Key Takeaways:

-

Agentic AML is a multi-agent compliance architecture built around unified customer, transaction, entity, and case data.

-

Deterministic AML rules must remain separate from probabilistic AI outputs throughout the platform architecture.

-

Behavioral ML and graph analytics power detection, while RAG-grounded LLM agents support investigation and SAR drafting.

-

Custom builds cost $70,000 to $300,000 with realistic timelines of four to nine months for deployment.

-

How Intellivon builds agentic AML platforms where analysts retain full control of escalation, case closure, and SAR submission.

AML compliance teams manage transaction monitoring queues that grow with every increase in transaction volume. In response, agentic banking compliance AI development starts with a graph-based entity resolution layer. That layer maps relationships between accounts, entities, and counterparties across the full transaction network. From there, AI agents monitor transactions, triage alerts, generate SAR narratives, and escalate cases for human review.

The graph layer, moreover, determines whether the AI detects real money laundering or simply mirrors legacy alert volumes. Without it, agents apply ML thresholds to individual transactions rather than network-level patterns. Research shows that 90% of AML alerts in traditional systems are false positives. Graph-based entity resolution is therefore the layer that changes that ratio fundamentally.

Intellivon builds banking compliance AI platforms where BSA, FATF, and SR 11-7 compliance are production requirements. The approach always starts with the graph entity resolution layer before any monitoring agent is designed. Accordingly, this blog covers multi-agent AML architecture, graph detection design, and SAR narrative generation.

What Agentic AML Means for Banking Compliance Teams

Agentic AML uses specialized software agents to execute bounded, multi-step compliance tasks across customer due diligence, transaction monitoring, screening, and regulatory reporting.

Unlike a conventional AML model, an autonomous agent can retrieve evidence, call approved tools, apply internal procedures, create case documentation, and route an outcome for final human review.

Consequently, banking compliance AI changes the compliance function from manual data gathering to managing automated, end-to-end exception workflows.

1. AML Rules vs Machine Learning vs Copilots vs Agents

Financial institutions deploy different compliance layers, but autonomous agents represent a fundamental shift in technical capabilities.

Meanwhile, copilots help analysts perform individual tasks by generating text or summarizing documents. In contrast, autonomous agents plan and complete entire multi-step workflows independently.

| Capability | Rule-Based Systems | Machine Learning | GenAI Copilots | Agentic AML |

| Autonomy Level | Zero autonomy | Predictive scoring | Interactive assistance | Bounded execution |

| Data Access | Static databases | Structured tables | Vector databases | Dynamic APIs |

| Action Capacity | Basic alerts | Risk classification | Text generation | Cross-system execution |

| Explainability | Fully deterministic | Black-box scoring | Probabilistic text | Deterministic audit trail |

| Human Review | 100% review required | 100% review required | Inline validation | Exception-based review |

2. An AML Agent Should Have One Bounded Compliance Role

Building a production-ready agentic AI compliance platform for banks requires deploying specialized agents rather than a single general-purpose system. Each digital worker operates within strict guardrails to perform one exact function perfectly.

According to research by McKinsey & Company, specialized agent squads working with dedicated lead, specialist, and QA roles deliver the highest operational reliability.

- Data Retrieval Agent: Logs into core systems to pull transaction history and customer profiles.

- Entity Resolution Agent: Connects disparate customer records and eliminates duplicate entries across business units.

- Transaction Analysis Agent: Tracks funds movement to spot layering patterns and structuring attempts.

- Sanctions Screening Agent: Scans global watchlists and OFAC SDN databases to catch restricted entities.

- Adverse Media Agent: Monitors global news sources for negative press concerning high-risk customers.

- SAR Narrative Agent: Drafts compliant Suspicious Activity Reports using structured investigation notes.

Agentic AML transforms banking compliance by shifting human investigators from manual data gatherers to strategic system overseers. At the same time, specialized digital agents execute complex compliance workflows while preserving complete deterministic auditability.

Why Banks Are Building Agentic AML Infrastructure Now

Banks are investing in agentic AML because their compliance problem is no longer limited to detecting individual suspicious transactions. They must connect customer behavior, counterparties, ownership networks, screening events, case histories, and changing typologies while preserving a defensible record of every decision.

Consequently, traditional infrastructure struggles to keep pace with modern financial crime patterns.

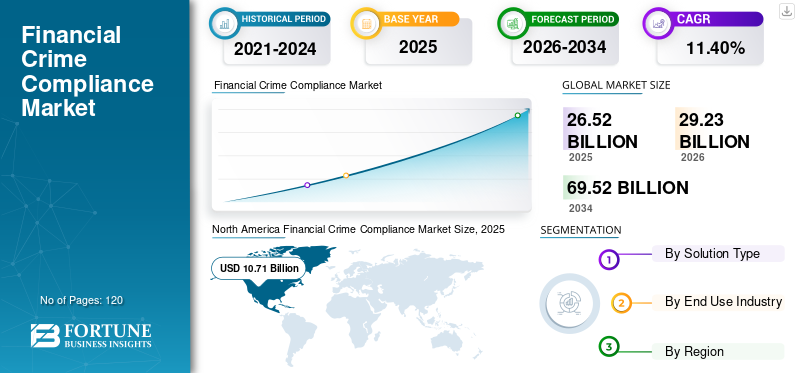

The global financial crime compliance market size is projected to grow from $29.23 billion in 2026 to $69.52 billion by 2034, expanding at a compound annual growth rate (CAGR) of 11.40%, according to Fortune Business Insights. This sustained multi-year investment cycle reflects the broader industry transition from labor-heavy operations to software-driven automation.

1. AML Investment Is Shifting Toward Measurable Effectiveness

Regulators are explicitly shifting their focus away from static, box-ticking processes toward demonstrable operational outcomes.

- FinCEN’s April 2026 Notice of Proposed Rulemaking (NPRM) fundamentally refocused AML/CFT program expectations on effectiveness rather than technical conformity.

- This regulatory push allows banks to deprioritize low-risk tracking and allocate technical capital toward complex risk isolation.

2. The Financial Crime Compliance Market Is Expanding

The economic pressure to modernize compliance architecture is accelerating globally as operational overhead balloons.

- The global financial crime compliance market size is projected to grow from $29.23 billion in 2026 to $69.52 billion by 2034, expanding at a CAGR of 11.40%, according to Fortune Business Insights.

- This massive deployment of capital reflects the industry-wide transition from labor-heavy operations to software-driven compliance automation.

3. Rule-Only Monitoring Cannot Connect Relationship-Level Risk

Legacy transaction monitoring systems rely on rigid thresholds that fail to detect coordinated, multi-entity financial crime.

- Mule-account networks that use multiple clean identities to distribute illicit funds.

- Circular fund flows designed to disguise the ultimate source or destination of capital.

- Rapid pass-through behavior where accounts are emptied within minutes of receiving transfers.

- Layering across products to break the continuous audit trail across cash, wires, and trade finance.

4. Analyst Capacity Does Not Scale Linearly With Alert Volume

Operations teams face extreme cognitive load due to fragmented systems, creating severe investigation bottlenecks.

- Investigators lose hours performing repeated data gathering and logging into up to five separate applications.

- Teams struggle with inconsistent narrative drafting and aging alert backlogs that introduce regulatory vulnerability.

- Manual collection of screenshots and notes forces compliance divisions to constantly choose between noise and missed risk.

5. Agentic AML Changes the Unit of Automation

Traditional automation improves isolated tasks, but agentic architecture orchestrates whole operational flows natively.

- Agents ingest alerts, gather multi-system evidence, compile case files, and deliver fully packaged investigations to human reviewers.

The transition to agentic AML is driven by a regulatory pivot toward program effectiveness and the collapse of rule-based systems under relationship-level risk. By automating entire investigative workflows rather than isolated tasks, banks can scale their compliance capacity without a linear increase in headcount.

Choose the First Loan Agent by Risk, Volume, and Data Readiness

The first automation setup should focus on a busy, everyday workflow that requires gathering simple proof but has no power to approve or deny loans on its own. Lenders find success by starting with basic data gathering, checking simple policy rules, or drafting denial letters rather than full auto-approvals.

Consequently, teams can test the new technology safely before giving AI systems the power to handle high-risk lending decisions.

1. Score Each Candidate Workflow Across Five Dimensions

Lenders sort out the best starting tasks by grading potential projects across five simple operational areas.

| Measurement | Importance (Weight) | What It Means |

| Mistake Risk | 25% | Focuses on areas where a human makes the final call. |

| Monthly App Volume | 20% | High-volume tasks save the most staff time. |

| Repeated Work Steps | 20% | Tasks that follow the exact same steps every time. |

| Data Accessibility | 20% | Requires clean digital access to credit systems. |

| Easy Success Tracking | 15% | Easy to measure how much faster the task gets done. |

Using this simple scorecard keeps risk managers from getting stuck on rare edge cases that slow down early projects. Therefore, companies build a safe operational foundation before trying to automate their entire loan lifecycle.

2. Start With Basic Data Gathering When Review Steps Repeat

Entry-level document queues are the best starting place because they follow the same matching rules every day.

- Stable Rules: Systems run smoothly when checking standard paperwork against a fixed list of company rules.

- Digital Inputs: The software reads standard customer files alongside past credit analyst decisions to compare its work.

- Fast Hand-offs: The system approves clear files and immediately hands complex files over to senior loan officers.

3. Start With Application Triage When Document Noise Dominates

Lending systems use smart tools to sort through large amounts of mixed paperwork and clean up messy applications.

- Name Analysis: The software checks variations in names, spelling mistakes, and alternative birthdays across credit databases.

- Proof Gathering: The agent automatically pulls local property data and business filings to verify user details.

- Safer Advice: The tool highlights mismatched data for human review but never modifies core credit criteria.

4. Start With Portfolio Tracking When Reviews Are Event-Driven

Moving from once-a-year portfolio checks to automatic alerts keeps lenders from missing sudden financial drops.

- Business Changes: The system watches for sudden shifts in company ownership, new management, or changing business addresses.

- Risk Warnings: Agents monitor sudden drops in bank statement cash flows or late payments on other credit lines.

- Document Tracking: The platform tracks expiring licenses and automatically asks the client for updated paperwork.

5. Start With Denial Drafts Only After Evidence Is Structured

Writing formal adverse action notices is a downstream step that requires fully verified facts before the software can type a word.

- Fact Ingesting: The writing tool needs access to verified credit scores, official dates, and exact missing document lists.

- Reason Matching: The software structures the text around exact regulatory rules and clear underwriter notes.

- Linked Proof: Every sentence in the draft letter links back to the original database record, so a human can verify it quickly.

Selecting a well-defined initial task provides the clean data structure and step-by-step proof needed to support larger AI networks later.

This initial setup creates the basic digital pipes needed to run stable AI operations across the company. Once these individual tasks run smoothly, the underlying architecture can safely scale to handle the entire end-to-end loan decisioning pipeline.

Where AI Agents Operate Across the AML Lifecycle

AI agents support the entire anti-money laundering pipeline, but each stage requires unique data, specialized tools, and clear human approval boundaries. A document-checking agent handles public records and identification files, while an alert-sorting agent evaluates transaction behavior.

Consequently, compliance teams deploy different specialized tools to tackle specific operational bottlenecks rather than relying on one general model.

1. Customer Onboarding, CDD, and Beneficial Ownership

New account opening requires agents to verify customer identities and map complex corporate structures rapidly.

- Data Extraction: The system automatically reads corporate registry filings, passports, and utility bills to confirm baseline information.

- Ownership Mapping: The tool traces ultimate beneficial owners across multi-tiered corporate structures to identify hidden risk.

- Risk Scoring: The platform assigns an initial customer risk rating by checking background data against policy rules.

2. KYC Perpetual Refresh and Enhanced Due Diligence

Moving past once-a-year calendar reviews allows agents to monitor active customer accounts for sudden profile changes continuously.

- Trigger Events: The system starts a review if a company changes its business address or adds new board directors.

- Background Monitoring: Agents check public news and court filings daily to flag negative media coverage involving current clients.

- Automated Outreach: The software drafts email requests to clients automatically when required licenses or identification files are about to expire.

3. Real-Time Transaction Monitoring and Alert Triage

Sorting through thousands of daily payment alerts requires agents to separate true risks from harmless customer behavior.

- Activity Baselines: The tool compares current wire, ACH, and card transactions against the client’s historical payment patterns.

- Peer Comparison: The system analyzes whether a customer’s spending looks normal compared to similar business accounts.

- Alert Enrichment: The agent pulls context from past bank files to explain why a transaction triggered a warning flag.

4. Sanctions, PEP, and Adverse-Media Screening

Screening workflows must handle different data formats across instant wire payments and static customer databases.

- Payment Screening: The system checks live international wire data within milliseconds to block banned entities.

- Political Risk: Agents screen names against global lists to identify politically exposed persons and their close associates.

- Data Cleansing: The software fixes name spelling variations and birthdate formats to lower the number of false alarms.

5. Case Investigation, SAR Drafting, and Regulatory Reporting

When a case requires deep analysis, agents assemble evidence timelines and draft regulatory filings for human approval.

- Timeline Creation: The software builds a clear visual map of all suspicious transactions, dates, and connected accounts.

- Narrative Generation: The agent writes a complete suspicious activity report narrative based on the verified investigation facts.

- Filing Handoff: The tool packages the approved report into the exact digital format required by federal financial regulators.

Section Takeaway: Deploying targeted agents across the compliance lifecycle reduces manual review times while building a completely auditable paper trail.

These distinct compliance jobs require specialized agents to pass evidence to one another without sharing unrestricted system authority. This strict operational division leads directly to the core design of a secure multi-agent platform architecture.

Designing Multi-Agent AML Architecture With Bounded Authority

A production agentic compliance platform requires an orchestration plane that manages specialist agents, restrains tool access, and routes key choices to human teams. Instead of using one massive AI model for every task, this architecture splits up work among focused, separate digital workers.

Consequently, lenders enforce strict operational boundaries and prevent a single model from independently approving risky transactions.

1. AML Orchestration and Workflow Control Plane

The control plane acts as the central manager, running task queues and routing work across the system without inventing its own legal authority.

- System Safeguards: The engine uses clear timeout limits, automatic retry configurations, and error recovery plans to handle database drops safely.

- Confidence Checks: The software scores its own work quality, routing files to senior teams automatically if confidence levels drop below set metrics.

- Idempotent Tasks: The platform ensures that repeating a process by accident results in identical outputs, preventing duplicate wire flags or data rewrites.

For a deeper breakdown of orchestration controls, see our guide on custom AI agent orchestration platform development. Intellivon designs these central control planes using deterministic rules to keep AI agents completely aligned with institutional compliance boundaries. Therefore, the core system never assumes its own regulatory powers.

2. Detection and Transaction Analysis Agents

Analysis agents review sudden risk signals coming from graph databases, machine learning systems, and transaction screening engines.

- Data Synthesis: The tool reads raw background signals and combines them with active device fraud warnings.

- Structured Output: The software formats its findings into an organized data file rather than creating a random text summary.

- Context Preservation: The agent passes this complete risk package to downstream workers without deleting the original transaction flags.

3. Entity, Ownership, and Network Investigation Agents

Investigation agents trace customer relationships and corporate ownership networks to find hidden links between bad actors.

- Relationship Discovery: The system reviews director lists, shareholder records, and shared physical addresses across different accounts.

- Flow Analysis: The software monitors circular payments, fan-in transaction spikes, and high pass-through ratios between suspect wallets.

- UBO Mapping: The agent builds complete corporate trees to reveal ultimate beneficial owners hidden behind multiple shell companies.

4. Research, Screening, and Evidence Agents

Evidence agents gather outside proof from approved channels while remaining blocked from accessing the open internet.

- Database Access: The system connects directly to formal business registries, global watchlists, and political exposure lists.

- Historical Review: The software checks past internal case notes and previous adverse media records to verify client histories.

- Source Validation: The tool links every pulled fact to an official record, ensuring human investigators can check the source text quickly.

5. SAR, Policy, and Quality Assurance Agents

Three independent agents handle report writing, procedure checks, and quality control to ensure strict filing compliance.

- The Writer: The SAR agent converts verified case facts into a clean, structured text draft matching regulatory standards.

- The Checker: The policy agent matches the draft report against local compliance rules and internal bank guidelines.

- The Auditor: The QA agent looks for missing evidence, math errors, and contradictory statements before a human signs off.

Splitting compliance duties among specialized agents protects the lending system from unmapped errors and hidden operational biases.

However, complex orchestration cannot fix broken or messy customer records. Consequently, engineers must design the underlying data and evidence layer completely before writing agent prompts or building automated workflows.

Build the AML Data and Evidence Layer Before the Agents

Agentic compliance systems require a unified data layer that connects customers, accounts, transaction events, and past choices. Without clear identity mapping, normalized time logs, and strict data tracking, agents will simply write highly polished summaries of broken or contradictory facts.

Consequently, institutions must build a single source of true data before deploying autonomous software tools.

1. Create a Canonical AML Data Model

A standardized data setup organizes all core banking records into clear, connected categories that agents can easily search.

- Core Entities: The platform structures entries for individual customers, corporate legal entities, distinct accounts, and active device footprints.

- Event Records: The architecture groups transaction flows, risk alerts, historical cases, and official regulatory filings into unified data blocks.

- Document Tracking: The system links specific identity files and background screening logs directly to the primary customer profile.

2. Resolve Customer and Counterparty Identities

Clean identity resolution ensures the platform accurately groups matching records across separate banking applications.

- Name Normalization: The software standardizes varying business names, resolves spelling variations, and handles complex foreign name translations.

- Relationship Discovery: The system links joint accounts, traces parent-subsidiary corporate ties, and groups profiles sharing identical contact details.

- Cross-System Tracking: The infrastructure maps scattered legacy customer identifiers into a single, permanent digital profile.

3. Build an Event-Driven Transaction Data Pipeline

Lenders require dynamic data pipelines to process real-time payments alongside delayed batch updates without losing track of details.

- Time Alignment: The pipeline normalizes payment timestamps across different time zones while managing late-arriving ledger entries cleanly.

- Correction Handling: The software accounts for sudden payment reversals, delayed settlement finalizations, and declined transactions automatically.

- Duplicate Control: The framework filters out duplicate event notifications to prevent agents from analyzing identical payments twice.

4. Use a Financial Crime Knowledge Graph

A graph database stores clear structural links between different customers, accounts, and payment paths across the entire bank.

- Link Visualization: The software maps out shared hardware devices, common physical addresses, and rapid money flows between accounts.

- Historical Memory: The system highlights whenever a new applicant shows direct connections to a previously flagged fraud case.

- Structural Safety: The graph database stores physical relationships clearly, allowing teams to run optional detection neural networks later.

5. Preserve Evidence Provenance and Data Lineage

Every document or summary generated by an AI agent must track its original data sources precisely for regulatory auditing.

- Source Tracking: The system attaches the original database name, exact record numbers, and data collection times to every document.

- Version Control: The tool saves the exact prompt, model version, and bank policy text utilized during the automated analysis.

- Audit Readiness: This tracking satisfies Federal Financial Institutions Examination Council (FFIEC) audit standards by proving that the bank can verify its automated surveillance systems.

A reliable evidence pipeline prevents software agents from hallucinating conclusions or acting on incomplete borrower profiles. Once this data foundation is completely trustworthy, risk teams can match each specific task to the exact type of AI model designed to run it.

Select AI Models by AML Task Type

Production systems combine deterministic rules, supervised classifiers, anomaly detection, and graph analytics because no single AI model can handle the entire compliance workflow alone. Consequently, effective setups function as hybrid networks where each technology solves a specific operational problem.

Lenders reduce error rates by matching every separate task to the exact type of software logic designed to run it.

1. Keep Deterministic Rules for Known Typologies and Obligations

Fixed logic remains the best tool for enforcing legal minimums, managing clear thresholds, and tracking strict regulatory filing deadlines.

- Hard Cutoffs: Rules handle exact currency amount limits, velocity triggers, and banned geographical regions automatically.

- Portfolio Control: The system blocks prohibited counterparties and enforces product restrictions without needing an AI estimate.

- Controlled Modifying: Software agents can recommend updates to these rule structures but cannot publish changes without human sign-off.

2. Use Supervised Models for Prioritization and Classification

Supervised machine learning algorithms evaluate known risks by analyzing new applications against historical analyst decisions.

- Queue Filtering: The software calculates false-positive likelihoods and assigns priority scores to new application alerts.

- Risk Grouping: The tool places customers into clear risk categories based on past defaults and verified profile histories.

- Predictive Routing: The system uses gradient-boosted trees and random forests to forecast which files require specialized executive review.

For a deeper look at transaction-scoring setups, see our guide on AI-powered transaction monitoring system development. Therefore, the system scores risks consistently before agents trigger downstream workflows.

3. Use Behavioral and Anomaly Models for Unknown Patterns

Anomaly detection tools watch for subtle deviations from normal activity to catch new fraud techniques that lack fixed rules.

- Baseline Tracking: The platform flags sudden shifts in transaction frequency, unexpected value spikes, or dormant account activations.

- Peer Analysis: The software raises an alert if an account’s spending habits deviate from those of similar business profiles.

- Location Monitoring: The system tracks sudden geographic changes and unusual counterparty payment routes in real time.

4. Use Graph Models for Network-Level Financial Crime

Graph databases map physical connections to expose coordinated networks, shell companies, and layered transaction flows.

- Link Discovery: The framework uncovers hidden money networks by highlighting multiple accounts sharing identical hardware addresses.

- Flow Detection: The software traces rapid pass-through actions, circular fund movements, and dense suspicious community groups.

- Mule Tracking: The tool flags sudden corporate connections that match known money-laundering layering patterns.

5. Use LLMs for Evidence Interpretation

Language models should only interpret documents and draft summaries, rather than act as primary transaction risk scorers.

- Text Processing: The software handles complex text tasks like adverse-media grouping, case summarization, and document data extraction.

- Drafting Support: The tool references internal credit policies to construct structured investigation outlines and SAR drafts.

- Constrained Design: Emerging compliance research shows that source-linked retrieval and counterfactual checks reduce text errors in automated triage systems.

Deploying a hybrid model framework ensures that language models focus on text interpretation while mathematical models handle risk scoring.

However, model accuracy alone does not determine whether an automated compliance system can execute a task. The platform architecture must define human authority boundaries and agent autonomy limits as distinct operational layers.

Human Review Boundaries and Progressive Agent Autonomy

Human review boundaries must be set based on the real-world consequences of an action, rather than on how impressive an agent appears in a software demo. Data retrieval and narrative drafting can run with high autonomy, whereas freezing accounts, closing high-risk alerts, and submitting regulatory filings require explicit human approval.

Consequently, lenders protect their institutional risk profiles by keeping final authority in human hands.

Level 0 — Observation and Shadow Mode

Lenders use shadow mode to safely test software agents against historical files before giving the platform any operational control.

- Passive Processing: The agent analyzes live or historical cases in the background without affecting active banking operations.

- Side-by-Side Validation: The system compares the agent’s recommended choices directly against the final decisions made by human analysts.

- Performance Baseline: This stage tracks model drift and scoring accuracy metrics to establish a clear operational baseline.

Level 1 — Analyst Assistance

At this level, the platform operates as a digital assistant to speed up manual research workflows for human underwriters.

- Evidence Gathering: The tool automatically pulls credit bureau histories, corporate registry data, and bank statement cash flows.

- Draft Generation: The agent creates concise file summaries and drafts formal adverse action notices for review.

- Full Oversight: A human credit officer reviews every piece of generated text and signs off on every recommendation.

Level 2 — Controlled Low-Risk Execution

Lenders grant limited execution authority to mature agents only within narrowly defined, low-risk operational categories.

- Automated Outreach: The software automatically emails borrowers to request missing tax returns or updated business licenses.

- Routine Processing: The agent closes specific, low-risk false-positive alerts that match pre-approved clearing rules.

- Override Safeguards: The platform uses strict confidence thresholds and immediately flags any data deviations for manual human review.

Level 3 — Conditional Workflow Autonomy

Conditional autonomy allows validated agent networks to manage standard underwriting pipelines within strict credit portfolio limits.

- Routine Management: The system handles clear-cut approvals for prime borrowers who perfectly match institutional lending criteria.

- Bounded Escalation: The platform automatically routes non-standard applications or minor policy exceptions to senior risk committees.

- Continuous Sampling: Compliance teams run daily random audits on auto-approved files to ensure absolute policy alignment.

Decisions That Should Remain Human-Controlled

Final credit authority, risk policy adjustments, and material adverse actions must remain entirely under human control.

- High-Risk Actions: Humans must handle final suspicious activity report submissions, account freezing, and law-enforcement referrals.

- Lending Governance: Only authorized risk leaders can modify core credit rules, approve new models, or alter the bank’s risk appetite.

- Compliance Reality: Industry practitioners highlight that fully automated alert closure exposes institutions to severe regulatory penalties.

Progressive autonomy allows institutions to scale up automated operations safely as the underlying AI models prove their accuracy over time.

Human control must remain fully visible to bank examiners through clear system documentation, model validation reports, and detailed override logs. This complete operational transparency leads directly to the core compliance requirements demanded by financial regulators.

Make Agentic AML Explainable

Examiner-ready compliance requires separate governance for rules, risk models, and language layers. Every technical piece needs an owner, an approved purpose, and a validation history to prove it operates safely.

Consequently, lenders establish deep regulatory transparency by proving their automated tools remain entirely inside human-authorized limits.

1. Apply Current Frameworks and Inventories

In April 2026, the Federal Reserve, FDIC, and OCC issued SR 26-2 (Revised Guidance on Model Risk Management), officially superseding the legacy SR 11-7 framework.

While generative AI sits outside its formal quantitative scope, banks must still manage agent platforms under broader safety, privacy, and third-party risk rules.

Therefore, compliance teams must maintain a centralized inventory documenting each agent’s purpose, inputs, permitted tool actions, and deployment versions.

2. Validate and Explain Workflows Safely

Risk teams must validate mathematical detection models and conversational agent workflows using entirely different testing criteria.

- Model Validation: Measures data precision, historical stability, and scenario backtesting.

- Agent Validation: Checks tool-selection logic, policy citation accuracy, and escalation rates.

- Evidence Explanations: Platforms must produce clean audit files showing triggered rules and source citations rather than raw text reasoning.

Component-level governance ensures that automated underwriting systems produce examiner-ready audit trails for every decision.

Safe Workflows

| Regulation | Requirement | System Impact |

| BSA / FinCEN | Risk-based reporting | Drives automated SAR drafts |

| EU AI Act / GDPR | Transparent logic | Blocks unmapped data processing |

This governance framework establishes why a platform is permitted to operate. Next, robust technical security architectures ensure that software workers cannot break out of these authorized boundaries.

Secure Every Agent and Compliance Data Path

Every AML agent must operate as a separately governed identity with limited data access, short-lived tokens, and complete activity logs. Giving a software tool broad access to core networks creates severe security vulnerabilities if a mistaken prompt triggers unauthorized actions.

Consequently, lenders prevent system-wide breaches by wrapping every autonomous component in a strict, zero-trust infrastructure layer.

Protect Identities and Tool Gateways

Lenders enforce the principle of least privilege by assigning dedicated service identities to individual software agents.

- Bounded Access: Software workers use short-lived credentials and attribute-based permissions to read only the specific records needed for their active tasks.

- Controlled Gateways: Agents are blocked from calling core banking APIs directly, routeing all requests through an isolated security gateway instead.

- Strict Enforcement: The gateway checks parameter shapes, enforces hard request rate limits, and demands manual human approval for any write permissions.

Defend Data Paths and Memory Stores

Active systems must actively screen out malicious inputs buried within untrusted customer documents or compromised public websites.

- Injection Defense: The platform isolates incoming data, uses schema validation, and cleans text to block prompt injection attacks.

- Memory Control: The database limits agent memory to the scope of a single case file, wiping temporary data records upon workflow completion.

- Data Privacy: The architecture separates tenant environments, encrypts sensitive records, and excludes all personally identifiable information from future model training.

Add System Kill Switches and Safe Failsafes

Lenders protect operational continuity by building mechanical circuit breakers that trigger when vendor APIs drop or performance metrics decline.

| Failure Event | System Action | Compliance Result |

| Watchlist Provider Outage | Pauses automated triage | Prevents un-screened processing |

| Unauthorized Agent Action | Revokes service token | Halts unexpected pipeline shifts |

| Latency Limit Crossed | Routes the file to the human queue | Maintains required banking speed |

Isolating software agents within a secure tool gateway ensures that technical errors cannot compromise core banking databases.

This security infrastructure guarantees that automated workers stay within their assigned technical boundaries. Next, the engineering team must connect these secure agents to the primary platforms where loan and customer data actually reside.

Integrate Agents With Core Banking and Existing AML Systems

A production deployment requires deep connectivity into your existing software ecosystem to turn raw analysis into automated actions. Building these links incorrectly can cause system downtime, laggy approvals, and out-of-sync databases.

Consequently, financial institutions design decoupled integration layers to move data securely between new reasoning agents and legacy transactional platforms.

1. Connect to Leading Core Systems and LOS Platforms

Lenders connect automated platforms to their primary transaction records and application software using microservices.

- Modern Integration: Software agents read application details directly from systems like nCino or Encompass through secure application programming interfaces (APIs).

- Legacy Connectivity: The architecture utilizes custom adaptors to pass credit decisions back to older core providers like Fiserv or Jack Henry.

- Customer Syncing: The system automatically pushes case summaries and adverse action notes into platforms like Salesforce to keep business records identical.

2. Build Multi-Tenant Architecture and Role-Based Controls

Fintech firms use multi-tenant designs to scale their systems across multiple business units while keeping operations completely separate.

- Environment Separation: The database physically splits client data stores, ensuring no application information ever crosses into another group’s workspace.

- Access Mapping: Risk leaders define clear roles, granting read-only access to basic agents while locking data modifications behind senior analyst profiles.

- System Growth: The orchestration layer balances transaction loads dynamically, allowing the platform to manage sudden application spikes without slowing down.

Decoupled API layers allow modern AI agents to interact with legacy banking cores without causing system lag.

Role-Based Controls System Type

| System Type | Integration Focus | Operational Target |

| Loan Origination (LOS) | Real-time data sync | Faster borrower approvals |

| Core Banking Platform | Record reconciliation | Error-free ledger logging |

This integration layer ensures data moves quickly between old banking cores and new automation networks. Once these digital pipes are secure, lenders can accurately estimate the complete technical investment required to build the platform.

Build AI Agents for AML Compliance in Seven Phases

Lenders deploy agentic underwriting infrastructure by following a structured engineering lifecycle. Building these platforms requires separating planning, data integration, model tuning, and security testing into distinct phases.

Consequently, teams deploy low-risk automated features first, proving system reliability before giving software tools the power to handle core portfolio decisions.

Phase 1 — Map AML Workflows, Risk Appetite, and Authority

Phase one defines your existing underwriting steps, standard operating procedures, and specific employee decision boundaries. Engineers map where legacy application bottlenecks happen and establish clear speed metrics for the project.

Intellivon maps every single agent action to an accountable compliance manager before picking any software models. Next, this operational plan moves into the data connection phase.

Phase 2 — Build the Customer, Transaction, and Entity Layer

Phase two builds a unified database that connects borrower profiles, banking transactions, and historical case outcomes together. The pipeline cleans messy names and maps company ownership trees so agents read accurate facts.

Intellivon stabilizes this evidence pipeline entirely before developing any agent prompts or autonomous software paths. Once data flows cleanly, the system is ready for risk classification logic.

Phase 3 — Develop Rules, Behavioral Models, and Graph Detection

Phase three builds the hybrid mathematical core, combining fixed compliance rules with machine learning and graph networks. These models group credit applicants, calculate risk scores, and flag network anomalies like shell companies.

Intellivon separates deterministic legal cutoffs from probabilistic machine learning risk signals to ensure absolute system control. This math engine then feeds directly into the reasoning systems.

Phase 4 — Build the Agent Orchestration and RAG Layer

Phase four configures the central control plane, specialized agent roles, secure tool gateways, and localized policy databases. The system cuts complex credit manuals into searchable data blocks, forcing agents to output structured files.

Intellivon gives each separate software worker a narrow functional purpose, explicit tool permissions, and clear completion rules. Next, these backend agents connect to the human interface.

Phase 5 — Develop Case Workflows and System Integrations

Phase five links the automation engine to human workspaces and primary loan origination software like nCino. Engineers build clean timelines and relationship maps so human underwriters can review agent work quickly.

Intellivon preserves the financial institution’s existing system of record unless building a new interface offers a massive speed advantage. With integrations active, the testing process begins.

Phase 6 — Validate in Historical Replay and Shadow Mode

Phase six runs the complete automated network in shadow mode against past loan files to evaluate its real-world accuracy. Teams run prompt-injection attacks and simulate missing data scenarios to check if the system escalates files correctly.

Intellivon blocks agents from receiving any data write authority until they pass independent security, policy, and workflow validations. After passing these benchmarks, the platform goes live.

Phase 7 — Roll Out Progressive Autonomy and MLOps

Phase seven opens the platform to limited user groups, automating simple, low-risk loan files while monitoring for model drift. Compliance teams use random sampling loops to audit auto-approvals and update agent prompt versions safely.

Intellivon expands system autonomy by narrowing credit categories rather than flipping on full, platform-wide automation at once.

A phased engineering framework guarantees that financial platforms maintain total regulatory compliance while scaling up automated operations.

Following this step-by-step roadmap allows engineering teams to control project scopes and build highly reliable software infrastructure. With the build steps clearly defined, risk leaders can accurately map out the total financial investment required to launch the platform.

Agentic AML Platform Development Costs $70K to $300K

Agentic AML platform development usually costs $70,000 to $300,000, depending on agent scope, transaction volume, graph and ML requirements, core banking integrations, regulatory jurisdictions, security controls, deployment model, and validation depth.

At the same time, lenders reduce technical risk by matching their starting budget to their current operational scale.

Consequently, institutions avoid unexpected software expenses by choosing a clear development tier early in the planning process.

1. Focused AML Agent MVP — $70,000 to $110,000

A minimum viable product focus builds a basic automation pipeline that tackles one high-volume business bottleneck safely.

- System Boundaries: The setup uses two or three specialized agents to handle basic alert intake and read data files cleanly.

- Core Functions: The software connects to an internal policy knowledge base to build structured case summaries or suspicious activity report drafts.

- Target Processes: This budget tier works best for automating entry-level alert sorting, simple sanctions reviews, or basic customer research tasks.

2. Production Banking Compliance AI Platform — $120,000 to $210,000

A full production platform scales automation across five to eight distinct software agents to manage active, live customer accounts.

- Advanced Scoring: The system uses behavioral models and identity resolution tools to track incoming consumer application data points accurately.

- Enterprise Features: The architecture includes single sign-on access controls, live sanctions data feeds, and complete dashboard workspaces for human teams.

- Safe Validation: Engineers run the code in shadow mode first to verify real-world accuracy before pushing decisions into production pipelines.

3. Enterprise or Multi-Tenant Agentic AML Platform — $220,000 to $300,000

Top-tier enterprise software supports multi-tenant workspaces, graph analytics, and multi-country compliance rules for global institutions.

- Complex Data: The platform uses deep graph models to track complex corporate networks and find hidden money laundering chains.

- Infrastructure Depth: The build includes a private-cloud setup, fully automated model tracking pipelines, and isolated audit logging environments for different business units.

- Resilient Systems: The framework includes complete disaster recovery systems and handles massive transaction spikes across multiple core banking platforms seamlessly.

4. Development Phase Cost Breakdown

The complete technical build is split across seven key engineering phases. Because these stages naturally overlap during production, the maximum cost boundaries are not directly additive.

| Development Phase | Estimated Price Range |

| Workflow Discovery and Control Design | $8,000–$15,000 |

| AML Data, Entity, and Evidence Layer | $15,000–$40,000 |

| Rules, ML, and Graph Detection Models | $18,000–$50,000 |

| Agent Orchestration and RAG Infrastructure | $18,000–$45,000 |

| Case Workflows and Software Integrations | $15,000–$55,000 |

| Security, Model Validation, and MLOps | $12,000–$40,000 |

| System Deployment, Training, and Rollout | $5,000–$15,000 |

5. Annual Maintenance and Model Governance Costs

Lenders must budget 15% to 25% of the initial build cost annually to cover long-term system updates, security patches, and platform governance.

- Continuous Tuning: Ongoing fees cover cloud server upkeep, data feed maintenance, software prompt updates, and adjustments for changing banking laws.

- Licensing Realities: Ongoing commercial software costs for external credit bureaus, name screening registries, and identity verification APIs sit completely outside this build budget.

- Intellivon Estimates: Past custom deployment records place related transaction-monitoring projects broadly within the $60,000 to $250,000 space, confirming that a comprehensive multi-agent system falls reliably inside this $70,000 to $300,000 range.

Transparent tier-based budgeting ensures that financial teams align their software investments directly with their long-term compliance goals.

This clear cost breakdown provides risk leaders with the concrete data needed to evaluate project scopes. Understanding the required financial investment allows executives to accurately weigh the choice between building custom code and buying off-the-shelf software.

Build Agentic AML Infrastructure With Intellivon

Build agentic AML infrastructure with Intellivon when your bank or fintech needs more than a basic case-summary chatbot or another layer of static rules. Intellivon acts as a trusted development partner, delivering production-ready multi-agent orchestration, graph-based detection, compliance-grade RAG, and examiner-ready controls. Consequently, financial institutions deploy technically rigorous, production-grade security layers that withstand strict regulatory scrutiny.

- Architecture and Integration: We build your unified data layer, orchestration engines, and tool permissions first, connecting seamlessly with legacy systems like FIS, Fiserv, Jack Henry, and Temenos.

- Hybrid Intelligence and Governance: The platform combines typology rules, behavioral models, and graph analytics within a fully governed MLOps pipeline featuring immutable human override logs.

- Enterprise Delivery Depth: Work with ex-MAANG engineers backed by 500,000+ engineering hours to build custom systems within a clear $70,000 to $300,000 range.

Talk to Intellivon’s fintech AI team to map your AML workflows, define safe agent boundaries, and estimate your custom build.

Conclusion

Deploying agentic loan decisioning transforms underwriting by replacing rigid rules with flexible controls. Consequently, structural data integration must always precede model selection.

This hybrid approach securely balances machine learning, graph networks, and human check gates. Therefore, institutions scale safely using progressive autonomy rather than immediate automation. Your immediate next step is selecting the first workflow to pilot.

FAQs

Q1. Can an AI Agent Automatically Close AML Alerts?

Only tightly defined, low-risk alert categories should be considered for automated closure. Consequently, the platform requires historical validation, strict confidence thresholds, evidence-linked explanations, and approved closure policies.

High-risk alerts, sanctions matches, and material customer actions must remain human-controlled. Therefore, risk managers deploy progressive autonomy rather than full immediate automation.

Q2. Should Banks Replace Their Existing AML System With Agents?

Lenders should keep their current transaction platform if it generates reliable alerts, stores cases securely, and exposes usable APIs. Consequently, you can deploy agents around legacy engines to handle evidence collection, graph analysis, and narrative reporting.

Replace core software only when rigid workflows or extreme vendor costs block effective modernization.

Q3. Can Agentic AML Reduce False Positives Without Missing Risk?

Autonomous systems reduce unnecessary alerts when the platform enriches files with customer behavior data, peer groups, and historical risk context. However, false-positive reductions must be balanced against precise recall scores and clear typology coverage.

Therefore, compliance teams track complete data lineage to guarantee that a lower alert volume never masks hidden financial crimes.

Q4. Is Custom Agentic AML Cheaper Than NICE Actimize or Oracle AML?

Custom development becomes more economical when five-year enterprise licensing fees, transaction charges, configuration rates, and vendor lock-in exceed software ownership costs.

Alternatively, a custom build is less attractive if a bank needs instant, pre-maintained workflows. Consequently, teams choose custom builds to gain flexible control over proprietary credit code.

To Sum It Up:

- An AML chatbot can draft text, but agentic AML must retrieve evidence, call controlled tools, follow policy, and preserve every action for review.

- Banks should automate evidence gathering before automating regulatory decisions because workflow reliability develops faster than decision authority.

- Graph analytics identifies relationship-level laundering patterns that transaction-by-transaction rules cannot see.

- A lower false-positive rate has little value unless recall, typology coverage, evidence quality, and false negatives remain within approved limits.

- Existing AML platforms do not always need replacement; a governed agent layer can modernize investigations while preserving the current system of record.