your gateway into a strategic asset. It protects your revenue while simultaneously reducing the friction for your legitimate customers.

Difference Between Gateway AI and Orchestration

Many leaders confuse basic gateway AI with full-scale payment orchestration. While both use data, they serve very different roles in your enterprise strategy.

Gateway AI focuses on the internal health of a single provider. In contrast, orchestration manages your entire network of multiple global providers.

| Feature | Gateway AI | Payment Orchestration |

| Primary Goal | Optimizing a single provider | Managing multiple providers |

| Scope | Internal fraud and risk | Global routing and redundancy |

| Control | Locked to one ecosystem | Provider-agnostic control |

| Scalability | Limited to one partner | Unlimited global expansion |

Understanding this distinction is crucial for your long-term infrastructure planning. You must decide if you need to fix one pipe or manage the entire plumbing system.

Where AI Fits In The Payment Lifecycle

AI provides value at every stage of a transaction, from the first click to the final settlement. It is not a single tool but a series of checkpoints that improve the whole experience.

Consequently, every department, from marketing to finance, benefits from these automated insights.

- Pre-Authorization: AI checks for stolen credentials and bot activity before the bank is even contacted.

- During Authorization: The system selects the best bank route to ensure the highest chance of approval.

- Post-Authorization: It handles reconciliation and identifies patterns in chargebacks to prevent future losses.

- Retention Phase: Smart retry logic attempts to save failed subscriptions at the perfect moment for the user.

Integrating AI across the entire lifecycle creates a seamless loop of continuous improvement. Each transaction teaches the system how to handle the next one more efficiently.

Build AI Without Replacing The Gateway

AI can be added to existing gateways through middleware, scoring APIs, event streams, routing logic, and observability layers without disrupting live payments.

Enterprises often hesitate to upgrade their financial stacks because they fear significant downtime. However, modern integration methods allow you to add intelligence without ripping out your current infrastructure. You can enhance your existing systems while maintaining 100% uptime for your customers.

1. Keep the existing gateway in place

Your current gateway likely has deep ties to your accounting and logistics software. Replacing it entirely would be a massive and risky undertaking for any stable enterprise.

Instead, you can treat your existing gateway as a reliable and familiar utility. AI sits on top of this foundation to handle the complex decision logic. This approach preserves your established banking relationships and merchant IDs perfectly.

2. Add middleware between checkout and gateway

Middleware acts as a smart bridge that intercepts transaction data before it hits the processor. This layer performs the heavy lifting of analysis without slowing down the user experience.

It allows you to run complex simulations and risk checks in parallel. Because the middleware is decoupled, you can update your AI models at any time. This flexibility ensures your system stays ahead of emerging global fraud trends.

3. Use APIs for real-time scoring

Application Programming Interfaces (APIs) provide a lightweight way to inject intelligence into your flow. When a user enters their details, an API call sends the metadata to an AI engine.

The engine returns a risk score or a routing suggestion in milliseconds. This modularity means you only use the AI features you actually need. Consequently, you avoid the bloat and cost of a full platform migration.

4. Stream payment events into AI models

Modern AI thrives on the continuous flow of data from your live environment. By streaming transaction events, you create a feedback loop that improves over time. Every success and every decline teaches the model how to better predict future outcomes.

This streaming architecture ensures your models are never working with stale or outdated information. Therefore, your decision-making remains sharp even during high-traffic seasonal sales events.

5. Route decisions back into payment flows

Once the AI makes a decision, it must be injected back into the transaction path. This might involve choosing a specific 3D Secure protocol or selecting a secondary processor.

These micro-adjustments happen behind the scenes without the customer ever noticing a change. This automated orchestration ensures every payment follows the path of least resistance. It maximizes your authorization rates while effectively minimizing your processing fees.

6. Preserve the current checkout experience

The most important factor for conversion is a smooth and familiar checkout process. AI integration should never force a redesign of your frontend user interface. Because the intelligence lives in the backend, the user sees no change in the interface.

They only experience faster approvals and fewer frustrating false declines during their purchase. Maintaining this visual consistency is vital for brand trust and long-term customer retention.

This modular strategy removes the technical debt associated with legacy payment migrations. It allows your business to innovate at high speed while keeping your core operations stable.

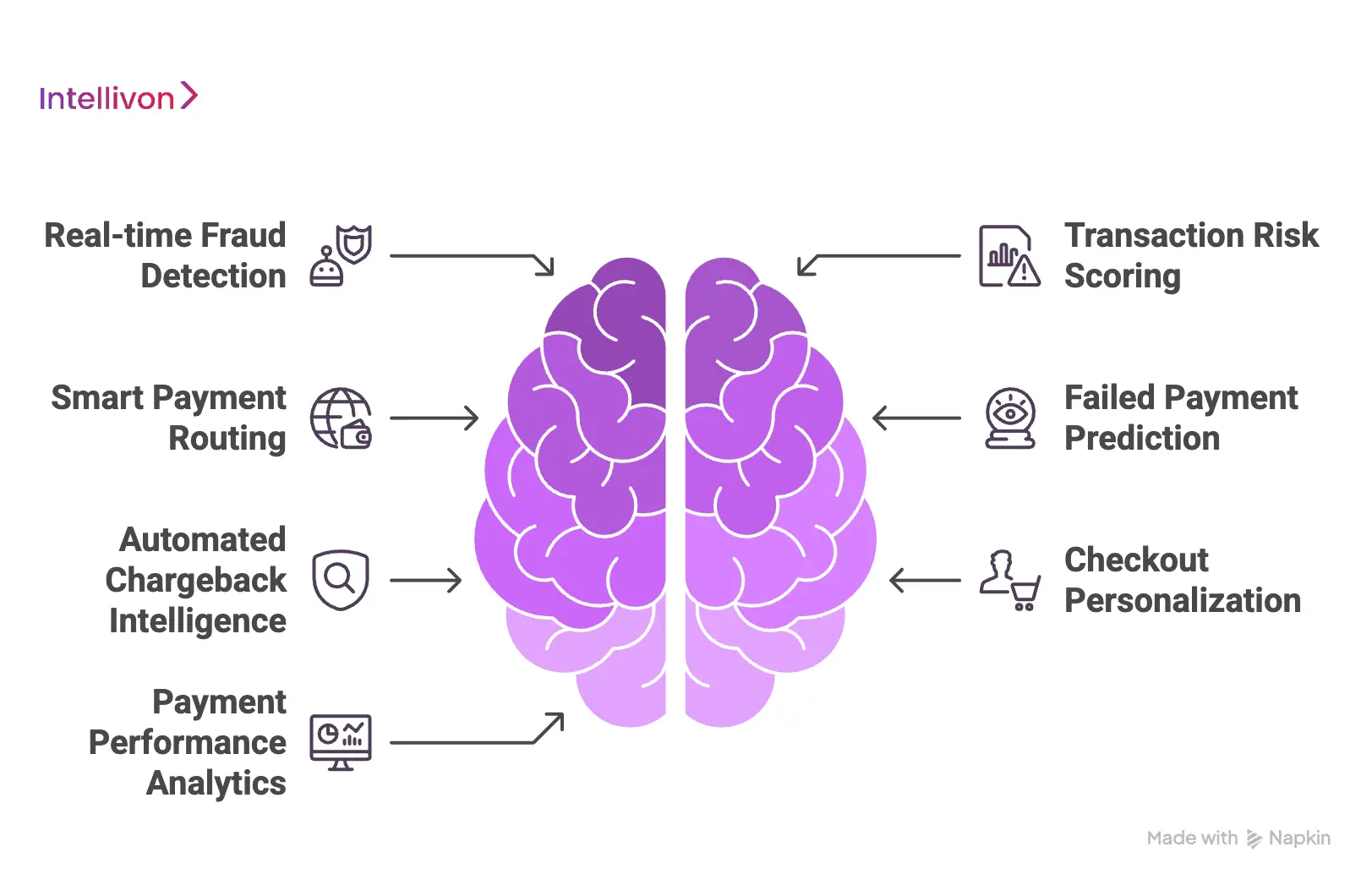

Which AI Features Can You Add To Gateways?

Existing payment gateways can be upgraded with AI fraud detection, risk scoring, payment routing, retry logic, personalization, dispute automation, and analytics.

Upgrading a financial stack with AI involves deploying specialized modules that target specific operational leaks. Instead of a single monolithic update, organizations can implement focused features that resolve unique friction points.

These enhancements transform a passive gateway into an active engine for revenue protection through a strategic AI integration payment approach.

1. Real-time fraud detection

Legacy fraud detection often relies on static blacklists or basic geographic filters. In contrast, AI identifies sophisticated attacks by analyzing behavioral patterns across millions of sessions.

This approach detects anomalies like automated credential stuffing or synthetic identity creation before the transaction finishes.

- Behavioral Monitoring: The system tracks mouse movements and typing speeds to distinguish humans from bots.

- Device Fingerprinting: It recognizes returning devices even when users change their IP addresses or browsers.

- Velocity Checks: AI monitors the speed of transactions across the entire network to stop coordinated attacks.

2. Transaction risk scoring

Risk scoring replaces the “pass/fail” binary with a nuanced probability model for every payment. This allows the system to apply different levels of friction based on the calculated risk level.

Consequently, high-trust users enjoy a frictionless experience while suspicious requests face additional verification.

- Multi-factor Triggers: The system only requests 3D Secure or biometric checks for medium-risk scores.

- Confidence Thresholds: Merchants can set custom limits to balance security against conversion goals.

- Contextual Data: Scores incorporate external factors like global merchant trends and current cyber-threat levels.

3. Smart payment routing

Global enterprises often struggle with varying bank acceptance rates across different regions. Smart routing uses machine learning to select the best acquiring bank for every individual payment.

This decision happens in real time based on the highest probability of authorization.

- Bank Health Monitoring: The AI detects if a specific processor is experiencing downtime or latency.

- Cost Optimization: It routes transactions through the most affordable path without sacrificing speed.

- Regional Specialization: Payments go to local banks to avoid the high decline rates of cross-border processing.

4. Failed payment prediction

Many payment failures are predictable and preventable with the right data modeling. Instead of waiting for a decline, AI anticipates issues like insufficient funds or temporary network errors.

Therefore, the system can adjust its strategy before the user sees an error message.

- Intelligent Retries: The system calculates the exact minute at which a retry is most likely to succeed.

- Payment Method Swaps: AI suggests an alternative payment method if the primary one shows signs of failure.

- Churn Mitigation: It identifies users at risk of leaving due to payment friction and offers assistance.

5. Automated chargeback intelligence

Managing disputes manually is an expensive and time-consuming burden for finance teams. AI automates the evidence collection process and predicts the likelihood of winning a specific case. This allows the business to focus efforts on disputes that are worth the investment.

- Evidence Aggregation: The system pulls transaction logs and delivery receipts automatically into a single file.

- Fraud Identification: It highlights “friendly fraud” patterns where customers falsely claim they did not receive goods.

- Success Forecasting: Machine learning models estimate the win rate for every dispute based on historical outcomes.

6. Check out personalization

A static checkout experience often ignores the unique preferences of global customers. AI analyzes demographics and past behavior to present the most relevant payment options. This level of customization reduces cart abandonment and increases the average order value.

- Localized Methods: The checkout dynamically displays popular local wallets or “buy now, pay later” options.

- One-Click Optimization: It identifies returning customers and prioritizes their preferred saved cards.

- Currency Conversion: The system displays accurate local pricing while optimizing the backend exchange rates.

7. Payment performance analytics

Traditional reporting often lacks the depth needed to make strategic business decisions. AI-driven analytics uncover hidden patterns in payment data that human analysts might miss.

These insights help leaders understand exactly where revenue is being lost or gained.

- Trend Detection: The software identifies sudden drops in acceptance rates for specific card types.

- Anomaly Alerts: Finance teams receive instant notifications when transaction volumes deviate from the norm.

- Revenue Attribution: AI tracks how specific payment optimizations contribute to the overall bottom line.

Implementing these features creates a resilient payment architecture that adapts to market volatility. Modern payment stacks now prioritize AI integration for payment and orchestration to maintain a competitive edge in a crowded digital landscape.

When Should You Integrate AI Into Payments?

Enterprises should integrate AI when fraud losses, payment failures, manual reviews, poor authorization rates, or gateway fragmentation affect revenue and operations.

Deciding the right time for a technical overhaul requires a clear assessment of operational bottlenecks. Enterprises must determine if current infrastructures can support aggressive growth without sacrificing security or efficiency.

1. High transaction volumes

Manual monitoring becomes impossible once a business scales beyond a certain monthly transaction threshold. High volumes increase the surface area for sophisticated attacks that human teams cannot spot in real time.

- Automated Oversight: Systems provide consistent high-level scrutiny without slowing down the transaction pipeline.

- Scalability: Machine learning handles sudden surges in traffic during peak seasons without requiring additional headcount.

- Consistency: Every payment undergoes identical analysis, removing the variability of human judgment.

Consequently, the cost of oversight begins to outweigh the benefits of manual control in high-growth environments.

2. Fraud rules creating false declines

Static rules often penalize legitimate customers because they do not fit a narrow behavioral profile. If a significant percentage of declines are actually honest buyers, current logic is likely too blunt.

- Nuanced Assessment: An AI integration payment strategy allows for accurate risk scoring based on thousands of variables.

- Brand Protection: Reducing false positives prevents the damage to customer trust that occurs during a blocked checkout.

- Adaptive Learning: Models update automatically to recognize new legitimate shopping patterns, such as cross-border travel.

Therefore, moving away from rigid rules directly improves customer lifetime value and global conversion rates.

3. Payment failures impacting revenue

Consistent payment failures are a primary driver of involuntary churn in subscription-based models. A system that cannot distinguish between a temporary network glitch and a permanent card error is outdated.

- Predictive Retries: AI identifies the optimal window to re-attempt a transaction based on historical bank behavior.

- Active Recovery: Intelligent systems recover funds by correcting minor data discrepancies before the final decline.

- Churn Mitigation: Lowering failure rates ensures that recurring revenue streams remain stable and predictable.

4. Fragmented gateway or PSP setups

Managing a fragmented payment stack across different regions creates massive complexity for finance and tech teams. Without a unified intelligence layer, it is difficult to effectively compare performance or route traffic.

- Unified Orchestration: A smart layer shifts volume to the most successful provider at any given moment.

- Global Resilience: Operations remain stable even if a specific regional provider faces a localized outage.

- Cost Efficiency: Automatic routing ensures transactions follow the most affordable path available.

5. Demand for faster risk decisions

A growing backlog of pending transactions indicates that internal processes are reaching their limit. If risk teams spend hours on manual reviews, sales are lost, and customers become frustrated.

- Instant Processing: AI provides decisions in milliseconds by evaluating data points that humans cannot process at speed.

- High-Stakes Focus: Experts can pivot their energy to complex investigations rather than routine approvals.

- Operational Velocity: Faster decisions lead to quicker fulfillment and improved cash flow across the organization.

6. Data readiness for model training

Effective machine learning requires a healthy foundation of historical transaction data. If an organization has spent years collecting clean and structured data, it is positioned for the next step.

- Custom Modeling: Businesses can leverage existing logs to build models reflecting specific industry risks.

- Strategic Advantage: Clean data allows for the deployment of specialized AI agents that optimize the entire payment lifecycle.

- Future Proofing: Establishing these models now prepares the infrastructure for future shifts in global commerce.

Identifying these triggers early allows a business to pivot before operational inefficiencies become permanent roadblocks. These signs indicate that payment infrastructure is no longer a support function but a strategic priority.

How Does AI Work Inside A Payment Gateway?

AI works inside payment gateways by collecting transaction data, scoring risk in real time, triggering decisions, routing payments, and learning from outcomes.

The mechanical process of an AI integration payment system operates behind the scenes in milliseconds between a click and a confirmation. Rather than a single static check, the architecture functions as a high-speed pipeline that evaluates, routes, and learns from every transaction.

This practical framework ensures that intelligence is applied at the exact moment of financial impact.

1. Transaction data ingestion

The process begins by capturing a broad spectrum of data points as soon as a user initiates a checkout. Traditional systems only look at card numbers and expiry dates, but AI-enabled gateways ingest much more.

This includes metadata like IP addresses, browser types, session durations, and even the cadence of the user’s keystrokes.

- Holistic Inputs: The system gathers environmental data that goes beyond the basic transaction amount.

- Speed Requirements: Ingestion happens in real time to ensure there is no noticeable latency for the customer.

- Data Enrichment: External signals, such as global blacklists or currency fluctuations, are pulled in to add context.

2. Feature engineering for payment signals

Raw data must be converted into “features” or signals that a machine can understand. For example, a single transaction from a new city is just a data point.

However, comparing that city to the user’s last ten purchases creates a meaningful signal about potential fraud.

- Signal Identification: AI identifies patterns such as “velocity,” which tracks how many times a card is used in an hour.

- Behavioral Baselines: The system compares current actions against the typical behavior of a specific user segment.

- Historical Comparison: Features are built by looking at months of past transaction logs to spot anomalies.

3. Real-time scoring APIs

Once features are ready, they are sent to a scoring engine via high-speed APIs. This engine produces a numerical value that represents the risk level or the likelihood of authorization. These scores are generated almost instantly, allowing the gateway to make a split-second decision before contacting the bank.

- Dynamic Probability: Scores move on a sliding scale rather than a simple “yes” or “no.”

- Custom Thresholds: Businesses can adjust their risk appetite based on product type or seasonal goals.

- API Efficiency: The communication between the gateway and the AI model is optimized for sub-second responses.

4. Rules and AI decision engines

The decision engine combines the AI score with the specific business rules of the organization.

While the AI provides the “probability,” the decision engine provides the “action.” This might involve allowing the payment, requesting a secondary verification, or routing it to a different processor entirely.

- Hybrid Logic: This layer balances the predictive power of AI with the hard constraints of legal compliance.

- Automated Action: The engine can trigger a 3D Secure challenge only when the score hits a specific danger zone.

- Policy Flexibility: Rules can be updated instantly to react to a sudden surge in a specific type of cyberattack.

5. Feedback loops from payment outcomes

The most critical part of the architecture is the feedback loop. Once the bank either approves or declines the payment, that result is fed back into the AI model.

If a transaction was flagged as safe but later resulted in a chargeback, the model learns from that mistake to prevent it from happening again.

- Closed-Loop Learning: The system constantly refines its accuracy based on real-world successes and failures.

- Ground Truth: Actual bank responses serve as the “correct answers” that train the next generation of models.

- Continuous Improvement: The gateway becomes more intelligent with every single dollar processed.

6. Monitoring model accuracy and drift

Market conditions change, and so does fraud behavior; this is known as “model drift.” An effective AI integration payment setup includes continuous monitoring to ensure the intelligence remains sharp over time.

If the model starts blocking too many legitimate users, the system alerts engineers to retrain the algorithm.

- Performance Tracking: Analysts monitor the “False Positive” rate to ensure the AI isn’t becoming too aggressive.

- Automatic Retraining: Modern pipelines can trigger new training cycles when accuracy dips below a certain level.

- Transparency: Dashboards provide visibility into why certain decisions were made, ensuring the “black box” of AI remains accountable.

This architecture turns a simple financial bridge into a self-optimizing ecosystem. It ensures that the payment infrastructure is always moving at the speed of global commerce while maintaining the highest levels of security.

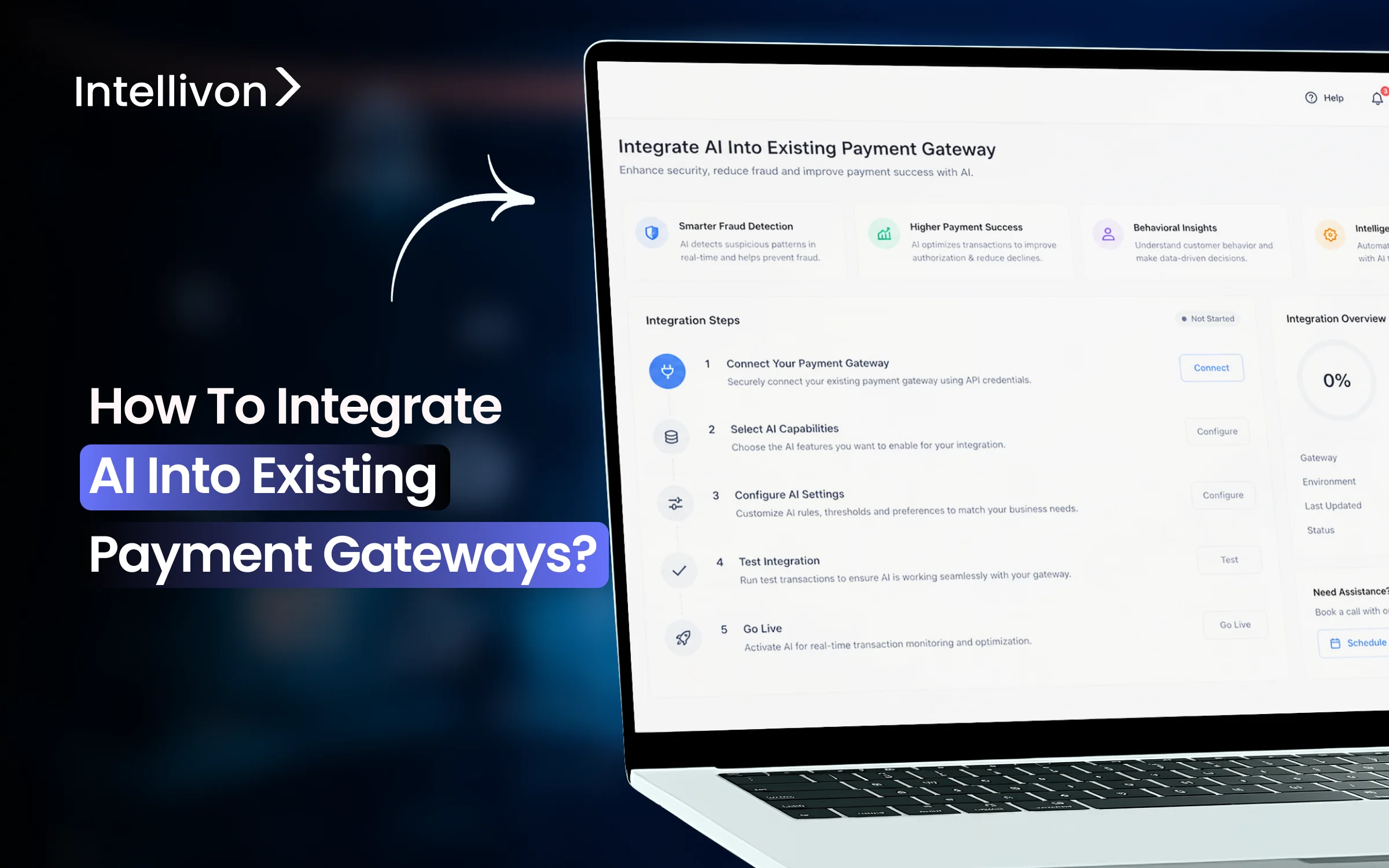

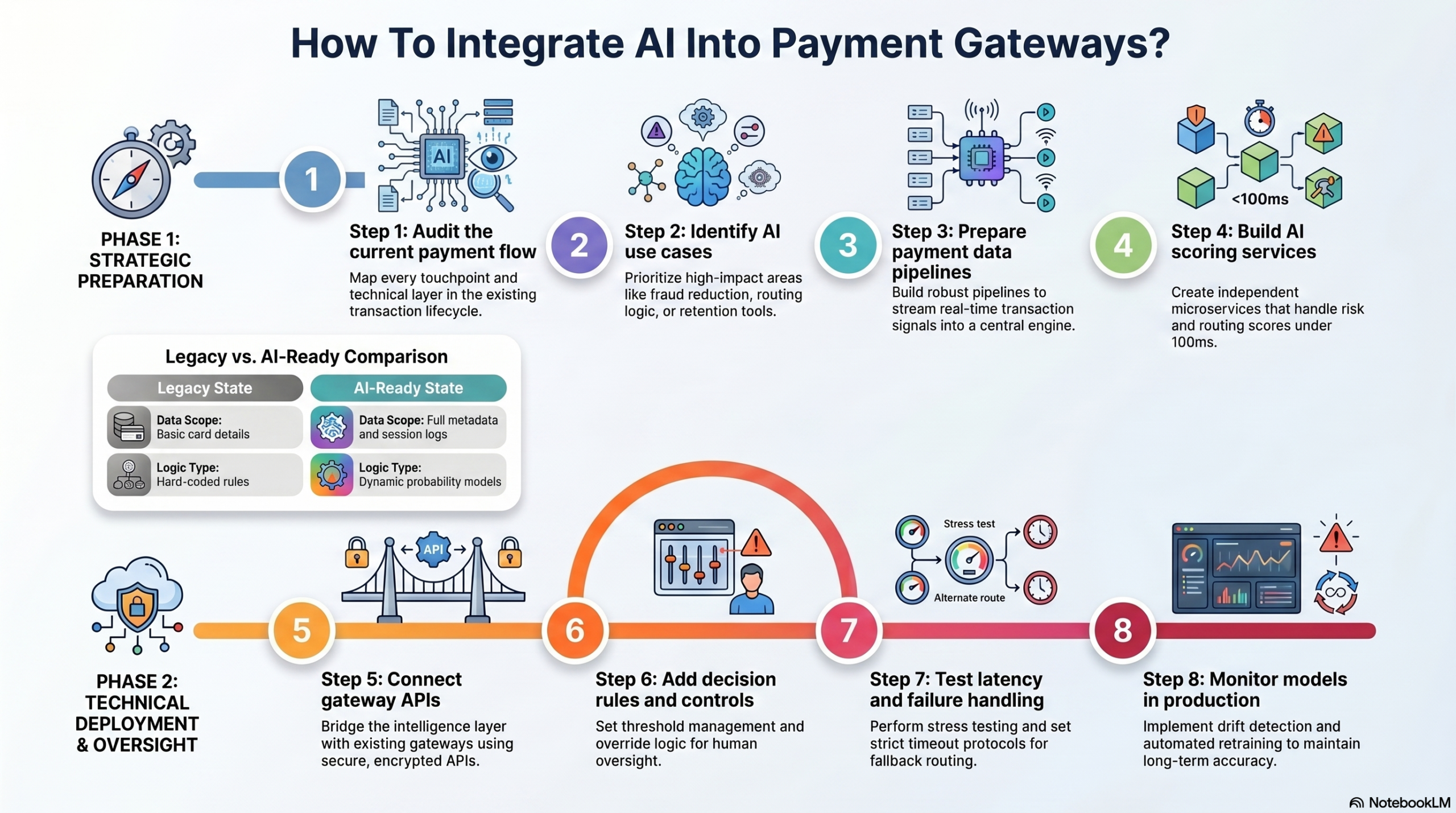

How To Integrate AI Into Payment Gateways?

AI can be integrated into payment gateways through APIs, middleware, orchestration layers, event streams, fraud engines, and real-time decision systems.

Implementing a strategic AI integration payment approach requires a structured methodology to ensure security and stability. Organizations must move through these stages carefully to avoid disrupting live cash flows.

At Intellivon, this eight-step framework serves as our blueprint for deploying enterprise-grade AI into existing financial stacks.

Step 1: Audit the current payment flow

The process begins with a comprehensive map of every touchpoint in the existing transaction lifecycle. We document how data moves from the checkout page to the final settlement bank. Understanding these technical layers helps identify where latency occurs and where data is being lost.

- API Mapping: Identify every call made between internal servers and external payment providers.

- Success Benchmarking: Establish baseline authorization rates and fraud levels for comparison.

- Dependency Check: Document which internal systems rely on the current gateway output.

| Audit Focus | Legacy State | AI-Ready State |

| Data Scope | Basic card details | Full metadata and session logs |

| Logic Type | Hard-coded rules | Dynamic probability models |

Step 2: Identify AI use cases

Not every payment problem requires a complex machine learning model. We focus on prioritizing the highest-impact areas, such as reducing false declines or optimizing routing. Decisions must be made whether to focus on top-line revenue growth or bottom-line cost reduction first.

- Fraud Reduction: Target high-risk regions with advanced behavioral biometrics.

- Routing Logic: Focus on transactions with the highest processing fees.

- Retention Tools: Apply smart retry logic to recurring billing cycles to prevent churn.

Step 3: Prepare payment data pipelines

AI is only as effective as the data it consumes in real time. We build robust pipelines that stream transaction events into a central processing engine. Clean, structured data ensures that models remain accurate and do not produce biased results.

- ETL Processes: Extract, transform, and load historical data to train the initial models.

- Real-time Streaming: Set up event buses to capture live transaction signals instantly.

- Data Enrichment: Integrate third-party signals like IP reputation and global threat intelligence.

Step 4: Build AI scoring services

The core intelligence layer is developed by creating specialized microservices that handle risk and routing scores. These services must be highly available and respond in under 100 milliseconds. Building these as independent units allows for easy updates without affecting the entire payment stack.

- Model Selection: Choose between supervised learning for fraud or reinforcement learning for routing.

- Training Loops: Use historical logs to teach the system successful patterns.

- Probability Outputs: Ensure every service provides a clear numerical score for decision-making.

Step 5: Connect gateway APIs

Once the intelligence layer is ready, it must be bridged with the existing gateway via secure APIs. This connection allows the AI to receive data and send back actionable instructions. This integration maintains PCI-DSS compliance and high data encryption standards.

- Tokenization: Ensure sensitive card data remains encrypted while the AI analyzes metadata.

- Webhook Integration: Set up listeners to receive instant status updates from the provider.

- API Throttling: Implement safeguards to prevent overwhelming the gateway during traffic peaks.

Step 6: Add decision rules and controls

An AI integration payment system needs a “control room” where leaders set boundaries. This layer combines the AI score with the specific risk tolerance of the organization. It allows for human oversight over automated decisions to ensure brand safety and compliance.

- Threshold Management: Define exactly what score triggers an automatic block or review.

- Override Logic: Create “fail-safe” rules if the AI service becomes unavailable.

- A/B Testing: Run AI logic in “shadow mode” against existing rules to compare performance.

Step 7: Test latency and failure handling

Payments are time-sensitive, so any added intelligence must not slow down the checkout process. Rigorous load testing ensures the system handles thousands of concurrent transactions without crashing. Failure handling protocols ensure payments still go through if the AI layer stalls.

- Stress Testing: Simulate extreme traffic spikes to find the breaking point of the bridge.

- Timeout Protocols: Set strict limits on how long the gateway waits for an AI score.

- Fallback Routing: Ensure transactions default to a standard path if smart routing fails.

Step 8: Monitor models in production

The final step is continuous oversight to ensure the system remains accurate as market conditions shift. Models can “drift” over time as fraudsters change tactics or consumer behavior evolves. Real-time dashboards provide visibility into how the AI impacts the bottom line every hour.

- Drift Detection: Monitor for sudden changes in approval rates, indicating a model error.

- Accuracy Audits: Regularly compare AI predictions against actual bank outcomes.

- Retraining Schedules: Automate the process of updating models with the latest transaction data.

This eight-step methodology ensures that intelligence is added with surgical precision. At Intellivon, we follow this path to modernize your financial core while protecting every cent of revenue. We handle the technical heavy lifting so you can focus on scaling your business with confidence.

What Is The Best AI Integration Architecture?

The best AI payment architecture separates the gateway, AI decision layer, data pipeline, rules engine, monitoring system, and compliance controls.

The most effective financial systems avoid a monolithic design in favor of a modular, decoupled framework. This separation ensures that adding an AI layer does not introduce single points of failure.

By isolating core processing from the decision-making engine, enterprises gain the ability to scale each component independently.

1. AI middleware between app and gateway

Positioning a dedicated middleware layer ensures that the application and the payment provider never communicate in a blind vacuum. This layer acts as a sophisticated interceptor that enriches every request with additional security context.

It allows for complex logic to be executed without modifying the underlying code of the main application.

- Logic Isolation: Core payment code remains clean while the middleware handles the cognitive load.

- Rapid Deployment: New risk models can be pushed to the middleware without a full system reboot.

- Security Perimeter: Sensitive data is filtered and tokenized before it travels to external endpoints.

2. Event-driven payment intelligence layer

An event-driven architecture responds to transaction triggers in real time rather than waiting for scheduled batches. This ensures that the system is always reacting to the most current data available in the financial ecosystem.

Consequently, the speed of decision-making matches the speed of the global markets.

- Asynchronous Processing: Non-critical tasks like analytics happen in the background to keep the checkout fast.

- System Resilience: If one component pauses, the event queue holds data to prevent transaction loss.

- Scalability: The architecture handles massive spikes in volume by distributing events across multiple processors.

3. API-first scoring and routing services

Developing intelligence as a series of APIs ensures that any internal or external tool can benefit from the AI. This modularity allows the finance team to use the same risk scoring for online sales as they do for manual invoices.

It creates a “single source of truth” for risk across the entire organization.

- Standardized Inputs: Every department uses the same data definitions for risk and performance.

- Third-party Compatibility: Standard APIs allow for easy connection to new banks or fraud databases.

- Maintenance Efficiency: Developers can fix or upgrade one specific API without touching the rest of the stack.

4. Data lake for payment intelligence

A central repository for all transaction logs, behavior signals, and bank responses is vital for long-term growth. This data lake provides the raw material needed to train increasingly accurate machine learning models.

Therefore, the system becomes more specialized to the unique needs of the business over time.

- Long-term Analysis: Teams can identify seasonal trends by looking at years of historical data.

- Cross-channel Insights: Data from different platforms is merged to find hidden fraud patterns.

- Audit Readiness: A centralized log makes regulatory compliance and financial auditing much simpler.

5. Human review workflows for risk teams

Even the most advanced AI integration payment setup requires a pathway for human intervention. The architecture must include an interface that presents high-risk cases to experts in a clear and actionable format.

This ensures that unique or complex situations receive the proper attention they deserve.

- Evidence Visualization: Dashboards show the exact data points that led the AI to flag a transaction.

- Efficiency Tools: One-click actions allow reviewers to approve or block payments instantly.

- Feedback Integration: Every human decision is recorded and used to retrain the AI for better future performance.

6. Observability for every payment decision

A high-performing system must be transparent about how and why it makes specific choices. Observability tools track the health of the AI models and the performance of the underlying infrastructure.

This visibility prevents “black box” scenarios where errors could go unnoticed for long periods.

- Real-time Dashboards: Stakeholders can monitor authorization rates and fraud levels as they happen.

- Automated Alerts: The system notifies engineers if latency increases or if model accuracy begins to drift.

- Traceability: Every transaction has a detailed audit trail showing the specific logic used for the outcome.

Building with these principles ensures a robust and future-proof financial core. This modular approach allows for continuous innovation without risking the stability of daily operations.

How To Add AI For Failed Payments in Gateways?

AI helps prevent failed payments by predicting decline risk, identifying retry windows, selecting alternate routes, and improving revenue recovery workflows.

Involuntary churn is often the result of preventable technical errors or poorly timed transaction attempts.

Integrating AI into the recovery process allows a system to move from a passive “wait-and-see” approach to a proactive revenue protection strategy. This shift is particularly vital for businesses relying on consistent recurring billing cycles.

1. Predict payment failure risk

Machine learning models can evaluate the likelihood of a decline before the transaction is even sent to the bank. By analyzing past payment behavior and current balance signals, the system identifies high-risk requests.

Consequently, the business can adjust its strategy, such as delaying the charge, to increase the probability of success.

- Risk Scoring: Assign a success probability to every scheduled billing event.

- Preventative Pausing: Temporarily hold transactions that show a high likelihood of a technical failure.

- Dynamic Data Cleaning: Automatically correct common data entry errors that lead to immediate declines.

2. Classify soft and hard declines

Not all failures are equal, and treating them as such leads to wasted effort and lost customers. AI distinguishes between “hard” declines, such as a reported stolen card, and “soft” declines caused by temporary issues like network timeouts.

This classification ensures the recovery engine applies the most appropriate response for every unique situation.

- Logic Branching: Hard declines trigger immediate customer notification to update payment details.

- Technical Retries: Soft declines are channeled into an automated retry loop without bothering the user.

- Pattern Recognition: The system identifies if a specific bank is experiencing a broad technical outage.

3. Choose the right retry timing

Blindly retrying a failed card at the same time every day is an inefficient strategy that often leads to repeated failures. An AI integration payment model analyzes when a specific customer is most likely to have sufficient funds or when a bank’s servers are most responsive.

Therefore, the system schedules retries at the exact moment they are most likely to be approved.

- Optimal Window Analysis: Timing is adjusted based on local payday cycles and historical success windows.

- Frequency Capping: The engine limits retries to avoid triggering bank fraud alerts or excessive fees.

- Bank-Specific Logic: Retries are tailored to the specific processing habits of different global issuers.

4. Recommend backup payment methods

If a primary card fails repeatedly, the system should intelligently suggest the next best alternative. AI analyzes which backup methods, such as digital wallets or direct bank transfers, have the highest success rates for that specific user.

This reduces the friction of the recovery process and keeps the subscription active.

- Smart Suggestions: The interface prioritizes the alternative method most likely to be authorized.

- Cross-Method Analysis: Models track which combinations of payment types provide the highest overall stability.

- Incentivized Switching: The system can offer a small discount or benefit for moving to a more reliable payment method.

5. Trigger recovery workflows

Automating the communication process ensures that no failed payment falls through the cracks. When a transaction cannot be saved through background retries, the AI triggers a personalized “dunning” workflow.

These communications are timed and phrased based on the user’s past engagement patterns to maximize the response rate.

- Personalized Messaging: Email or SMS notifications are sent when the user is most active online.

- Multi-channel Orchestration: The system moves from email to in-app messages if the first attempt is ignored.

- Urgency Calibration: The tone of communication evolves based on the age of the failed payment.

6. Track recovered revenue by model

To justify the investment, the system must provide clear visibility into exactly how much revenue the AI has saved. Detailed dashboards compare the performance of AI-driven retries against traditional static methods.

This transparency allows stakeholders to see the direct impact on the bottom line and the reduction in churn.

- Success Attribution: Clearly mark which transactions were saved by the intelligent retry engine.

- ROI Dashboards: Monitor the “lift” in revenue provided by the AI integration payment layer.

- A/B Comparison: Regularly run the AI against legacy logic to ensure it continues to provide superior results.

Applying AI to failed payments transforms a major business pain point into a controlled and optimized process. This proactive approach ensures that technical hurdles never stand in the way of long-term customer relationships and stable revenue growth.

How To Secure AI Payment Gateway Systems?

AI payment systems must secure card data, protect APIs, tokenize sensitive information, control model access, and log every payment decision.

Security in an AI integration payment environment must function as a core structural component rather than an auxiliary feature. Because these systems handle sensitive financial data and make autonomous decisions, the security architecture must protect both the data and the logic.

A multi-layered defense ensures that the intelligence layer remains an asset rather than a vulnerability.

1. Tokenize sensitive payment data

Tokenization is the most effective way to remove sensitive cardholder data from the reach of the AI engine. By replacing actual card numbers with unique digital identifiers, the system ensures that the AI never processes raw financial details.

This strategy significantly reduces the scope of PCI-DSS compliance while allowing the models to analyze transaction patterns freely.

- Data Masking: Only non-sensitive metadata, such as transaction frequency or location, is exposed to the machine learning models.

- Vaulting: Original sensitive data is stored in a highly secure, isolated environment away from the primary processing flow.

- Irreversibility: Tokens are designed so they cannot be mathematically reversed to reveal the original card information.

2. Protect AI APIs from misuse

The APIs that connect the gateway to the AI engine are high-value targets for attackers. Securing these endpoints demands continuous monitoring to prevent unauthorized access or automated scraping.

Consequently, protecting these bridges is vital for maintaining the integrity of the entire payment flow.

- Mutual TLS (mTLS): Both the gateway and the AI service must authenticate each other using cryptographic certificates.

- Rate Limiting: Strict quotas prevent malicious actors from attempting to “brute force” the decision logic.

- API Gateway Security: A dedicated security layer inspects every request for signs of injection attacks or suspicious headers.

3. Use role-based access controls

Limiting who can modify AI models or access payment logs is a fundamental security practice. Role-based access ensures that developers, risk analysts, and administrators only see the information necessary for their specific tasks.

Therefore, internal threats and accidental configurations are minimized across the organization.

- Principle of Least Privilege: Users are granted the minimum level of access required to perform their professional duties.

- Multi-factor Authentication: Every entry into the system management console requires a secondary verification step.

- Access Reviews: Permissions are audited regularly to ensure that former employees or temporary contractors no longer have system access.

4. Encrypt data in motion and storage

Encryption provides a critical layer of defense if data is intercepted or if physical storage is compromised. Every piece of information, whether it is a live transaction request or a historical log, must be encrypted using modern cryptographic standards.

This ensures that the data remains unreadable to unauthorized parties at all times.

- End-to-End Encryption: Data is encrypted at the point of capture and only decrypted at the final authorized destination.

- AES-256 Standards: High-grade encryption algorithms protect stored data lakes containing years of payment history.

- Key Management: Cryptographic keys are rotated frequently and stored in hardware security modules (HSMs).

5. Monitor suspicious system behavior

Traditional security looks for known threats, but AI security must look for “behavioral” anomalies within the system itself. If an AI model suddenly starts approving transactions that it usually blocks, it may indicate a “model poisoning” attack.

Continuous monitoring identifies these deviations from the norm before they result in significant financial loss.

- Anomaly Detection: The system flags internal activities that do not align with established operational baselines.

- Real-time Alerts: Security teams receive instant notifications when system performance or decision patterns shift unexpectedly.

- Automated Quarantining: Suspicious processes can be automatically isolated to prevent a potential breach from spreading.

6. Keep audit logs for every decision

In a highly regulated environment, a “black box” is a liability. Maintaining a detailed audit log for every decision made by the AI is essential for accountability and forensic investigation. This log should record exactly what data was used and which model version was active at the time of the transaction.

- Immutable Logs: Audit trails are stored in a format that cannot be deleted or modified by any user.

- Traceability: Every decision, from a fraud block to a routing choice, can be traced back to its specific technical logic.

- Compliance Readiness: Structured logs simplify the process of proving adherence to global financial and privacy regulations.

Integrating these security measures into the heart of the architecture ensures a resilient financial environment. This approach allows enterprises to leverage the power of AI while maintaining the highest standards of trust and data protection.

How Much Does AI Gateway Integration Cost?

AI gateway integration costs usually range from $15,000 to $120,000+, depending on use cases, gateway complexity, payment volume, data quality, compliance needs, and production scale.

The cost of integrating AI into an existing payment gateway depends on how deeply the AI layer connects with your payment flow.

A basic fraud scoring system may only need transaction data, model logic, and a real-time scoring API. However, an enterprise-grade AI payment layer needs much more. It may include smart routing, failed payment recovery, chargeback intelligence, audit trails, fallback logic, dashboards, and model monitoring.

For most businesses, the cost is shaped by one question:

Are you adding one AI feature, or are you building an intelligent payment decision layer around your gateway?

Estimated AI Gateway Integration Cost

| Integration Scope | Estimated Cost Range | Best For |

| AI fraud scoring layer | $15,000–$30,000 | Fintechs, SaaS platforms, and marketplaces are facing rising fraud |

| Failed payment recovery AI | $20,000–$40,000 | Subscription businesses, lenders, insurers, and recurring billing platforms |

| AI chargeback intelligence | $25,000–$45,000 | Payment platforms and merchants with growing dispute volumes |

| Smart routing system | $30,000–$60,000 | PSPs, marketplaces, and platforms using multiple processors |

| Full AI payment decision layer | $60,000–$120,000+ | Enterprises needing fraud, routing, recovery, analytics, and governance |

These ranges give a practical starting point. The final estimate depends on your current gateway setup, existing data infrastructure, transaction volume, and the level of automation required.

A business using one gateway with clean transaction data will usually need a smaller scope. In contrast, an enterprise operating across multiple PSPs, currencies, payment methods, and regions will need a deeper integration.

Failed Payment Recovery Cost

Failed payment recovery AI usually costs between $20,000 and $40,000.

This system predicts which payments are likely to fail, identifies why they failed, and triggers the best recovery action. It is useful for subscription platforms, lending companies, insurance platforms, membership businesses, and B2B SaaS products.

The system may support:

- Soft and hard decline classification

- Retry timing prediction

- Backup payment method prompts

- Customer notification triggers

- Revenue recovery dashboards

- Gateway retry orchestration

- Recovery outcome tracking

This makes failed payment recovery more targeted than standard retry logic.

Cost Factors That Change The Scope

The final cost depends on how complex your current payment ecosystem is.

A simple gateway setup may only require one integration point. However, an enterprise payment environment often includes multiple gateways, PSPs, fraud tools, settlement systems, CRM platforms, finance tools, and internal dashboards.

Key factors that affect cost include:

- Number of gateways and PSPs

- Number of payment methods

- Transaction volume

- Data quality and availability

- Fraud model complexity

- Routing logic complexity

- Compliance and audit requirements

- Need for dashboards and reporting

- Existing API readiness

- Required latency target

- Cloud and infrastructure setup

- Human review workflow requirements

For example, an AI model that only scores card transactions will cost less than a system that supports cards, wallets, bank transfers, UPI, ACH, and real-time payment rails.

Similarly, a dashboard that only shows fraud scores will cost less than a full payment intelligence dashboard that tracks approval rates, routing performance, failed payments, disputes, chargebacks, and recovered revenue.

How Intellivon Estimates Project Cost

At Intellivon, we estimate AI gateway integration cost by studying your existing payment architecture first.

| Integration Scope | Estimated Cost Range | Best For |

| Basic AI fraud scoring | $10,000–$25,000 | Startups and growing fintechs |

| AI routing and retry logic | $25,000–$45,000 | PSPs, SaaS, marketplaces |

| Full AI payment intelligence | $45,000–$80,000+ | Enterprises and payment platforms |

We look at how payments move through your current system, where fraud checks happen, how failures are handled, how routing decisions are made, and what data is available for AI models.

If you want to understand the cost of integrating AI into your existing payment gateway, Intellivon can assess your current payment flow and build a clear implementation roadmap around your business goals.

Real Examples Of AI In Payment Systems

Leading global financial platforms have already shifted from static rules to “AI-native” infrastructures. These organizations demonstrate that AI integration payment strategies are not theoretical experiments but essential tools for maintaining market dominance.

By analyzing these implementations, enterprises can extract high-level lessons for their own digital transformations.

1. Stripe Radar for fraud intelligence

Stripe Radar utilizes a massive global network of transaction data to assign risk scores in real time. Because the system “sees” payments across millions of different businesses, it can identify a stolen card used at a grocery store before it ever reaches your checkout.

This cross-network intelligence allows for a 36% improvement in fraud detection for businesses that provide high-quality metadata.

- Lesson for Enterprises: Data depth is your greatest asset. The more context you provide, such as IP addresses and behavioral signals, the sharper your fraud protection becomes.

2. PayPal AI for transaction risk

PayPal manages over $1.6 trillion in annual payment volume using deep learning models trained over two decades. Their system focuses on “Context-Aware Verification,” which only triggers multi-factor authentication (MFA) when a situation seems unusual.

This ensures that low-risk, frequent buyers enjoy a seamless experience while high-risk attempts are stopped or challenged instantly.

- Lesson for Enterprises: Personalization reduces friction. Use AI to create a “sliding scale” of security that rewards trusted users with faster checkouts.

3. Adyen payment optimization tools

Adyen uses an “AI-first” suite to connect the full payment funnel, from risk management to cost optimization. Their pilot programs have shown up to a 6% uplift in payment conversion rates by automating complex routing and retry logic.

By removing the need for manual rules, some of their enterprise customers have reduced their operational workload by 86%.

- Lesson for Enterprises: Automation drives efficiency. Moving away from manual rules allows your human teams to focus on high-value strategy rather than routine maintenance.

4. Mastercard AI fraud prevention

Mastercard’s Decision Intelligence system scores billions of transactions per month with sub-120 millisecond response times. Their use of “Smart Agents” provides 360-degree insights into merchant and customer behavior across multiple channels.

This allows banks and acquirers to save millions of dollars annually by identifying emerging threats before they result in a loss.

- Lesson for Enterprises: Speed is a security feature. Your AI layer must be fast enough to make decisions in the cloud without adding noticeable latency to the user journey.

5. Razorpay AI-led payment innovation

As a leader in the Indian fintech market, Razorpay is moving toward “Agentic Commerce.” Their AI agents monitor account health, automate invoice follow-ups, and resolve disputes autonomously. This shift transforms the payment gateway from a simple utility into an intelligent operational system that runs the business banking functions.

- Lesson for Enterprises: Think beyond the transaction. Look for ways to integrate AI into your wider financial operations, including receivables, payouts, and customer support.

The common thread among these leaders is the move toward a decoupled, intelligent architecture. They treat every transaction as an opportunity to collect data and refine their models. Furthermore, they prioritize the customer experience by using AI to remove unnecessary hurdles rather than adding them.

Conclusion

Upgrading your payment infrastructure with AI is a fundamental requirement for maintaining security, efficiency, and revenue growth in a digital-first economy.

Transitioning toward an intelligent, data-driven gateway ensures your business remains resilient against emerging threats while providing a seamless experience for customers. This strategic shift transforms your financial core into a powerful engine for long-term scalability and success.

Build AI Payment Gateway Systems With Intellivon

Building AI into an existing payment gateway is not about adding a standalone model beside your checkout flow. It requires designing a secure payment intelligence layer where transaction data, fraud signals, issuer responses, routing logic, failed payment patterns, and compliance controls work together in real time.

At Intellivon, we build AI-powered payment gateway systems that fit around your existing infrastructure. This helps fintech platforms, PSPs, marketplaces, SaaS businesses, lenders, insurers, and enterprises reduce fraud, improve authorization rates, recover failed payments, and make smarter payment decisions without replacing their current gateway.

A. Designing AI Decision Layers For Live Payments

Payment AI works best when it becomes part of the live transaction flow. We design AI decision layers that score, route, retry, and escalate payments before revenue is lost or risk increases.

- Real-time scoring APIs for fraud, risk, and payment failure prediction

- Rules engines that combine AI outputs with business payment controls

- Gateway middleware that connects checkout, PSPs, and decision systems

- Decision logs that record every approval, block, retry, or review action

This ensures your AI system does not sit outside the payment flow. It actively supports better payment decisions while keeping the existing gateway in place.

B. Building AI Fraud And Risk Scoring Engines

Fraud detection needs speed, context, and accuracy. We build AI fraud engines that evaluate every transaction using payment behavior, device signals, customer history, merchant patterns, location data, and past dispute outcomes.

- Transaction risk scoring before authorization

- Behavioral anomaly detection for suspicious payment activity

- False positive reduction logic to protect legitimate customers

- Human review queues for high-risk or unclear transactions

This helps your payment team reduce fraud exposure without blocking good customers unnecessarily.

C. Adding Smart Routing Across PSPs And Rails

High-volume payment systems need more than one default processor. We build smart routing systems that choose the best payment path based on approval rates, issuer behavior, cost, latency, risk level, region, currency, and provider performance.

- AI-assisted routing across gateways, PSPs, acquirers, and rails

- Failover logic when a provider slows down or fails

- Authorization optimization by issuer, market, and payment method

- Routing dashboards to track performance and revenue impact

This helps your payment stack improve success rates while reducing dependency on a single provider.

D. Securing AI Payment Gateway Architecture

AI payment systems must be secure from the first design decision. We build PCI-aware architectures that protect sensitive payment data while still giving AI models the signals they need to make accurate decisions.

- Tokenized data flows for sensitive payment information

- Secure API authentication between the gateway and AI services

- Role-based access controls for payment and risk teams

- Audit trails for compliance, fraud reviews, and dispute handling

This gives your business the intelligence layer it needs without increasing unnecessary payment data exposure.

If your payment gateway is already handling volume but lacks intelligence, Intellivon can help you build the AI layer around it. Contact our team to discuss your gateway setup, AI use cases, and integration roadmap.

FAQs

Q1. Can AI be added without replacing our payment gateway?

A1. Yes. AI can be added as a decision layer around your existing gateway using APIs, middleware, webhooks, and event streams. It helps score fraud risk, route payments, trigger retries, and monitor outcomes without forcing a full gateway replacement.

Q2. Is AI smart routing worth it for payment gateways?

A2. Yes, if you process high payment volume, use multiple PSPs, or face frequent declines. AI smart routing can improve authorization rates, reduce processor dependency, lower payment costs, and recover revenue by choosing the best route for each transaction.

Q3. Will AI slow down payment processing?

A3. Not if it is built correctly. AI payment systems need low-latency scoring APIs, timeout rules, fallback logic, and real-time monitoring. The goal is to make fraud, routing, or retry decisions within the payment flow without adding checkout friction.

Q4. How do we make AI payment decisions compliant?

A4. Use PCI-aware data flows, tokenization, access controls, audit logs, and human review paths. Every AI decision should be explainable, secured, and traceable so risk, compliance, and payment teams can review why a transaction was approved, blocked, routed, or retried.