Key Takeaways:

-

AI AML platform development requires transaction data, alert history, KYC records, and SAR evidence preparation.

-

Model-risk documentation, secure infrastructure, case workflows, vendor integrations, and human review controls are mandatory.

-

Real-time monitoring, graph analytics, sanctions integrations, model validation, and audit controls define enterprise readiness.

-

Enterprise AI AML platforms cost $60,000 to $250,000 with annual maintenance at 18 to 25%.

-

How Intellivon builds AI AML platforms around data lineage, explainability, MLOps, security, and examiner-ready evidence.

AI AML platform development for banks starts with the question about what the platform needs to do. The answer falls into five non-negotiable layers, which include data readiness, model governance, SAR reporting infrastructure, a human-in-the-loop review workflow, and an immutable audit trail. When the platform is built on these 5 layers, explainability is clear, and the pipelines are clear for the engineers.

The sequencing of that build determines whether it works. Without the right data mapping, the AI has no credible foundation. Your labeled SAR data, alert disposition history, and KYC records must map to your regulatory schema before any model trains. Banks that structure this data layer before development reduce false positive volumes by up to 60%. They also double compliance ROI within 18 months, thereby rebuilding examiner trust and erasing the investigation backlog that erodes institutional credibility.

Intellivon has built compliance-native AI for financial institutions for over ten years, always starting with requirements validation rather than model selection. That sequence is what this blog walks through, and by the end, you will have a framework to scope your AI AML build, secure board approval, and evaluate any partner.

What Is an AI AML Platform for Banks?

An AI AML platform for banks is a compliance technology system that uses machine learning, graph analytics, rules, entity resolution, case intelligence, and human-review workflows to detect, prioritize, investigate, and document suspicious financial activity. It connects transaction monitoring, KYC/CDD data, sanctions context, case management, SAR workflows, and model governance into one controlled AML operating layer.

Consequently, leadership teams must realize this platform is not a basic fraud dashboard. While fraud tools catch immediate losses, an enterprise AI AML platform development strategy focuses on long-term systemic risk.

Therefore, it systematically supports alert triage, dynamic risk scoring, deep investigation, automated SAR evidence gathering, and strict audit readiness.

For example, by using integrated graph analytics, investigators can instantly visualize complex shell company networks that manual reviews miss.

Core Architecture Components

- Data and Detection Layers: Combines a real-time transaction monitoring engine with an entity resolution layer. This connects KYC, CDD, EDD, and beneficial ownership data into a unified customer risk profile.

- Workflow and Governance Layers: Powers alert prioritization and case routing into a human-in-the-loop investigation workflow. This setup feeds SAR evidence support while maintaining an immutable logging layer for model risk validation.

| Platform Layer | What It Does | Why Banks Need It |

| Data Layer | Collects transaction, customer, KYC, and case data | Creates the foundation for reliable AML detection |

| Detection Layer | Uses rules, ML, anomaly models, and graph analytics | Identifies suspicious activity patterns |

| Investigation Layer | Routes alerts, evidence, and reviewer actions | Helps analysts make faster case decisions |

| Reporting Layer | Supports SAR evidence and regulatory documentation | Improves reporting quality and examiner readiness |

| Governance Layer | Tracks models, approvals, validation, and monitoring | Supports model risk management requirements |

Ultimately, banks must view this platform as highly regulated banking infrastructure. Your engineering and compliance teams are not just buying trendy software. On the contrary, you are building a tightly controlled decision system for financial crime compliance.

Once the platform architecture is clear, the next logical question is why banks are prioritizing this shift right now.

Why AI AML Platform Development Is Becoming a Priority

Modernization is being pulled by three inescapable forces: financial crime scale, digital transaction growth, and escalating regulatory pressure. Boards care deeply about controlling operational risk, avoiding severe regulatory findings, and managing structural compliance costs. Therefore, banks are not investing in AI simply to reduce operational headcount.

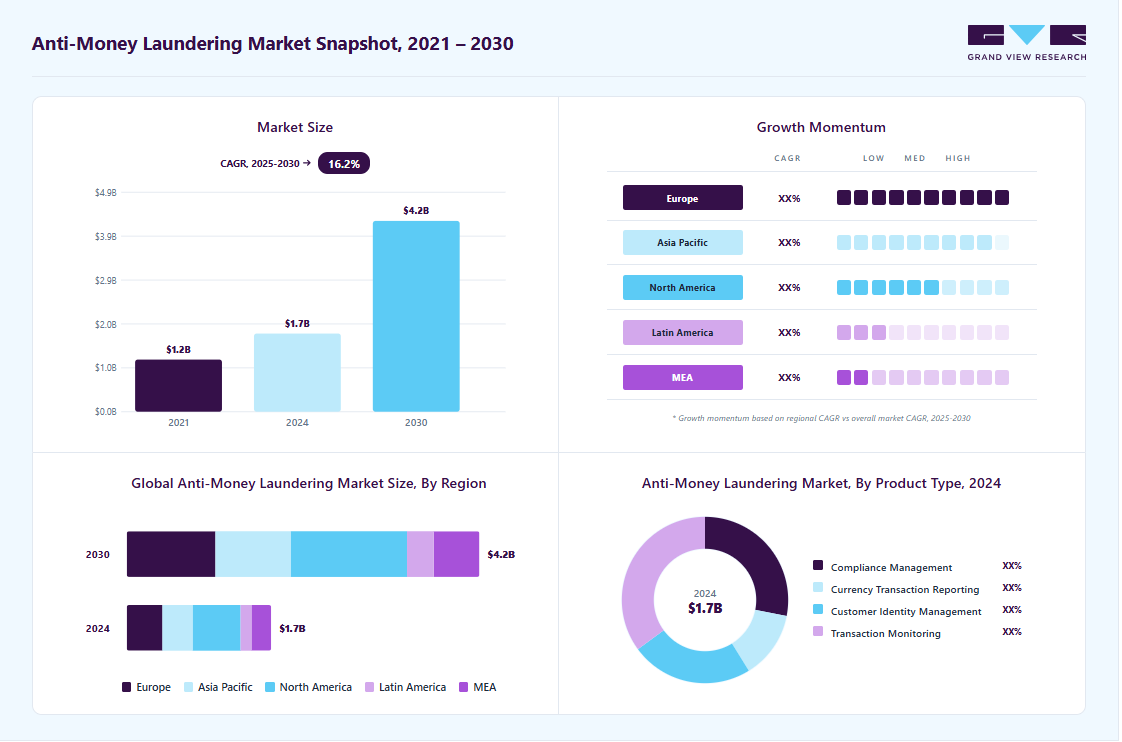

The global anti-money laundering market is projected to reach USD 4.24 billion by 2030, growing at a 16.2% CAGR according to Grand View Research. Similarly, MarketsandMarkets expects this sector to hit USD 9.38 billion by 2030 at a 17.8% CAGR.

Consequently, expanding transaction volumes and complex criminal networks make automated infrastructure investment an urgent priority for banking boards.

1. Financial Crime Is Outgrowing Manual Review Capacity

Financial crime volume is growing faster than traditional AML review teams can scale.

Banks need AI-assisted prioritization, entity resolution, typology detection, and case intelligence because more analysts alone cannot solve fragmented data, high false positives, and hidden network behavior.

- Transaction and Payment Speed: Explosive digital transaction growth and real-time, faster payment rails make manual intervention impossible.

- Complex Illicit Networks: Sophisticated cross-border flows, decentralized mule networks, and layered shell companies hide true ownership.

- Graph-Based Anomaly Patterns: Laundering patterns use distributed, multi-hop networks that require structural graph-based detection to uncover.

2. AML Budgets Are Moving Toward Infrastructure

AML budgets are shifting toward infrastructure because banks need systems that connect data, detection, review, reporting, and governance.

Standalone monitoring tools cannot support examiner-ready evidence if data lineage, model validation, reviewer actions, and SAR documentation remain disconnected.

- AML Platform Data Requirements: Centralizing historic transaction histories, customer profiles, and alert disposition histories into clean, standardized pipelines.

Globally, financial institutions now spend USD 206 billion annually on financial crime compliance to manage these disparate pipelines, as detailed by Flagright.

- Model Risk Management and MLOps: Deploying robust version control, automated retraining, and model validation software to satisfy regulatory frameworks.

This is critical given that total compliance costs across the US and Canada have spiked to USD 61 billion annually, according to studies by LexisNexis Risk Solutions.

- Governance and Board Oversight: Satisfying strict board oversight requirements for AML AI standards by tracking system performance through transparent reporting.

Within large financial institutions, the average individual bank now spends approximately USD 64.42 million annually just to sustain these basic processes, according to data from Tookitaki.

3. AI Adoption in Banking Is Raising Compliance Expectations

AI adoption in banking raises compliance expectations because regulators, risk teams, and boards need proof that models are explainable, validated, monitored, and controlled.

For AML, this means every AI score must connect to clear evidence, review accountability, and documented governance.

- Regulatory Explainability Standards: Transitioning away from opaque black-box models toward transparent systems that provide clear reasoning for every alert.

This change is urgent since 79% of organizations report that escalating software costs drive compliance increases, as documented by LexisNexis Risk Solutions.

- Human-in-the-Loop Design: Ensuring human reviewers validate, adjust, and log all machine learning decisions for comprehensive accountability.

This approach optimizes efficiency, especially in regions like EMEA where compliance operations require USD 85 billion in yearly funding, according to research by Lucinity.

- Third-Party Risk Management: Creating absolute traceability within the system to satisfy strict third-party risk and internal audit mandates.

This framework helps banks mitigate structural risks while handling millions of alerts before filing official documentation, as noted by Mayer Brown.

Ultimately, modern banks must recognize that building an AI AML system means establishing defensive infrastructure.

This structural development ensures your compliance architecture scales efficiently under intense regulatory pressure.

AI AML Platform Development Requirements for Banks

AI AML platform development requirements banks should define first include data readiness, transaction coverage, KYC/CDD completeness, beneficial ownership structure, model-risk governance, explainable scoring, SAR evidence capture, infrastructure security, core banking integrations, and human-in-the-loop review.

These requirements decide whether the build becomes a production compliance system or a fragile analytics layer.

1. Core Data Pipeline and Normalization Requirements

Establishing a clean data ecosystem is the initial engineering step. The engineering team must build a transaction monitoring data pipeline capable of structured parsing. This setup ingests and standardizes complex customer risk rating data, transaction histories, and historical alert disposition history data.

- KYC and Entity Completeness: Merging fragmented identity files, customer records, and CDD/EDD data into structured data formats.

- Beneficial Ownership Data Structure: Mapping layered corporate relationships and ultimate beneficial ownership records to resolve entity context.

- Data Lineage Compliance: Tracking the historical flow of ingestion parameters to ensure total audit visibility for regulators.

2. Machine Learning Model and Validation Frameworks

Model risk management standards dictate how banks deploy machine learning algorithms. Your platform requires a documented model inventory and clear evidence loops. Consequently, engineers must build champion-challenger model configurations to test operational updates safely.

- SAR Training Dataset Creation: Curating historic, labeled SAR data and narrative archives to train behavioral anomaly models effectively.

- Model Validation Documentation: Maintaining complete records to satisfy strict OCC, Federal Reserve, and SR 11-7 model risk guidance.

- Explainability Requirements: Integrating SHAP values to explain every risk score and eliminate opaque black-box decisions.

3. Human-in-the-Loop Investigation Workflows

The software must convert automated risk triggers into definitive case files for analysts. Therefore, the interface must prioritize human-in-the-loop design to facilitate rapid alert triage. The system accelerates reviewer actions by gathering all context into a single view.

- Automated Document Creation: Pulling merchant profiles and entity networks to streamline complex FinCEN SAR filing requirements.

- Audit Trail Requirements: Capturing all analyst notes, changes, and final decisions within immutable logging software layers.

- Parallel Run Requirements: Building user acceptance testing frameworks to validate system performance before full production deployment.

4. Infrastructure Security and Regulatory Defensibility

A bank-grade compliance network requires strict perimeter defenses and high availability. The infrastructure must handle multi-jurisdiction regulatory requirements without compromising speed. Furthermore, data residency requirements dictate precise cloud or on-premise infrastructure planning.

- Zero-Trust Security Controls: Deploying advanced encryption, role-based access control, and verified SOC 2 Type II environments.

- Low-Latency Performance: Utilizing Kafka streaming frameworks to power real-time monitoring across expanding fast-payment rails.

- Staff Onboarding and Training: Structuring staff training requirements and compliance officer onboarding pipelines before the official system launch.

Ultimately, compliance requirements should not begin with machine learning model selection. Instead, they must begin with the bank’s specific risk profile, available evidence, regulatory obligations, and operational review capacity.

For a deeper breakdown of financial crime monitoring architecture, see our guide on AI-powered transaction monitoring system development.

The Evidence Spine Banks Need Before the First Model

The most overlooked requirement for an AI AML platform is an evidence spine that connects every model score to source data, rule logic, analyst action, and final compliance decision. Without this spine, the bank may improve alert prioritization but still struggle to explain why a case was escalated, closed, or reported.

1. Key Evidence Architecture Components

- Data and Feature Lineage: Implements strict data lineage compliance by capturing transaction data snapshots and rule trigger states. This layout preserves the exact historical variables used by the system at the time of detection.

- Explainability Data Trails: Integrates precise SHAP values to fulfill the strict explainability requirements AML models must meet. This math breaks down opaque machine learning outputs into explicit, auditor-friendly risk factors.

- Human Action Capture: Enforces immutable logging requirements by tracking all internal analyst notes, manager approvals, and final SAR decision records. This permanent trail satisfies the core audit trail requirements banking groups need.

- System Validation Foundations: Automatically aggregates historical data parameters to maintain your model validation documentation. This process ensures your platform remains aligned with broad board oversight requirements AML AI programs demand.

| Evidence Layer | What It Captures | Why It Matters |

| Source data layer | Transaction, customer, counterparty, device, geography | Proves what the system saw |

| Feature layer | Velocity, frequency, amount, peer deviation, network link | Explains how risk was calculated |

| Detection layer | Rules, ML scores, graph signals, anomaly outputs | Shows why an alert was created |

| Review layer | Analyst action, approval, escalation, override | Proves human accountability |

| Reporting layer | SAR decision, narrative evidence, supporting records | Supports regulatory reporting |

| Governance layer | Model version, validation date, drift status, thresholds | Supports model risk management |

Ultimately, engineers must prioritize human-in-the-loop design requirements to preserve comprehensive FFIEC examination readiness across every operational layer. This architectural approach proves to regulators that your machine learning model can be fully trusted, explained, and legally defended under intense scrutiny.

Bank AML AI Platform Data Requirements

Bank AML AI platform data requirements include complete transaction history, customer profiles, KYC documents, CDD and EDD records, beneficial ownership data, alert outcomes, SAR filings, sanctions results, and case notes.

The platform needs enough clean, normalized, permissioned data to train, validate, monitor, and explain AML decisions across products and jurisdictions.

1. Transaction Data Requirements

Transaction data must include amount, currency, timestamp, channel, product, originator, beneficiary, counterparty, location, device, account status, and historical behavior. For real-time monitoring, the platform also needs event timestamps, payment state, settlement status, and data latency metrics.

- Core Systems Ingestion: Connects core banking data integration pipelines with payment processor data requirements. This process normalizes data flows from ACH, wire, card, real-time payments, wallet, trade finance, and correspondent banking.

- Message Formatting Standards: Maps incoming streams to fulfill SWIFT data format requirements and the modern ISO 20022 data standard. This ensures structural fields translate cleanly into usable features for downstream models.

- Data Volume Benchmarks: Ingests historical transaction records based on the Google Cloud AML AI guidelines. MVPs require 12 to 24 months of data, while strong typology modeling needs 24 to 60 months.

Once transaction streams are completely normalized, the system requires deep customer context to decide whether a specific financial activity is genuinely unusual.

2. Customer and Entity Data Requirements

Customer and entity data must include identity, occupation, business type, ownership, geography, expected activity, risk rating, account relationships, source of funds, and onboarding history. Without this context, an AI model may flag activity that looks unusual only because the customer profile is incomplete.

- Risk Profile Centralization: Compiles customer risk rating data alongside general entity data requirements AML teams rely on for investigations. This unifies fragmented records across core banking databases.

- Diligence Layer Integration: Aggregates historical CDD data requirements and EDD data requirements to establish baseline consumer behaviors. This context helps the platform identify deviations from expected financial activity.

- Ownership Graph Resolution: Parses complex beneficial ownership data structure formats to ensure strict KYC data completeness requirements are met. This step resolves hidden entity relationships across corporate account holders.

After the customer data layer is made usable, the development team must verify whether historic case labels are trustworthy enough for supervised machine learning.

3. Alert and SAR Data Requirements

Alert and SAR data must show which alerts were closed, escalated, linked to cases, converted into SARs, or rejected after review. This history helps train prioritization models, test false-positive reduction, and document whether the platform improves real AML decision quality.

- Training Label Validation: Audits historical alert disposition history data and labeled SAR data requirements to remove noisy training inputs. This cleanup ensures machine learning algorithms learn from accurate historical outcomes.

- Model Optimization Archives: Organizes a historical SAR training dataset to establish clear false positive threshold requirements and AML KPI baseline requirements. These baselines dictate how the model scores risk.

- Defensive Performance Audits: Compiles historical review logs to satisfy the rigorous backtesting data requirements AML compliance models face during validation. This loop proves model stability to internal risk teams.

Once the data foundation is clear, the platform must align with specific regulatory obligations before core infrastructure architecture begins.

AI AML Platform Regulatory Requirements Banks Must Map

AI AML platform regulatory requirements banks must map include BSA/AML program controls, SAR filing obligations, CDD, beneficial ownership, sanctions screening, record retention, model risk management, data privacy, third-party risk, and jurisdiction-specific AML rules.

These obligations shape architecture, workflow approvals, model explainability, reporting outputs, and audit evidence from the start.

1. BSA/AML and SAR Requirements

A bank AML AI platform must support suspicious activity monitoring, case documentation, SAR decisioning, filing timelines, confidentiality, and evidence retention. The platform should help staff identify and report suspicious activity, but final reporting decisions must remain with qualified compliance officers.

- Filing Pipeline Integration: Standardizes data pipelines to execute FinCEN SAR filing requirements and CTR filing requirements automatically. This ensures data matches official reporting specifications seamlessly.

- Internal Compliance Controls: Aligns system alert scoring logic with your bank’s foundational BSA program requirements. This setup ensures technical definitions mirror internal policy guidelines.

- Audit-Ready Quality Guidance: Organizes chronological transaction artifacts to build examiner-ready evidence for financial investigators. This framework structures historical case outcomes safely according to the FFIEC BSA/AML Examination Manual.

SAR workflows need customer due diligence and ownership data to support credible narratives.

2. CDD, EDD, and Beneficial Ownership Requirements

CDD, EDD, and beneficial ownership requirements define the customer context an AI AML platform must use. The system should understand customer identity, expected activity, risk profile, ownership structure, control persons, high-risk relationships, and ongoing monitoring changes before it scores suspicious behavior.

- Diligence Layer Mapping: Compiles fragmented user information into structured CDD data requirements and EDD data requirements. This tracks profile deviations dynamically as transaction patterns shift.

- Corporate Entity Verification: Parses complex beneficial ownership data structure formats to isolate high-risk customer monitoring signals. This process separates nested legal entities into visible structures.

- Profile Score Tracking: Feeds verified corporate documents into centralized customer risk rating data tables. This structure balances the ownership prong and control prong simultaneously during risk calculations according to OCC Risk Management Standards.

Once regulatory records are structured, the bank must decide where data can be processed and stored.

3. Data Residency and Cross-Border Compliance

Data residency requirements banking teams must review include where customer data, transaction history, model features, logs, and SAR evidence are stored and processed. Cross-border data compliance becomes critical when the platform serves global branches, offshore operations, correspondent banking, or outsourced review teams.

- Jurisdiction Footprint Planning: Configures underlying systems to follow data residency requirements banking networks enforce across geographic borders. This matches internal hosting architectures with physical data sovereignty requirements.

- Deployment Perimeter Controls: Directs processing streams through private cloud AML requirements or on-premise deployment requirements. This isolation preserves local bank privacy standards completely.

- Vendor Due Diligence Support: Records multi-region compliance logs to satisfy strict vendor due diligence requirements. This trail provides clear evidence for comprehensive third-party risk management audits.

Cross-border alignment requires global tracking across varying framework mandates.

4. Global and Multi-Jurisdiction Regulatory Alignment

Multi-jurisdiction operations require real-time mapping of global financial crime frameworks across distinct legislative zones. The platform architecture must accommodate varying data standards and filing windows without interrupting localized detection engines.

- Global Framework Adherence: Integrates standardized rules to maintain FATF recommendation compliance across sovereign territories. This aligns baseline behavioral flags with international expectations.

- Localized Enforcement Mapping: Customizes workflows to execute specialized regional directives. This step embeds precise FCA AML requirements UK teams use, MAS AML requirements Singapore dictates, and AMLD6 requirements Europe enforces.

- Interoperable Alert Routing: Segregates local investigations while synchronizing risk typologies across the entire global business enterprise. This protects individual privacy while preventing corporate-wide systemic exposure.

Regulatory mapping then informs the architecture the bank should build.

Technical Requirements AI AML Platform Banking Teams Need

Technical requirements AI AML platform banking teams need include secure ingestion, data normalization, entity resolution, feature engineering, real-time scoring, batch analytics, graph analytics, case management, model serving, MLOps, audit logging, and API integration. These components must support low-latency monitoring without losing explainability, security, or regulatory traceability.

Therefore, your technical layout dictates how well the system processes raw financial activity without compromising bank performance.

1. Real-Time Monitoring Infrastructure

Real-time monitoring infrastructure should score events before money movement becomes difficult to interrupt. Banks need streaming ingestion, low-latency APIs, sanctions checks, customer-risk context, and escalation workflows that can hold, approve, reject, or route transactions based on defined authority rules.

- Streaming Queue Architecture: Employs precise Kafka streaming requirements to ingest live financial records across payment processor data requirements. This setup ensures continuous event tracking without data drops.

- Performance Optimization Limits: Minimizes transaction delays by establishing strict low-latency processing requirements within the core banking data integration layer. This constraint ensures live scoring occurs under sub-second thresholds.

- Interoperable Interface Engineering: Integrates clean API integration requirements AML platforms use to coordinate flags across core payment engines instantly. This pipeline facilitates rapid data sharing during execution.

Real-time scoring handles immediate activity, but batch analytics finds longer patterns.

2. Batch Monitoring and Graph Analytics

Batch monitoring and graph analytics detect laundering patterns that do not appear in a single payment. These systems analyze customer networks, shared counterparties, ownership links, device overlap, transaction chains, and repeated movement across time windows.

- Network Relationship Engines: Utilize specific graph database requirements AML software maps to expose hidden mule network detection paths. This framework links disconnected accounts through shared attributes.

- Analytical Integration Steps: deploys deep Neo4j graph analytics requirements over clean entity data requirements AML teams rely on for deep investigation. This uncovers circular layering strategies across multiple entities.

- Ownership Structure Mapping: Unfolds a complex beneficial ownership data structure into visible node relationships to trace hidden ultimate control. This visualization reveals illicit networks trying to hide behind nested corporations.

3. Platform Infrastructure and Deployment Architecture

| Layer | Requirement | Why It Matters |

| Data Ingestion | APIs, event queues, batch loaders | Pulls activity from core systems |

| Normalization | Canonical AML data model | Makes old and new data usable |

| Entity Resolution | Customer, account, device, counterparty matching | Connects hidden relationships |

| Feature Engineering | Velocity, peer behavior, network risk | Feeds AML models |

| Detection | Rules, ML, graph analytics, typology logic | Identifies suspicious patterns |

| Case Workflow | Alerts, queues, reviewer actions | Turns scores into investigations |

| Reporting | SAR, CTR, evidence exports | Supports compliance obligations |

| MLOps | Versioning, monitoring, retraining | Keeps models defensible |

| Security | RBAC, encryption, logging, network controls | Protects sensitive bank data |

4. Cloud and Deployment Infrastructure Models

Enterprise environments mandate highly secure, performant hosting setups that adapt to strict institutional risk profiles. System planners must choose infrastructure footprints that reconcile scaling demands with local data protection laws.

- Private Cloud Environments: configure private cloud AML requirements to run within isolated corporate virtual spaces. This combines modern scaling benefits with enterprise perimeter defenses.

- On-Premise Infrastructure Options: Sustains localized server arrays to answer strict on-premise deployment requirements that some traditional banking licenses require. This ensures direct asset ownership and execution monitoring.

- Rigorous Platform Security: Implements role-based access control, comprehensive data encryption, and deep monitoring logs to fulfill all cloud infrastructure requirements banking environments enforce. This step protects sensitive records from internal and external threats.

With architecture defined, banks must choose the AI models that fit the AML workflow.

ML Model Requirements AML Platform Teams Should Define

ML model requirements AML platform teams should define include model purpose, input features, training labels, validation method, performance thresholds, explainability outputs, retraining triggers, drift monitoring, and reviewer controls.

A bank should not approve one generic AI model for AML because transaction monitoring, case triage, sanctions context, and SAR drafting need different model designs.

1. Supervised Risk Scoring Models

Supervised risk scoring models work best when banks have reliable historical labels from confirmed alerts, SARs, escalations, and analyst decisions. These models can prioritize alerts, reduce low-value reviews, and rank suspicious activity, but only when the training data reflects real risk outcomes.

- Training Signal Curation: Assembles verified records to fulfill labeled SAR data requirements and alert disposition history data parameters. This filters out historically noisy alerts from the core model.

- Historical Behavioral Baselines: Syncs model training with comprehensive historical transaction data requirements across multi-year accounting cycles. This provides a clear mathematical baseline of normal institutional behavior.

- Validation Protocol Setup: Generates retroactive alert matches to satisfy backtesting data requirements AML review boards examine closely. This verification confirms that the system meets target false positive threshold requirements.

When labels are weak, anomaly detection and graph models become more useful.

2. Anomaly Detection and Behavioral Models

Anomaly detection models help banks identify unusual behavior without relying only on past SAR labels. These models compare customer activity against historical behavior, peer groups, expected transaction patterns, velocity changes, and high-risk deviations.

- Dynamic Attribute Structuring: Aggregates centralized customer risk rating data to map current transaction patterns against verified consumer profiles. This establishes distinct behavioral baselines across variable account segments.

- Advanced Target Calculation: Directs core system features through custom feature engineering requirements AML architectures need for outlier detection. This allows the system to identify extreme peer group analysis deviations automatically.

- System Stability Auditing: Sets operational checkpoints to execute model performance monitoring requirements continuously. This setup detects when changing consumer habits trigger inaccurate behavioral anomalies.

Some laundering patterns require relationship analysis, not isolated account scoring.

3. Graph Analytics and Entity Resolution Models

Graph analytics models help banks detect hidden relationships across customers, accounts, businesses, devices, counterparties, and beneficial owners. These models are useful for mule networks, layering, shell company patterns, circular payments, and shared-control structures.

- Network Relationship Mapping: Configures graph database requirements AML systems depend on to stitch together disconnected entity data requirements AML teams monitor. This exposes complex circular payment networks instantly.

- Multi-Source Graph Analytics: Harnesses explicit Neo4j graph analytics requirements to trace overlapping physical data attributes. This maps cross-account linkages by checking shared phone numbers, devices, or addresses.

- Data Asset Synchronization: Feeds a complex beneficial ownership data structure alongside sanctions database integration requirements and blockchain analytics requirements into the graph. This reveals hidden connections to high-risk PEPs or addresses.

4. Model Governance and Explainability Workflows

Institutional safety requires that advanced software platforms submit to strict administrative supervision structures. Teams must build explicit engineering controls around their machine learning models to satisfy model risk management requirements.

- Algorithmic Safety Testing: Establishes rigorous champion-challenger model requirements to evaluate operational code updates against live production systems safely. This deployment strategy eliminates unexpected disruptions during compliance updates.

- Defensible Score Dissemination: Employs SHAP values as a commonly used explainability method to document individual risk calculations. This math explicitly ranks exactly which transactional variables caused the system to fire an alert.

- Operational Control Loops: Enforces human-in-the-loop design requirements by giving analysts direct tools to validate, score, or overwrite algorithmic recommendations. This oversight creates an audit trail that proves humans manage the system.

Once detection models are defined, the bank must govern them under model-risk standards.

Model Risk Management Requirements for AI AML Systems

Model risk management requirements for AI AML systems include model inventory, conceptual soundness review, independent validation, performance testing, backtesting, documentation, governance, ongoing monitoring, challenger models, change control, and vendor oversight.

Banks must prove that AML models are accurate enough, explainable enough, and controlled enough for their intended compliance use.

1. Model Inventory and Use Classification

Every AML AI model should enter the bank’s model inventory before production use. The inventory should identify model owner, business purpose, inputs, outputs, users, limitations, validation status, deployment environment, vendor dependencies, and risk tier.

- System Asset Mapping: Logs comprehensive model inventory requirements by tracking the designated model owner and recording explicit use case classification parameters. This centralizes vital visibility for internal auditing teams.

- Dependency and Tier Tracking: Identifies all third-party model dependencies while assigning a specific operational risk tiering value to each codebase. This ensures the system tracks active validation status in real time.

- Formal Approval Workflows: Documents the definitive system approval status across distinct business groups before pushing updates to active payment rails. This control prevents unverified code from impacting daily compliance queues.

After inventory, validation must prove that the model works for the bank’s actual risk profile.

2. Validation, Backtesting, and Challenger Models

Validation must test whether the AML model performs reliably on historical, out-of-sample, and changing transaction patterns. Banks should compare the model against existing rules, analyst outcomes, and challenger models before production rollout.

- Defensible Record Compilation: Generates structured model validation documentation that justifies algorithmic assumptions and testing parameters. This serves as the primary technical defense during rigorous examiner reviews.

- Retroactive Scoring Diagnostics: Collects localized data subsets to satisfy complex backtesting data requirements AML review boards demand. This history confirms model performance monitoring requirements are achieved without accuracy degradation.

- Parallel Competitive Testing: Runs dedicated champion-challenger model requirements to contrast active detection engines against experimental configurations. This continuous outcome analysis checks for parameter drift testing anomalies over time.

Validation gives approval evidence, but explainability gives investigation evidence.

3. Explainability and Human Review

Explainability requirements AML models must meet include risk reason codes, contributing factors, feature importance, relationship paths, transaction evidence, and reviewer override visibility. Human reviewers must understand why the system escalated, prioritized, or recommended a case action.

- Advanced Attribution Integration: Deploys the SHAP values regulatory requirement framework as a practical explainability method within your analyst screens. This translates multi-layered risk weights into transparent reason codes.

- Operational Control Workflows: Enforces human-in-the-loop design requirements by anchoring automated alerts to mandatory manual approval workflows. This structure guarantees that skilled compliance professionals check every system output.

- Defensible Action Logging: Captures all reviewer-approved narrative drafting steps alongside real-time override logging metrics inside the audit database. This permanent trail shows regulators that the bank retains full operational command.

Ultimately, modern banks must recognize that building an AI AML system requires satisfying strict administrative supervision frameworks. This structural development ensures your compliance architecture scales efficiently under intense regulatory pressure. Governed models still need secure integrations to work inside a bank’s live environment.

Integration Requirements for AI AML Compliance Platforms

AI AML compliance platform build requirements include integrations with core banking systems, payment processors, KYC providers, sanctions databases, case management tools, document stores, graph databases, cloud infrastructure, reporting systems, and model governance tools.

Integration quality determines whether the platform becomes daily compliance infrastructure or another disconnected dashboard.

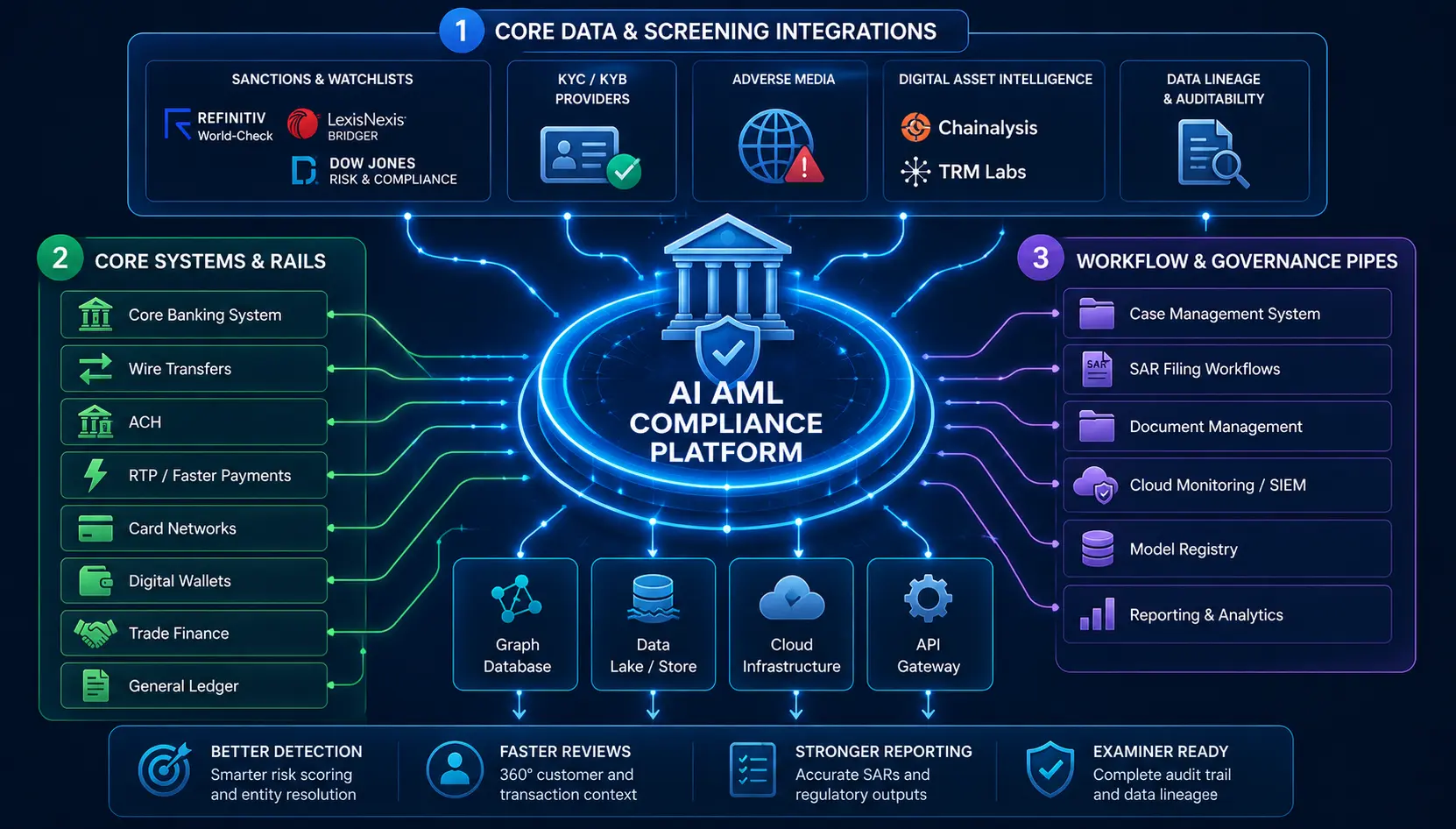

1. Core Data and Screening Integrations

Establishing a unified financial crime ecosystem requires strict connectivity across diverse identity and validation networks. Consequently, technical teams must design specialized API integration requirements AML platforms rely on to feed real-time risk scores into your pipeline.

- Sanctions Ecosystem Sourcing: Implements robust sanctions database integration requirements to synchronize operational records continuously. This setup pulls active watchlists directly from Refinitiv World-Check requirements, LexisNexis Bridger requirements, and Dow Jones Risk requirements.

- Digital Asset Infrastructure: Embeds specialized Chainalysis integration requirements and TRM Labs requirements if your institution handles crypto assets. This tracking exposes exposure to illicit wallets and decentralized protocol vulnerabilities instantly.

- Auditability and Lineage Preservation: Configures data pipelines to preserve absolute data lineage, latency metrics, and auditability during ingestion. This guarantees that external screening changes do not break down historical evidence trails.

2. System Connectivity Integration Checklist

- Core Systems and Rails: Connects the core banking ledger directly to wire, ACH, RTP, card, wallet, and trade finance transaction feeds.

- Identity and Verification Layers: Hooks into external KYC/KYB providers, beneficial ownership registries, and automated adverse media scraping software.

- Workflow and Governance Pipes: Integrates your internal case management system, automated FinCEN SAR filing workflows, cloud monitoring tools, and model registries.

Ultimately, modern banking institutions must execute deep vendor due diligence requirements to protect core system access securely. This rigorous vetting process ensures your third-party risk management framework satisfies intense regulatory scrutiny before deployment.

In conclusion, integration requirements should always be scoped entirely by specific evidence needs rather than arbitrary feature counts. Every single connected system should visibly improve overall detection, analyst review speed, regulatory reporting quality, or examiner reconstruction accuracy.

Security and Infrastructure Requirements AML Platforms Need

Security and infrastructure requirements AML platforms need include encryption, role-based access control, zero-trust architecture, secure APIs, private cloud or on-premise deployment options, immutable logs, penetration testing, SOC 2 controls, data residency enforcement, secrets management, disaster recovery, and continuous monitoring.

Therefore, AML platforms process highly sensitive financial and investigative data.

1. Core Security Architectures and Vetting Protocols

Protecting institutional transaction pipelines requires implementing tight boundary controls around data storage, access privileges, and processing nodes. Consequently, system engineers must align system components with strict cloud infrastructure requirements that banking networks enforce across production environments.

- Deployment Perimeter Options: Implements secure private cloud AML requirements or on-premise deployment requirements based on the bank’s charter rules. This isolation keeps highly confidential customer data safely inside authorized networks.

- Zero-Trust and Access Control: Deploys strict zero-trust architecture requirements by combining granular role-based access control requirements with absolute encryption requirements that banking authorities mandate. This structure enforces least-privilege policies across all analyst levels.

- Operational Validation Checks: Validates system integrity by completing SOC 2 Type II requirements audits alongside aggressive annual penetration testing requirements. These checks provide clear verification of third-party risk management protections.

2. Critical Bank Security Controls

| Control | Requirement | Bank Review Owner |

| Encryption | Data at rest and in transit | CISO |

| RBAC | Analyst, reviewer, admin, auditor roles | Compliance + Security |

| Immutable logs | Case, model, and reviewer history | Risk + Audit |

| Zero trust | Least privilege and segmented access | Security |

| Pen testing | Pre-launch and post-change testing | Security |

| SOC 2 mapping | Vendor and platform control evidence | Procurement + Risk |

| Data residency | Regional storage and processing rules | Legal + Compliance |

| Disaster recovery | RTO/RPO and backup procedures | IT Operations |

Ultimately, banking compliance leads must evaluate data touchpoints carefully if the platform interacts with healthcare or insurance payments. For instance, specific BAA requirements AML vendors face apply only when processing health-fintech or clinical data workflows, whereas standard banking data requires traditional financial data protections.

In conclusion, AML system security must never be viewed as a basic, one-off cybersecurity box to check. Instead, your deployment strategy directly protects the physical legal standing, examiner trust, and operational continuity of the entire financial institution.

AI AML Platform Development Cost for Banks

Enterprise AI AML platforms cost $60,000 to $250,000 with annual maintenance at 18 to 25% for banks, depending on data readiness, transaction volume, payment rails, model complexity, real-time processing, vendor integrations, security requirements, validation needs, and multi-jurisdiction compliance scope. A controlled MVP costs less than a full financial crime platform replacing legacy monitoring infrastructure.

Consequently, project budgets shift dramatically based on specific structural engineering complexities and institutional risk targets. Therefore, your development team must evaluate your underlying technical ecosystem before allocating physical software capital.

Phase-by-Phase Platform Cost Breakdown

| Development Phase | Estimated Cost |

| Discovery, risk scope, and requirements | $15,000–$40,000 |

| Data audit and readiness assessment | $25,000–$75,000 |

| Data pipelines and normalization | $35,000–$120,000 |

| Core banking and payment integrations | $40,000–$150,000 |

| AI risk scoring and anomaly models | $50,000–$160,000 |

| Graph analytics and entity resolution | $45,000–$140,000 |

| Case management and SAR workflows | $40,000–$130,000 |

| Model validation and MRM documentation | $30,000–$100,000 |

| Security, RBAC, logging, and infrastructure | $35,000–$120,000 |

| UAT, parallel run, and deployment | $25,000–$90,000 |

Core Cost Drivers and Maintenance Calculations

Annual maintenance typically ranges from 18% to 28% of the initial build cost. This covers model monitoring, retraining, alert tuning, regulatory updates, security patches, vendor API changes, infrastructure optimization, and compliance documentation updates.

- Data Quality AML Platform Conditions: Baseline data quality AML platform teams find drives cost because dirty, non-normalized records require heavy upfront parsing. This formatting work expands development timelines significantly.

- Pipeline and Processing Complexity: Ingesting multiple real-time payment rails costs substantially more than setting up standard batch-processing structures. Real-time environments require high-availability infrastructure and immediate API connections.

- Integration and Governance Scopes: Connecting multiple sanctions, adverse media, and graph database providers expands total engineering hours. Furthermore, satisfying strict multi-jurisdiction regulatory requirements and model validation rigor balloons overall documentation budgets.

For a deeper cost view of AML copilot workflows, see our guide on AI AML compliance copilot cost.

Ultimately, scaling your software layout carefully controls unexpected capital outlays during product construction. By locking down integration footprints early, your risk team ensures the system scales efficiently under intense regulatory pressure.

Build an AI AML Platform With Intellivon

Intellivon helps banks, credit unions, fintech platforms, and financial institutions build AI AML platforms around real compliance workflows, not isolated AI experiments. The work starts with your AML risk profile, available data, regulatory obligations, operating model, and existing technology stack. From there, Intellivon designs the platform architecture, data pipelines, AI models, case workflows, validation controls, and rollout plan needed to move from internal approval to production.

For banks, the goal is not only to detect suspicious activity faster. The platform must help compliance teams explain why an alert was created, which evidence supported the decision, who reviewed the case, what model version produced the score, and how the final SAR decision was approved. That is why Intellivon builds AI AML systems around traceability, model governance, human review, and examiner-ready documentation from the beginning.

1. What Intellivon Helps You Build

- Risk-scoped AML architecture: Define the first release around your customer segments, payment rails, jurisdictions, transaction volume, and highest-risk typologies.

- AML data readiness layer: Prepare historical transaction data, KYC records, CDD and EDD profiles, beneficial ownership data, alert history, SAR outcomes, and case notes for model development.

- Transaction monitoring intelligence: Build AI-assisted detection across real-time and batch workflows using rules, anomaly detection, risk scoring, graph analytics, and entity resolution.

- Explainable model workflows: Design AI outputs with reason codes, supporting evidence, reviewer visibility, confidence scoring, and human approval checkpoints.

- Investigation and case intelligence: Route high-risk alerts, group related activity, surface customer context, summarize evidence, and support analyst decisions without removing human accountability.

- SAR evidence and reporting support: Help teams prepare reviewer-approved SAR narratives with transaction facts, customer context, linked cases, and documented escalation logic.

- Model risk and validation controls: Create the documentation, monitoring, testing, backtesting, and approval workflows needed for controlled AI use in banking.

- Security and audit infrastructure: Preserve access controls, immutable logs, data lineage, encryption, deployment controls, and examiner-ready evidence across the platform.

2. When to Work With Intellivon

Work with Intellivon when your bank has outgrown basic rule tuning and needs a controlled AI AML platform built around your own risk profile. This is especially relevant if your teams are dealing with high alert volumes, fragmented KYC data, disconnected case systems, weak SAR evidence trails, poor entity resolution, or limited visibility across payment channels.

Intellivon is also a strong fit when your leadership team needs a clear build plan before committing budget. That includes a requirements checklist, architecture roadmap, cost range, timeline, integration scope, data readiness review, and model-risk plan.

3. What You Get Before Full Development Begins

Before engineering starts, Intellivon can help your team define the core requirements that decide whether the project is build-ready. This gives your CTO, Chief Compliance Officer, Chief Risk Officer, and program leads a clearer path to internal approval.

The early-stage roadmap can include:

- AML risk scope and platform use-case definition

- Data readiness and data quality assessment

- Core banking and payment integration map

- AI model and feature engineering plan

- Case workflow and SAR evidence design

- Security, audit, and access-control requirements

- Model validation and monitoring framework

- Phase-wise cost and delivery roadmap

- MVP versus production-release recommendation

4. Why This Matters

A strong AI AML platform should not create another black-box system for compliance teams to defend. It should give your analysts better evidence, your risk teams better controls, your technology teams cleaner architecture, and your leadership team a clearer view of cost, scope, and operational impact.

Intellivon builds with that reality in mind. Every model, workflow, integration, and audit trail is designed to support practical AML operations, not just technical performance.

If your bank is evaluating AI AML platform development, start with a requirements and readiness discussion before choosing models or vendors. Talk to Intellivon to scope your AI AML platform architecture, data requirements, compliance controls, integrations, development cost, and rollout roadmap before committing to a full build.

Conclusion

Building an enterprise AI AML platform requires a unified framework that balances data readiness, clear model governance, and strict regulatory alignment. Consequently, banks must treat this software as core compliance infrastructure rather than a generic analytics dashboard.

By prioritizing a transparent evidence spine and secure architectural integrations from day one, your risk team ensures the finished system delivers legally defensible decisions that easily withstand intense regulatory scrutiny during examinations.

Things To Know About AI AML Platform Development

Q1. How long does it take to build AML AI platform workflows?

A1. Consequently, establishing a controlled MVP usually takes 14 to 20 weeks when data access and compliance integration points are ready. However, a production bank deployment typically requires 6 to 12 months because data normalization and model validation take time. Therefore, multi-region platforms can extend this baseline timeline significantly.

What it takes to build AML AI platform architectures depends entirely on your initial system testing readiness.

Q2. What AI AML platform development requirements banks should approve first?

A2. Therefore, banks must approve risk scope, data requirements, model-risk controls, human-review rules, integration scope, security parameters, and operating ownership immediately. This sequence prevents teams from selecting models before compliance can explain outputs. Consequently, the strongest approval pack incorporates an architecture map, cost range, timeline, and validation plan.

AI AML platform development requirements banks evaluate first dictate long-term production safety.

Q3. What are the bank AML AI platform data requirements?

A3. Bank AML AI platform data requirements include transaction history, KYC records, CDD and EDD data, customer risk ratings, beneficial ownership records, and historical SAR outcomes. Therefore, banks should start with 12 to 24 months of usable history for an MVP. However, richer models require longer, cleaner historical transaction histories to perform accurately.

This core framework ensures your transaction pipelines remain consistent across expanding multi-jurisdiction rails.

Q4. Can AI write SAR narratives for banks?

A4. Importantly, AI can draft SAR narratives, but it should never file them or make final reporting decisions without manual oversight. Consequently, the safest workflow uses algorithms to assemble transaction evidence, summarize suspicious patterns, and prepare reviewer-approved drafts. Therefore, according to discussions on Reddit, every narrative claim must trace back to verified source transactions.

To Sum Up:

- Banks do not need “more AI” in AML first. They need better evidence continuity from transaction data to SAR decisions.

- A model that reduces alerts can still fail bank review if analysts cannot explain why each case was closed, escalated, or reported.

- The most expensive AI AML builds usually become expensive before coding starts, because legacy data lacks ownership, lineage, and usable labels.

- A strong AI AML platform should improve detection and documentation at the same time.

- Custom AML AI makes sense when the bank’s risk logic, data control, workflows, or integrations create strategic value.