Building a B2B global payments platform at enterprise scale involves a key decision about infrastructure. This choice affects how businesses move money, manage risk, and compete internationally. Companies like SoFi didn’t succeed by just copying existing banking systems. They thrived by rethinking how financial infrastructure should work in a world where speed, compliance, and transparency are essential.

The need for smart, scalable cross-border payment systems is growing quickly. This is because businesses that operate in multiple regions need platforms that can handle currency conversion, regulatory compliance, fraud detection, and real-time settlement at the same time, smoothly. However, getting this right involves more than just putting together APIs. It requires careful planning, thorough compliance engineering, and a solid understanding of where the real challenges are before writing any code.

This blog explains what it takes, covering core architecture, integration layers, compliance frameworks, and scalability choices. At Intellivon, we design and provide enterprise-grade payment infrastructure for these types of environments. That experience shapes everything that you are about to read here.

Why Is SoFi a B2B Global Payments Benchmark?

SoFi is emerging as a B2B global payments benchmark by combining a regulated, nationally chartered bank with an API-driven platform. It supports 24/7 movement of both fiat and stablecoins. At the same time, it integrates directly with major payment rails like Mastercard and fintech infrastructure through Galileo.

As a result, enterprise and fintech partners use SoFi as a payment infrastructure layer embedded within their own systems.

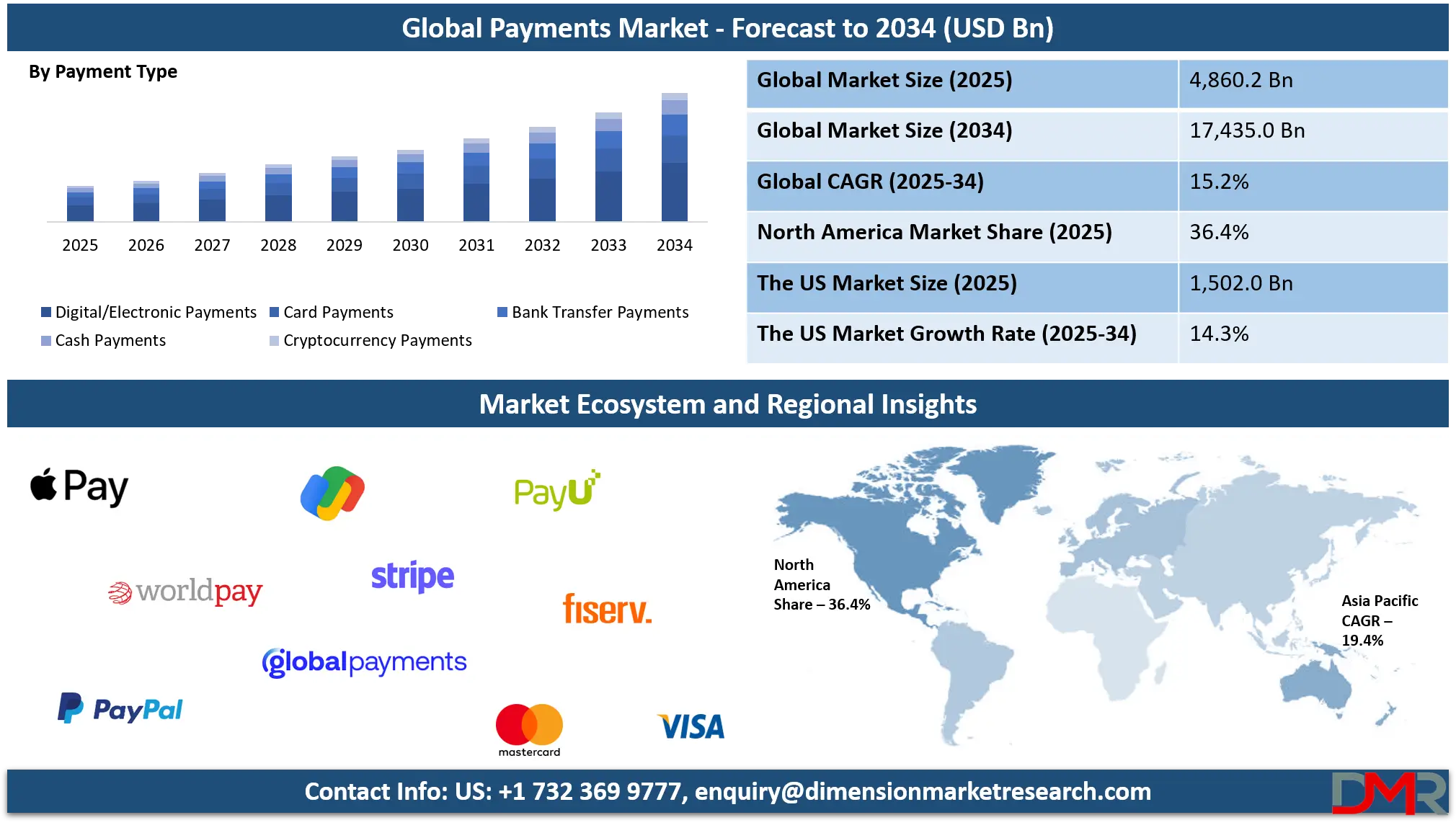

Another reason behind SoFi’s success is the market trajectory of global payments in general. The global payments market is projected to reach USD 4,860.2 billion in 2025. It is expected to grow at a CAGR of 15.2%, reaching USD 17,435.0 billion by 2034.

SoFi transformed the industry by moving beyond its initial niche. It proved that a B2B payments platform succeeds when it stops being a utility and starts being an ecosystem.

1. From student lending to a full fintech ecosystem

Success in the modern market starts with solving one high-friction problem exceptionally well. For SoFi, this was student debt, but the goal was always larger.

They leveraged that initial trust to build a comprehensive suite of banking, investment, and payment tools. This evolution shows that a B2B platform must eventually address every touchpoint of a user’s financial journey to remain relevant.

2. Shift from single-product to platform thinking

Single-feature products are easily replaced by cheaper competitors. Platform thinking involves creating an architecture where each new service adds value to the existing ones.

In a global payments context, this means integrating treasury management with real-time FX hedging. Enterprises prefer a unified interface over managing twenty different vendor relationships for their global cash flow.

3. Owning the complete financial lifecycle

Retaining a customer for decades requires capturing their needs at every growth stage.

- Startup Phase: Focus on low-cost domestic transfers.

- Expansion Phase: Provide multi-currency accounts and cross-border payroll.

- Maturity Phase: Offer sophisticated credit lines and automated liquidity management.

4. Unified financial experience as a competitive moat

Complexity is the enemy of the enterprise user. By providing a “single pane of glass” for global transactions, a platform reduces operational risk.

When payments, compliance, and reporting live in one place, the cost of switching to another provider becomes prohibitively high.

5. Scaling through infrastructure ownership

A true benchmark company like SoFi owns the rails. By acquiring or building its core processing layers, a platform gains better margins and faster deployment cycles.

This independence allows for deeper customization, which is a critical requirement for large-scale enterprise clients.

The SoFi model demonstrates that market leadership is won through integration and the elimination of financial silos. For investors, the value lies not in the individual payment but in the total ownership of the financial stack.

What Is a B2B Global Payments Platform?

A B2B global payments platform is an enterprise financial infrastructure that enables businesses to send, receive, and settle transactions across borders, handling multi-currency conversion, compliance, fraud detection, and real-time settlement within a single system.

Unlike consumer payment tools, B2B platforms are built for high transaction volumes, complex regulatory environments, and deep integration with enterprise financial systems.

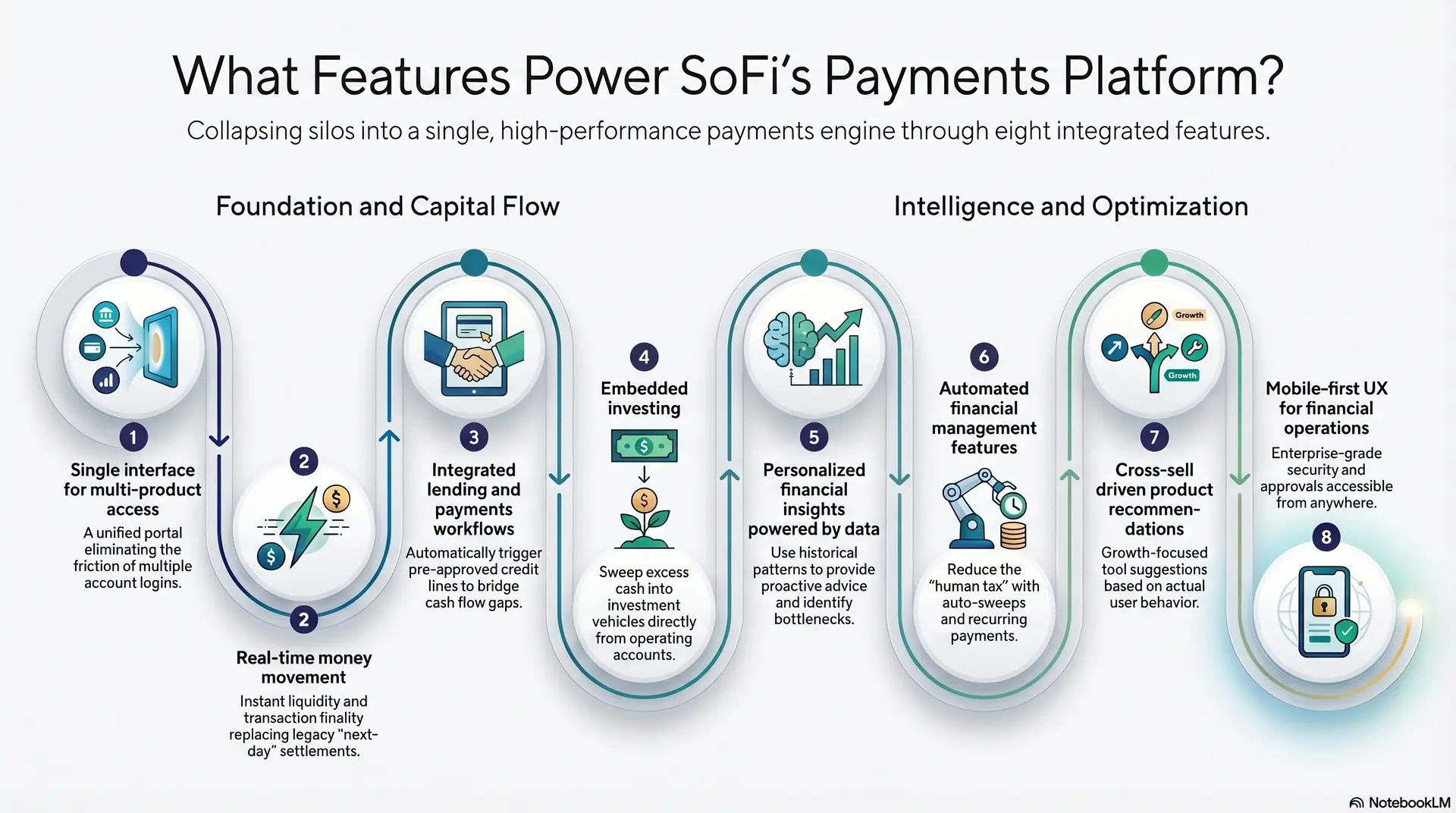

What Features Power SoFi’s Payments Platform?

The strength of this model lies in its ability to collapse traditional banking silos into a single, high-performance engine that handles more than just moving capital.

1. Single interface for multi-product access

The platform acts as a unified portal where users manage diverse financial needs without switching accounts. This “single pane of glass” philosophy eliminates the friction of logging into multiple portals for payroll, FX, and credit.

For a business leader, this means reduced training time and a much lower risk of manual data entry errors.

2. Real-time money movement

Modern commerce moves instantly, and legacy “next-day” settlement is becoming obsolete. A robust B2B payments platform must provide instant liquidity visibility and immediate transaction finality.

- Instant Settlement: Utilizing modern rails to move funds in seconds.

- Live Ledgers: Ensuring the dashboard reflects current balances across all currencies.

- Audit Readiness: Maintaining a continuous, real-time log of every movement for compliance.

3. Integrated lending and payments workflows

Friction occurs when credit and payments live in different worlds. By embedding lending directly into the payment flow, a business can bridge cash flow gaps automatically.

For instance, if an outgoing vendor payment exceeds current cash reserves, the platform can trigger a pre-approved line of credit to ensure the transaction completes without delay.

4. Embedded investing

Idle capital is wasted capital. A sophisticated platform allows users to sweep excess cash into low-risk investment vehicles directly from their operating account.

This feature transforms the payments platform from a mere spending tool into a strategic asset that generates yield on operational floats.

5. Personalized financial insights powered by data

Data is only valuable if it is actionable. The platform uses historical transaction patterns to provide proactive advice, such as identifying upcoming seasonal cash crunches.

These insights help decision-makers pivot strategies before minor issues become major operational bottlenecks.

6. Automated financial management features

Automation reduces the “human tax” on financial operations.

- Auto-Sweeps: Automatically moving funds between accounts based on set thresholds.

- Recurring Payments: Scheduling vendor settlements to avoid late fees.

- Smart Allocation: Directing incoming funds to specific tax or reserve accounts instantly.

7. Cross-sell driven product recommendations

The platform grows alongside the business by suggesting the right tools at the right time. If the system detects a spike in international transactions, it might recommend an FX hedging tool. This is a consultative approach that adds value based on actual user behavior.

8. Mobile-first UX for financial operations

Decision-makers are often on the move. A mobile-first approach ensures that high-level approvals, urgent transfers, and balance checks are accessible from anywhere.

The goal is to provide enterprise-grade security and depth without sacrificing the speed and ease of a consumer-grade mobile application.

By centralizing these features, the platform moves from being a simple vendor to an essential operational partner. It creates a seamless environment where capital flows as fast as the information that drives it.

How Does SoFi Secure Its Payments Platform?

A benchmark platform treats security as a proactive feature rather than a reactive barrier. It integrates protection into every layer of the user journey, ensuring that safety never compromises speed.

1. Regulatory alignment across financial services

Operating a B2B payments platform requires strict adherence to global and local laws. This means maintaining licenses and staying compliant with frameworks like SOC2, GDPR, or specific banking regulations in every operating region.

By aligning with these standards, the platform provides a safe environment where enterprise leaders can move capital without fearing legal repercussions.

2. KYC and AML as onboarding foundations

Knowing Your Customer (KYC) and Anti-Money Laundering (AML) protocols are the first line of defense.

- Identity Verification: Using biometric and document scanning to confirm user authenticity.

- Vetting: Checking entities against global watchlists and sanctions.

- Speed: Implementing automated workflows so that rigorous checks don’t slow down the onboarding experience.

3. Encryption standards across all transactions

Data must be unreadable to unauthorized parties, whether it is sitting in a database or moving across the internet. Utilizing AES-256 for data at rest and TLS 1.3 for data in transit ensures that sensitive financial information remains private.

This level of encryption is the gold standard for protecting corporate secrets and transaction histories from sophisticated cyber threats.

4. Real-time fraud detection and monitoring

The system must be able to spot a threat before the money leaves the account. Advanced monitoring tools analyze thousands of transactions per second to find anomalies.

If a payment looks out of character for a specific business, such as an unusual destination or a sudden spike in volume, the system can flag it for human review or block it instantly.

5. Risk scoring across user activity patterns

Security is improved when the platform understands what “normal” looks like. By assigning a risk score to every user based on their behavior, the platform can apply “step-up” authentication only when necessary.

This means a low-risk recurring payroll run happens smoothly, while a high-risk transfer to a new vendor might trigger additional security prompts.

6. Secure identity and access management controls

Enterprise leaders need granular control over who can do what. Multi-factor authentication (MFA) and Single Sign-On (SSO) integrations are essential for preventing unauthorized access.

- Role-Based Access: Ensuring a junior clerk cannot authorize a million-dollar transfer.

- Audit Trails: Keeping a permanent record of every login and change made within the system.

- Session Management: Automatically logging out inactive users to prevent local breaches.

7. Transparent fee and transaction visibility

Hidden fees and “ghost” transactions destroy trust. A secure platform ensures every penny is accounted for with clear, itemized reporting.

When a CFO can see exactly where money is and why a certain fee was charged, it eliminates the uncertainty that often surrounds cross-border payments.

8. Trust as a product experience layer

Ultimately, security should feel invisible but reassuring. The UI should communicate safety through clear confirmations and proactive alerts. When users feel the platform is looking out for them, they are more likely to deepen their engagement and use more advanced financial products.

Building a secure platform like SoFii rests on creating a stable foundation where global trade can happen with total confidence.

What Is SoFi’s Payments Platform Revenue Model?

The core of this model is diversification. By spreading income across multiple channels, the platform remains resilient even when market interest rates or transaction volumes fluctuate.

1. Lending margins and interest income streams

While the platform facilitates payments, it often acts as a balance-sheet player. By holding deposits and issuing loans, the system earns on the “net interest margin”, the difference between the interest paid to depositors and the interest earned from borrowers.

This is a massive revenue driver for platforms that integrate banking licenses with payment rails.

2. Interchange and payment processing fees

Every time a corporate card is swiped or a cross-border transaction is initiated, a small percentage is captured as an interchange fee.

- Transaction Volume: Revenue scales directly with the growth of the client’s business.

- Network Fees: Small, consistent margins that provide a steady “top-line” flow.

- FX Spread: Earning a margin on the currency conversion for international transfers.

3. Investment and trading monetization

Platforms that offer wealth management or treasury services can monetize through management fees or “payment for order flow.”

When an enterprise invests its idle cash into money market funds or stocks via the platform, the service provider earns a small commission or a fraction of the assets under management (AUM).

4. Subscription and premium tier offerings

Predictable revenue often comes from monthly or annual SaaS fees.

- Basic Tier: Essential payment tools with standard processing rates.

- Premium Tier: Advanced reporting, lower FX margins, and dedicated account management.

- Enterprise Tier: Custom API integrations and white-labeling options for a fixed monthly cost.

5. Cross-product monetization strategy

The “SoFi way” involves getting a user through the door with one product and then moving them to others. If a client joins for a B2B debit card, the platform might eventually monetize through an enterprise loan or a secondary insurance product.

This reduces the cost of acquisition per product and maximizes the utility of the existing infrastructure.

6. Customer lifetime value optimization

Success is measured by how much a client is worth over several years, not just one month. By offering a full suite of services, the platform becomes deeply embedded in the client’s operations.

This “stickiness” ensures that the revenue continues to flow for years, far outweighing the initial cost spent to acquire that business.

7. Data-driven upsell and cross-sell revenue

Algorithms analyze spending patterns to identify when a business needs more capital. By offering a pre-approved loan exactly when the data shows a cash-flow gap, the platform increases its conversion rates.

This proactive selling is far more efficient than traditional cold outreach and creates a “consultative” revenue stream.

Relying on just one source of income, ike transaction fees, is risky in a competitive market. A diversified model protects the business from industry downturns. If interest rates fall, transaction fees might stay high. At the same time, if trading volume drops, lending margins might pick up the slack, ensuring a stable bottom line.

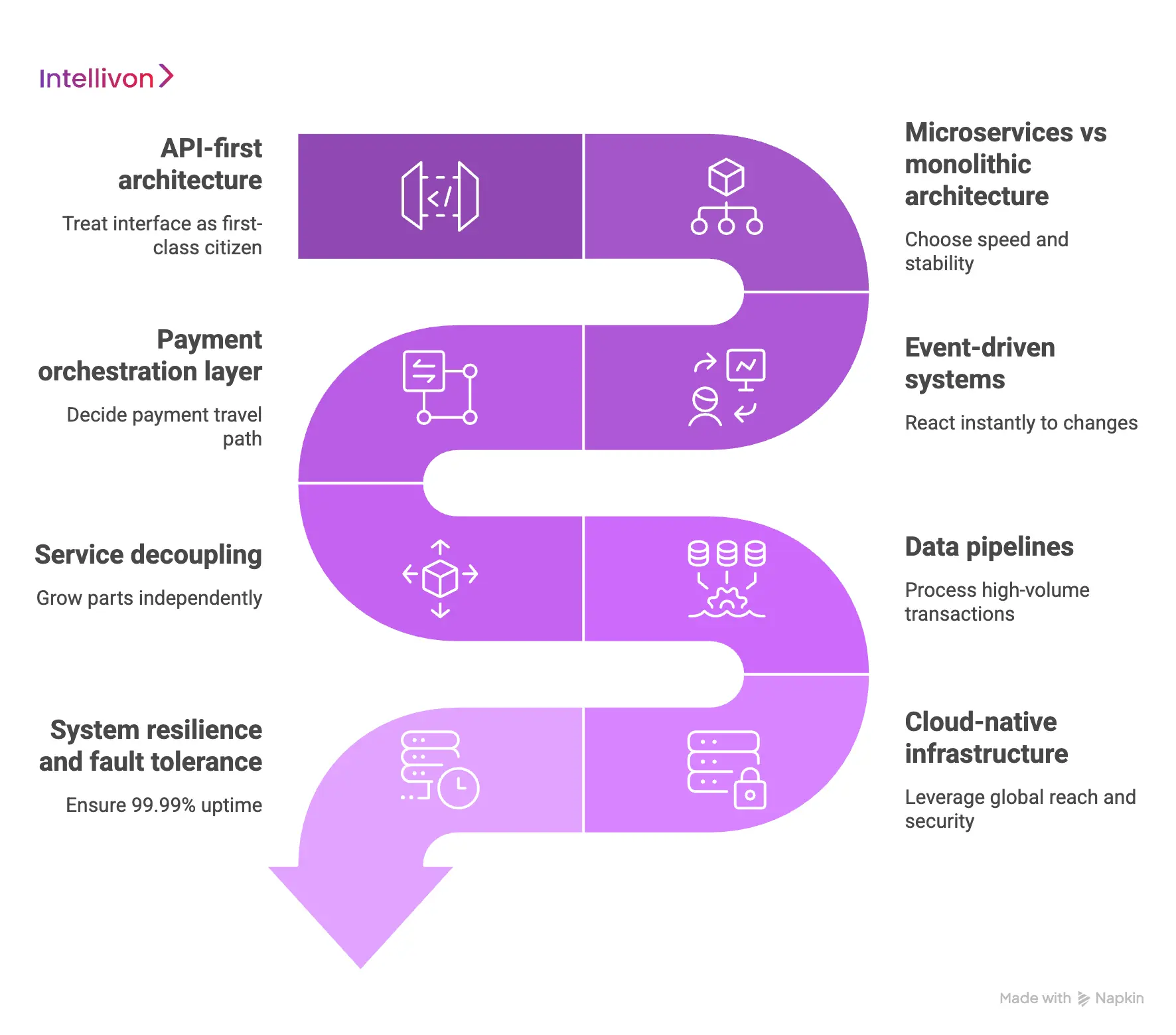

How To Architect a B2B Payments Platform Like SoFi?

Building a global payments engine is an exercise in engineering precision. The goal is to create a system that is robust enough to handle billions in capital yet flexible enough to integrate with legacy banking systems and modern fintech APIs.

1. API-first architecture for maximum flexibility

An API-first approach treats the interface as a first-class citizen. Instead of building a UI and then figuring out the data flow, you build the core functionality as a set of programmable services.

This allows your enterprise clients to plug your payment rails directly into their own ERP systems or internal software, making your platform an invisible but essential part of their business.

2. Microservices vs monolithic architecture trade-offs

Large-scale platforms must choose between speed and stability.

- Monoliths: Easier to deploy initially, but become “spaghetti code” that slows down innovation as the platform grows.

- Microservices: Breaking the platform into independent services (e.g., identity, ledger, FX). While more complex to manage, this setup ensures that a bug in the rewards module won’t crash the core payment processing engine.

3. Event-driven systems for real-time payment flows

In a payments environment, every action is an event. Using an event-driven architecture (often powered by tools like Kafka) allows the system to react instantly to changes.

When a payment is initiated, the system triggers a chain reaction: check balance, verify identity, log transaction, and send notification, all happening in parallel rather than waiting in a slow, linear queue.

4. Payment orchestration layer design

Orchestration is the “brain” that decides how a payment should travel. If one banking partner is down or a specific route is too expensive, the orchestration layer automatically reroutes the transaction through the most efficient path.

This intelligence ensures high success rates for cross-border transfers and optimizes costs for the platform operator.

5. Service decoupling for horizontal scalability

Decoupling ensures that different parts of your system can grow independently. If your platform sees a massive spike in login attempts but very few actual transfers, you can scale your “Identity Service” without wasting resources on scaling the “Payment Execution Service.”

This efficiency is vital for maintaining high performance during peak market volatility.

6. Data pipelines for high-volume transaction processing

A global platform generates massive amounts of telemetry. You need robust data pipelines to move information from the live transaction database to analytical engines.

- Ingestion: Capturing every click and cent moved.

- Processing: Cleaning and normalizing data for reporting.

- Storage: Keeping records in high-availability “hot” storage for users and “cold” storage for long-term compliance audits.

7. Cloud-native infrastructure strategies

Modern platforms live in the cloud to leverage global reach and security. By using containerization (like Docker and Kubernetes), your team can deploy updates across multiple regions instantly.

This ensures that a user in London experiences the same low latency as a user in New York, which is critical for real-time B2B operations.

8. System resilience and fault tolerance design

Failure is inevitable in global networking, so the architecture must be “self-healing.” This involves implementing circuit breakers that stop a failing service from overwhelming the rest of the system.

By building with a “zero-trust” and “high-availability” mindset, you ensure that the platform remains operational 99.99% of the time, even during regional internet outages or cloud provider hiccups.

A well-architected platform is a competitive advantage. It allows you to move faster than traditional banks while providing the rock-solid reliability that enterprise CFOs demand.

Which Payment Rails Does a Global Platform Like SoFi Need?

The right mix of payment rails determines the speed, cost, and reliability of your service. A benchmark platform like SoFi optimizes them to provide the most efficient path for every dollar moved.

1. Payment rails selection and integration strategy

Choosing the right rails is a balance between reach and speed. You must decide whether to integrate directly with central banks or use “aggregator” APIs to access multiple regions at once.

A successful strategy involves building a modular “connector” layer. This allows you to add or swap regional payment methods without rewriting your core transaction logic as you expand into new markets.

2. ACH, SEPA, SWIFT, RTP, and UPI support

To serve a global enterprise, your platform must speak the local language of money.

- Domestic Speed: Supporting ACH (USA) and SEPA (Europe) for standard transfers.

- Global Standard: Integrating SWIFT for high-value, secure international wires.

- Instant Rails: Leveraging RTP (Real-Time Payments) and UPI (India) to offer 24/7 settlement.

- Future Proofing: Preparing for CBDCs (Central Bank Digital Currencies) as they become mainstream.

3. FX conversion engines and dynamic pricing

Cross-border payments are often expensive due to hidden currency markups. An enterprise-grade platform integrates with multiple liquidity providers to offer mid-market rates.

By implementing a dynamic pricing engine, you can provide “guaranteed” FX rates for a short window, giving businesses certainty on exactly how much the recipient will receive.

4. Intelligent payment routing and cost optimization

Not every payment needs to travel the same path. Intelligent routing acts like a GPS for money. If a client needs to send funds to London, the system evaluates if it’s cheaper to use a local SEPA transfer from a regional balance or a traditional SWIFT wire.

This logic reduces “middleman” fees and ensures the fastest possible delivery for the client.

5. Settlement and clearing workflow design

Moving money involves two distinct steps: clearing (the agreement to move) and settlement (the actual transfer of value). Your workflow must manage these states in real-time.

- Authorization: Confirming the sender has the funds.

- Clearing: Exchanging the transaction details between banks.

- Settlement: Updating the final ledgers to reflect the completed movement.

6. Cross-border compliance rule handling

Every border has a digital gatekeeper. Your platform must automatically apply “Sanctions Screening” and “Travel Rule” compliance based on the origin and destination.

By embedding these rules directly into the payment rail layer, you prevent transactions from being “frozen” in transit, which is a major pain point for global CFOs.

7. Latency optimization in global payment flows

In the world of high-frequency commerce, milliseconds matter. Optimizing latency involves placing your payment servers close to the banking gateways.

Using edge computing and optimized API calls ensures that when a user hits “send,” the message reaches the clearing house instantly, reducing the window for market volatility or timeout errors.

By mastering these rails, you move from being a simple app to a foundational piece of global infrastructure. This connectivity allows your users to treat the world as a single, borderless market for their capital.

Building Compliance Into Global Payments Platforms Like SoFi?

In the world of global finance, compliance is the ultimate gatekeeper. For an enterprise-grade platform, regulatory adherence rests in building a fortress that protects your investors, your clients, and your reputation.

Platforms like SoFi don’t treat compliance as a manual hurdle. Instead, it embeds these requirements directly into the code, making the legal safeguards a seamless part of the user experience.

1. KYC and KYB onboarding workflow design

Onboarding is the first test of a platform’s integrity. While Know Your Customer (KYC) is standard for individuals, Know Your Business (KYB) is the critical layer for B2B platforms.

This involves verifying corporate structures, ultimate beneficial owners (UBOs), and legal registrations. A well-designed workflow automates these checks using third-party data feeds, allowing a legitimate business to go from “signup” to “first transaction” in minutes rather than days.

2. AML transaction monitoring systems

Anti-Money Laundering (AML) is an ongoing process, not a one-time check. The system must scan every transaction for red flags, such as structuring (breaking large sums into small ones) or sudden transfers to high-risk jurisdictions.

By using machine learning, the platform can distinguish between a high-growth startup’s legitimate scaling and suspicious, non-linear activity, reducing the “false positives” that frustrate honest users.

3. Regulatory reporting infrastructure

Maintaining a license requires constant communication with authorities. A robust platform includes an automated reporting engine that generates Suspicious Activity Reports (SARs) and Currency Transaction Reports (CTRs).

This infrastructure ensures that data is formatted correctly for different regulators (like FinCEN in the US or FCA in the UK) without requiring a massive team of manual auditors.

4. GDPR, PCI-DSS, and PSD2 compliance layers

Global operations require a “compliance stack” that handles multiple data and security standards simultaneously.

- GDPR: Ensuring data privacy and the “right to be forgotten” for European users.

- PCI-DSS: Maintaining the highest security standards for handling credit card data.

- PSD2: Implementing Strong Customer Authentication (SCA) and open banking protocols to give users more control over their financial data.

5. Region-specific compliance challenges

Every market has its own “local flavor” of regulation.

A global platform must be modular enough to apply these specific rules only where they are needed, avoiding a “one-size-fits-all” approach that could slow down operations in less-regulated regions.

6. Licensing strategy vs BaaS decisions

One of the biggest strategic choices for an entrepreneur is whether to get their own banking licenses or use Banking-as-a-Service (BaaS).

- Own License: Offers more control and better margins but requires years of legal work and massive capital reserves.

- BaaS Partnership: Allows for a faster market launch by “renting” the license of an existing bank, though it means sharing revenue and following the partner bank’s risk appetite.

7. Risk management and financial audit systems

Trust is built on transparency. The platform must maintain an immutable ledger where every movement of funds is recorded and cannot be altered.

This “audit trail” is essential for internal risk management and external audits. It allows the platform to prove its solvency and operational integrity to investors and regulators at any given moment.

By turning legal complexity into a streamlined digital process, the platform becomes a trusted infrastructure for global trade. This level of rigor is what separates a simple fintech app from a global benchmark.

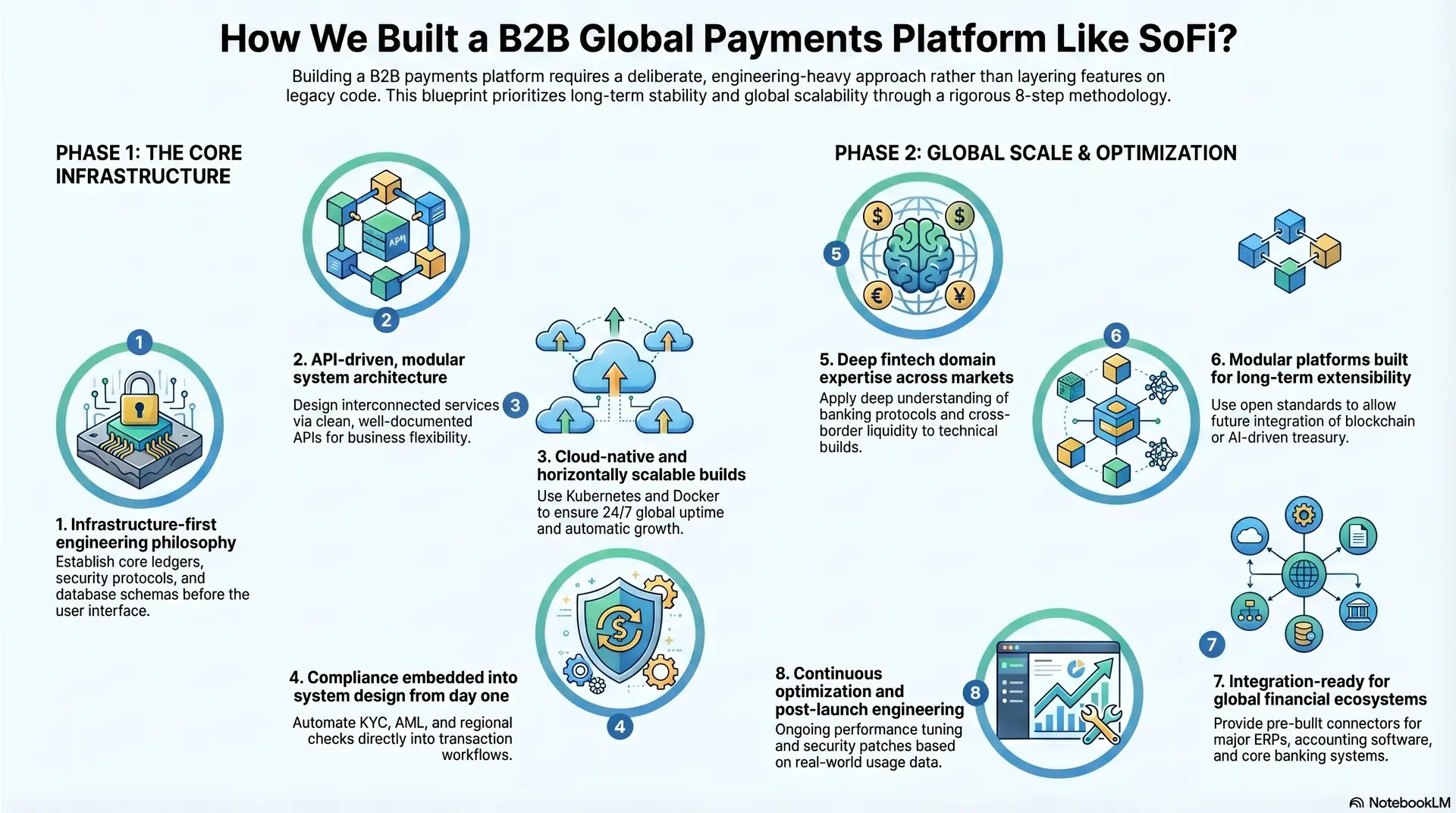

How We Built a B2B Global Payments Platform Like SoFi?

To build a platform that rivals global benchmarks like SoFi, you cannot simply layer features on top of legacy code. Success requires a deliberate, engineering-heavy approach that prioritizes long-term stability over short-term shortcuts.

At Intellivon, we follow a rigorous blueprint to ensure every platform we build is ready for the complexities of global finance.

1. Infrastructure-first engineering philosophy

We begin by focusing on the “plumbing” of the system. Before building the user interface, we establish the core ledgers, security protocols, and database schemas. This philosophy ensures that the system can handle high-volume transaction loads without latency.

By prioritizing the backend first, we create a rock-solid environment where money moves reliably, and data remains immutable.

2. API-driven, modular system architecture

We design our platforms as a series of interconnected services rather than one giant program. Every function, from currency exchange to user authentication, is accessible via a clean, well-documented API.

This modularity allows your business to pivot quickly. If you need to change your FX provider or add a new payment rail, you can do so by updating a single module without touching the rest of the system.

3. Cloud-native and horizontally scalable builds

Global platforms must stay online 24/7 across every time zone. We build using cloud-native technologies like Kubernetes and Docker to ensure “horizontal scalability.”

This means that as your user base grows from a few hundred to several million, the platform automatically adds more computing power to meet the demand. This ensures a consistent, fast experience for every user, regardless of their location.

4. Compliance embedded into system design from day one

Compliance is never an afterthought at Intellivon. We integrate KYC, AML, and regional regulatory checks directly into the transaction workflows. By automating these “gatekeeper” functions, we reduce the manual burden on your legal teams.

This “compliance-as-code” approach ensures that every movement of capital is tracked, verified, and reported according to global financial standards.

5. Deep fintech domain expertise across markets

Building a payments platform requires more than just coding skills; it requires an understanding of how money moves globally. Our team brings deep expertise in banking protocols, settlement cycles, and cross-border liquidity.

We navigate the technical nuances of different financial markets so that your platform can offer a seamless experience, no matter where the client is.

6. Modular platforms built for long-term extensibility

The financial landscape changes rapidly, and your platform must be ready to evolve. We build with “extensibility” in mind, using open standards that allow for easy integration of future technologies like blockchain or AI-driven treasury management.

This ensures that the investment you make today continues to deliver value five or ten years down the line.

7. Integration-ready for global financial ecosystems

A platform is only useful if it fits into the client’s existing world. We ensure our builds are “integration-ready” for major ERPs, accounting software, and core banking systems.

By providing pre-built connectors and flexible middleware, we make it easy for enterprise clients to adopt your solution without overhauling their entire internal technology stack.

8. Continuous optimization and post-launch engineering

Launch is just the beginning of the journey. We provide ongoing engineering support to optimize performance based on real-world usage data.

From fine-tuning database queries to updating security patches, we ensure the platform stays at the cutting edge. This commitment to continuous improvement is why leaders choose Intellivon to bring their fintech visions to life.

Building a B2B global payments platform is a transformative move that turns financial complexity into a competitive advantage. To execute a vision of this scale, you need a partner who understands both the high-level strategy and the deep technical requirements of enterprise finance.

How Do B2B Payments Platforms Manage Risk?

A leading platform manages risk by treating every data point as a signal. By analyzing these signals in real-time, the system can differentiate between a sudden pivot in a client’s business model and an actual security threat.

1. Real-time fraud detection pipelines

The window for stopping a fraudulent transaction is measured in milliseconds. Modern risk engines use high-speed pipelines to scan outgoing payments against known blacklists and suspicious patterns.

This process must happen “in-line” with the transaction flow, ensuring that protection does not create a lag that frustrates legitimate users.

2. Transaction-based risk scoring models

Every payment is assigned a numerical risk score based on its attributes.

- Destination: Is the money going to a high-risk jurisdiction?

- Amount: Does the sum exceed the historical average for this specific user?

- Frequency: Are there multiple rapid-fire transfers to the same recipient?

- Velocity: Is the capital moving faster than the typical business cycle allows?

3. Behavioral analytics for anomaly detection

Static rules are easy for criminals to bypass, so the system learns “normal” behavior. By tracking how a business leader typically interacts with the platform, such as their login times, device signatures, and typical transfer windows, the system creates a behavioral baseline. Any sharp deviation triggers a verification request, such as a biometric check or a call from an account manager.

4. AI-driven underwriting and decisioning systems

Risk management extends into the lending side of the platform. AI-driven models ingest thousands of variables, from cash-flow health to industry trends, to provide instant credit decisions.

This allows the platform to offer “Just-in-Time” financing to low-risk businesses while automatically tightening credit limits for those showing signs of financial distress.

5. Monitoring transaction patterns at enterprise scale

Managing risk for thousands of corporations requires a “macro” view of the network. The system monitors for systemic risks, such as a sudden downturn in a specific sector to which many clients belong.

This enterprise-scale visibility allows the platform to adjust its overall risk appetite and reserve capital more effectively during market volatility.

6. Automated alerts and risk response workflows

When a threat is detected, the system shouldn’t just send an email; it should act.

- Temporary Hold: Automatically pausing a suspicious transfer.

- Notification: Alerting the CFO via an urgent push notification.

- Resolution: Providing a clear path to verify the transaction or report a breach.

- Escalation: Moving high-value disputes to a specialized human risk team for immediate review.

7. Data storage and analytics infrastructure design

To fight modern fraud, you need historical data. A robust infrastructure stores years of transaction telemetry in a way that is easily searchable for forensic analysis.

This data lake is used to reconstruct events after a breach or to provide evidence during a regulatory audit, ensuring the platform remains transparent and accountable.

By mastering these risk layers, a platform creates an environment of total stability. For a business leader, this means knowing that their capital is not just being moved, but is being actively guarded by a sophisticated, always-on intelligence system.

Integrating B2B Global Payments Platform Into Existing Systems

Successful integration ensures that data flows without friction. When your payment rails are deeply connected to the enterprise’s existing software stack, you reduce manual overhead and eliminate the “data gaps” that lead to costly accounting errors.

1. Core banking system integration patterns

For platforms that act as an extension of traditional banks, the integration must be rock-solid. This often involves using ISO 20022 messaging standards to ensure that data sent from the platform is perfectly understood by the bank’s legacy ledger.

By using “bridge” adapters, the platform can translate modern JSON-based API calls into the formats required by older banking cores, ensuring compatibility without compromising on speed.

2. ERP and accounting platform connectivity

Enterprise Resource Planning (ERP) systems like SAP, Oracle, or NetSuite are the source of truth for most businesses.

- Direct Sync: Automatically pushing transaction data into the general ledger.

- Reconciliation: Matching bank statements with internal invoices in real-time.

- AP/AR Automation: Triggering payments directly from the ERP’s accounts payable module.

3. Payment gateway and fintech API connections

No platform is an island. You must integrate with existing gateways (like Stripe or Adyen) and niche fintech APIs for specialized tasks like tax calculation or identity verification.

A modular “adapter” pattern allows you to plug in these third-party services quickly, ensuring your clients have access to the best tools in the market through a single interface.

4. Partner and third-party ecosystem integrations

A platform grows in value when it opens its doors to partners. By allowing third-party developers to build “apps” on top of your payment rails, such as custom reporting tools or industry-specific payroll modules, you create a rich ecosystem.

This makes your platform stickier, as businesses can customize their financial stack without leaving your environment.

5. API versioning and lifecycle management

In an enterprise setting, you cannot “break” an integration with a sudden update. Strict API versioning ensures that while you roll out new features, older integrations continue to function perfectly.

- Semantic Versioning: Clearly labeling updates (e.g., v1.1 vs v2.0).

- Deprecation Policies: Giving developers years, not months, to migrate to newer versions.

- Backward Compatibility: Ensuring that core payment flows remain untouched during upgrades.

6. Middleware and integration layer design

Middleware acts as the translator between your platform and the client’s messy internal systems. By building a dedicated integration layer, you can handle data mapping and transformation outside of your core processing engine.

This keeps your main system clean and fast while allowing for the high level of customization that large-scale enterprise clients often demand.

7. Real-time data synchronization across enterprise systems

In global trade, “stale” data is a risk. If a payment is made in London, the CFO in New York should see the updated balance in their ERP instantly.

Implementing webhooks and “push” notifications ensures that every connected system is updated the moment a transaction status changes, providing a “single version of truth” across the entire organization.

Integration is the bridge between a good product and an essential one. By making the platform easy to adopt and impossible to outgrow, you position it as the permanent foundation of a client’s global financial strategy.

How Do B2B Global Payments Platforms Make Money?

Profitability in this space comes from high-volume, low-friction interactions. By diversifying income across transaction fees, software subscriptions, and financial spreads, the platform remains stable despite shifts in the global economy.

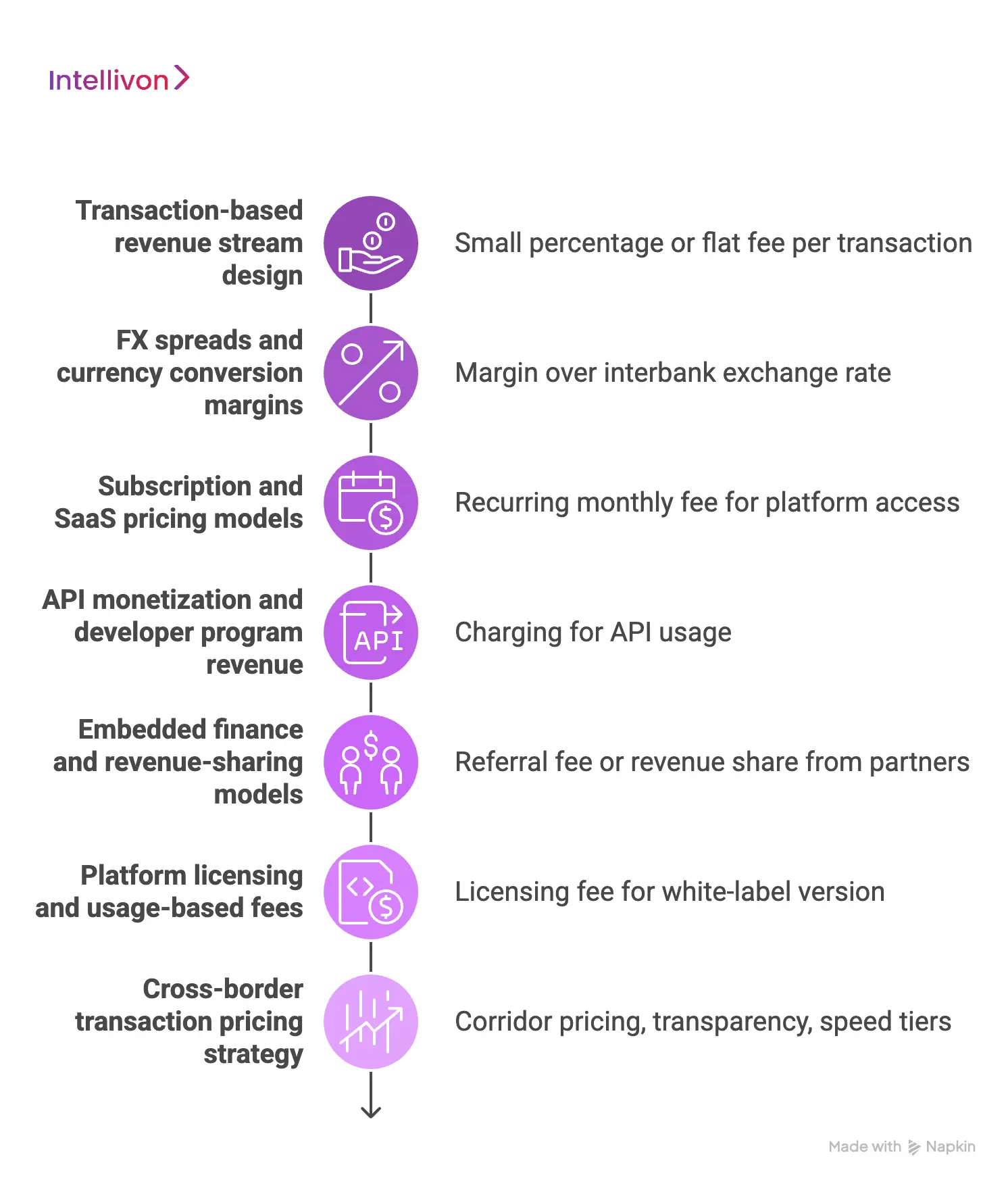

1. Transaction-based revenue stream design

The most direct way to generate income is by taking a small percentage or a flat fee from every transaction. For B2B platforms, this usually involves tiered pricing where the fee per transaction decreases as the client’s volume increases.

This “volume-for-margin” trade-off encourages enterprises to route all their global capital through your system rather than splitting it among competitors.

2. FX spreads and currency conversion margins

Cross-border payments offer a significant revenue opportunity through Foreign Exchange (FX) spreads. When a business sends money in USD, and the recipient receives it in EUR, the platform applies a small margin over the “interbank” or mid-market exchange rate.

While this margin is often lower than traditional bank rates to attract users, the sheer scale of enterprise transfers makes this a highly lucrative stream.

3. Subscription and SaaS pricing models

To ensure a predictable monthly income, platforms often charge a recurring SaaS fee.

- Access Fees: Charging for the use of the dashboard and reporting tools.

- User Seats: Billing based on the number of employees with platform access.

- Premium Modules: Adding costs for advanced features like automated tax filing or deep ERP integrations.

4. API monetization and developer program revenue

If your platform is used as a foundation for other companies to build their own products, you can monetize the API itself. This might involve charging “per-call” or offering developer tiers.

This turns your technical infrastructure into a product, allowing you to earn from the innovation of other fintechs who use your payment rails to power their own apps.

5. Embedded finance and revenue-sharing models

Embedded finance allows you to offer third-party products, like insurance or specialized lending, directly within your interface. You earn a referral fee or a percentage of the revenue generated by these partners.

This “marketplace” model adds value to the user without requiring you to build every specialized financial tool from scratch.

6. Platform licensing and usage-based fees

For massive global corporations, you might offer a “white-label” version of your platform. In this scenario, the enterprise pays a significant licensing fee to use your technology under its own brand.

Alternatively, usage-based fees can be applied to specific high-value activities, such as real-time compliance checks or instant liquidity triggers.

7. Cross-border transaction pricing strategy

Pricing for international payments must be strategic to remain competitive globally.

- Corridor Pricing: Adjusting fees based on the difficulty of the route (e.g., USD to GBP is cheaper than USD to VND).

- Transparency: Providing a clear breakdown of “all-in” costs to build trust with CFOs.

- Speed Tiers: Charging a premium for “instant” delivery while offering lower rates for standard 2-day settlements.

Tiered pricing structures for enterprise clients

Large-scale clients require custom contracts that reflect their unique needs. A tiered structure allows the platform to grow with the client. A startup might start on a “Pay-as-you-go” plan, while a global conglomerate moves to a custom enterprise tier with negotiated flat rates and dedicated support.

This flexibility ensures that the platform is accessible to small businesses while remaining profitable for the largest players in the market.

A smart revenue model aligns the platform’s success with the client’s growth. When the pricing is fair and transparent, the platform ceases to be a cost center and becomes a strategic partner that facilitates global expansion.

What Does It Cost to Build a Global Payments Platform?

Building a global payments platform is not a fixed-cost project. The total investment depends on how deeply your system integrates with payment rails, banking infrastructure, compliance layers, and enterprise workflows.

Unlike simple payment apps, these platforms operate as core financial infrastructure. As a result, costs are shaped more by architecture, integrations, and scalability requirements than just feature count.

In most cases, a well-scoped global payments platform typically falls between $50,000 and $150,000, depending on complexity and rollout strategy.

Key Cost Drivers in Enterprise Builds

Several factors influence how your budget scales.

- Geographic coverage across multiple regions

- Payment rail integrations (SWIFT, SEPA, ACH, RTP, UPI)

- Transaction volume and real-time processing needs

- Compliance requirements (KYC, AML, reporting)

- Integration depth with ERP, banking, and APIs

The more global and real-time your system is, the higher the investment.

Cost Breakdown by Modules and Complexity

| Component | Scope | Estimated Cost |

| Core Platform & UI | Admin panel, dashboards, workflows | $8,000 – $15,000 |

| Payment Engine | Transactions, routing, orchestration | $10,000 – $25,000 |

| Ledger System | Wallets, reconciliation, accounting | $8,000 – $20,000 |

| Payment Integrations | SWIFT, SEPA, ACH, RTP, UPI | $10,000 – $30,000 |

| Compliance Systems | KYC, AML, reporting | $8,000 – $20,000 |

| API & Integrations | ERP, banking, third-party APIs | $5,000 – $15,000 |

| Security Systems | Encryption, IAM, fraud detection | $5,000 – $12,000 |

| Analytics & Monitoring | Reporting, alerts, dashboards | $3,000 – $8,000 |

Estimated Total Cost:

$50,000 – $150,000

Infrastructure and Maintenance Costs

Beyond development, ongoing costs are critical.

- Cloud infrastructure (AWS, GCP, Azure) scales with usage

- Monitoring, logging, and observability tools

- Third-party API and payment provider fees

- Compliance audits and regulatory updates

- Security maintenance and system upgrades

Enterprise platforms require continuous investment to remain stable and compliant.

Timeline vs Cost Trade-Off

Your timeline directly impacts your budget.

- 3–5 months (MVP): Core features, lower cost

- 6–9 months (mid-scale): Balanced functionality and integrations

- 9+ months (advanced): Higher scalability and compliance depth

Faster timelines increase cost due to larger teams and parallel development.

Strategic Insight

The real cost of a global payments platform is building a system that can scale, stay compliant, and process transactions reliably across regions.

If you’re planning a platform inspired by SoFi, the smartest investment is in architecture and scalability from day one, not just initial build cost.

Conclusion

Building a global payments platform is a strategic investment in future growth. It transforms financial friction into a powerful competitive advantage. Success requires more than just moving capital. It demands a secure, integrated, and highly scalable ecosystem.

When you own the infrastructure, you control the entire client journey. This foundation allows for rapid expansion and long-term market leadership. The right architecture makes global commerce simple, fast, and remarkably efficient.

Build Your Global Payments Platform With Intellivon

Building a global payments platform rests on creating a scalable financial infrastructure that can handle real-time flows, multi-region compliance, and enterprise integrations from day one.

At Intellivon, we don’t approach this as a feature development project. We build platforms as end-to-end financial systems, designed to support high-volume transactions, cross-border payments, and evolving regulatory requirements.

Our engineering approach combines API-first architecture, cloud-native infrastructure, and modular system design. This ensures seamless integration with payment rails, core banking systems, ERPs, and third-party fintech services, without disrupting your existing operations.

Why Build With Intellivon

- Infrastructure-First Approach: We build platforms that function as financial backbones, not short-term payment solutions.

- Designed for Real Payment Workflows: Every system is structured around real-world transaction flows, reconciliation, and settlement processes.

- API-Driven and Integration-Ready: Easily connect with banking systems, payment networks, and enterprise software ecosystems.

- Compliance Built Into the Core: KYC, AML, and regulatory frameworks are embedded into the architecture from the start.

- Scalable for Global Operations: Handle multi-currency transactions, cross-border payments, and high-volume processing without performance bottlenecks.

Build With Confidence

If you’re looking to build a platform inspired by SoFi but tailored for B2B global payments at scale, the right foundation makes all the difference.

Talk to Intellivon’s experts to get a quote and platform roadmap built around your business goals.

FAQs

Q1. What Payment Rails Does a B2B Global Payments Platform Need?

A1. A B2B global payments platform needs ACH for domestic US batch transfers, SWIFT for international wires, SEPA for euro-zone transactions, RTP, and FedNow for real-time settlement. No single rail covers every market, so the platform must support multi-rail routing that selects the fastest and cheapest path per transaction.

Q2. Should I Build or Use BaaS for a Payments Platform?

A2. Build when you need proprietary control over compliance, FX pricing, or ledger logic, typically at $1M+ transaction volumes where unit economics justify infrastructure ownership. Use BaaS when speed to market matters more than margin optimization, or when your team lacks payments domain depth.

Q3. How Long Does It Take to Build a Payments Platform?

A3. A B2B global payments platform MVP covering core rails, a multi-currency ledger, and KYC onboarding takes 6 to 9 months with a focused team. A production-grade platform with multi-rail support, FX engines, AML monitoring, ERP integrations, and multi-region deployment typically requires 12 to 24 months.

Q4. What Compliance Does a Global Payments Platform Need?

A4. A4.A global B2B payments platform must address KYB/KYC for business onboarding, AML transaction monitoring, PCI-DSS for card data security, PSD2 for European open banking, and GDPR for data privacy in the EU.