Key Takeaways:

-

AI automates SAR evidence gathering, investigation summarization, and narrative drafting but never filing decisions.

-

RAG pipelines, FinCEN narrative controls, hallucination safeguards, and reviewer approval are core production requirements.

-

Transaction monitoring integration, case management access, and audit trails ensure regulator-ready documentation throughout.

-

Enterprise AI SAR platforms cost $60,000 to $250,000 with annual maintenance at 18 to 25%.

-

How Intellivon builds SAR generation systems around source-grounded evidence, compliance officer control, and regulator-ready documentation.

Every SAR your team files starts with a compliance officer manually drafting a narrative that meets FinCEN’s who-what-when-where-why standard. It takes hours, and when the caseload scales, the backlog compounds over time. AI SAR generation changes that by using LLMs to draft those narratives from investigation data in minutes, shifting your team’s role from authoring to reviewing.

What determines whether this automation holds up to regulatory scrutiny, however, is not the model, but instead, the access to evidence. Without a RAG pipeline grounding the LLM to verified case data, the model invents details that create direct filing liability. However, with the right architecture, every sentence traces to verified case evidence. Consequently, banks that get this right reduce per-SAR drafting time by up to 70% and double SAR throughput within 12 months, thereby rebuilding the examiner trust and institutional credibility that backlogs erode.

Intellivon has built compliance automation for financial institutions using an evidence-grounded RAG methodology. This blog covers that specific approach here and gives you a full picture of the system from scratch.

What Is a Suspicious Activity Report and Why Is It Needed?

A Suspicious Activity Report, or SAR, is a confidential regulatory report that financial institutions file when they detect activity that may involve money laundering, fraud, terrorist financing, sanctions exposure, cybercrime, or other financial crime risk. SARs help regulators and law enforcement understand suspicious behavior patterns, connect investigations, and act on financial intelligence.

Under the Bank Secrecy Act and BSA-AML reporting requirements, banks must document any transaction that lacks a clear legal purpose. However, a SAR is simply a record of suspicious behavior, and it is never official proof of a crime. Because of this distinction, banks must keep these filings strictly confidential to protect both the investigation and customer privacy.

When an institution detects a threat, the FFIEC SAR guidance outlines strict filing timelines that the compliance team must follow. Managing these strict timelines requires strong operational discipline:

- The 30-Day Window: The team must file within a mandatory 30-day SAR filing requirement once they identify a specific suspect.

- The 60-Day Extension: If the suspect remains unknown, the bank can use a 60-day SAR extension requirement to gather more transaction data.

- Continuation Filings: If the illicit behavior continues over time, the bank must submit a SAR continuation filing every 90 days.

Poorly written narratives often create severe audit risks during an OCC SAR examination standards review. For this reason, the text must explain the suspicious activity clearly so federal investigators can understand the transaction pattern.

The following table highlights these core regulatory rules and explains how automated software must handle them.

Core Regulatory Rules

| SAR Requirement | What It Means for Banks | Why AI Must Handle It Carefully |

| Suspicious activity detection | The bank identifies activity that may require reporting. | AI must not decide suspicion alone. |

| Narrative explanation | The SAR explains the who, what, when, where, why, and how. | AI must generate source-backed language. |

| Filing deadline | Reports must follow a strict 30-day or 60-day timeline. | AI must track clocks and queue urgency. |

| Confidentiality | SARs cannot be disclosed to the reported party. | AI needs access controls and audit logs. |

| Continuing activity | Ongoing bad behavior needs a follow-up filing every 90 days. | AI must link related cases and prior SARs. |

| Supporting evidence | The bank must preserve all underlying documentation. | AI must map claims to source records. |

Ultimately, SARs are not just simple bureaucratic forms. They are vital pieces of regulatory intelligence that must be accurate, timely, confidential, and backed by clear evidence. To meet these high standards consistently without burning out compliance teams, banks are now turning to specialized enterprise technology.

For a deeper breakdown of how modern institutions scale their compliance infrastructure, see our guide on AI AML compliance copilot development. This infrastructure provides the foundation for automated software to draft complex narratives safely.

What Is an AI Suspicious Activity Report Generation Platform?

An AI suspicious activity report generation platform is a controlled compliance system that turns AML case evidence into reviewable SAR drafts. It retrieves transaction data, KYC records, investigator notes, typology signals, sanctions results, adverse media, and prior case history. Then it drafts a source-grounded narrative for human review, approval, and filing preparation.

This enterprise software goes far beyond simple text generation. Specifically, a true AI SAR narrative generation platform acts as an operational hub that unifies evidence retrieval, automated drafting, and compliance tracking. Consequently, it supports the entire compliance hierarchy by providing dedicated tools for frontline analysts, quality assurance reviewers, and senior managers.

Importantly, this generative AI SAR drafting software never makes autonomous filing decisions. Instead, the core architecture enforces a strict human-in-the-loop SAR review protocol to ensure absolute accuracy before final submission.

The following table outlines how these core components orchestrate the data lifecycle safely.

Core Components of Data Lifecycle

| Platform Component | What It Does |

| Alert ingestion | Pulls suspicious activity cases from monitoring tools. |

| Evidence retrieval | Collects transactions, KYC, notes, and risk signals. |

| RAG pipeline | Coordinates data via RAG case management integration. |

| SAR narrative generator | Drafts the report in a regulator-ready structure. |

| Quality scoring layer | Powers SAR quality review automation to check completeness. |

| Reviewer dashboard | Allows analysts to apply mandatory compliance officer SAR approval. |

| Filing workflow layer | Powers SAR filing workflow automation and tracking. |

| Audit trail | Creates immutable SAR documentation by logging all edits. |

Therefore, the platform’s real value comes from connecting disparate evidence, regulatory language, human review, and strict filing control into a single, cohesive workflow. This end-to-end integration ensures that no critical piece of evidence is left out.

For a practical look at how these data pipelines connect to core banking systems, see our comprehensive guide on how banks develop an AI AML compliance copilot platform. This engineering framework explains the foundations of secure data ingestion.

Why SAR Automation Is Becoming a Banking Priority

SAR automation is becoming a priority because AML teams face rising alert volumes, tighter review expectations, faster digital transactions, complex typologies, and pressure to control compliance costs. The market is moving from basic workflow automation toward AI-assisted investigation, evidence retrieval, narrative drafting, and quality control.

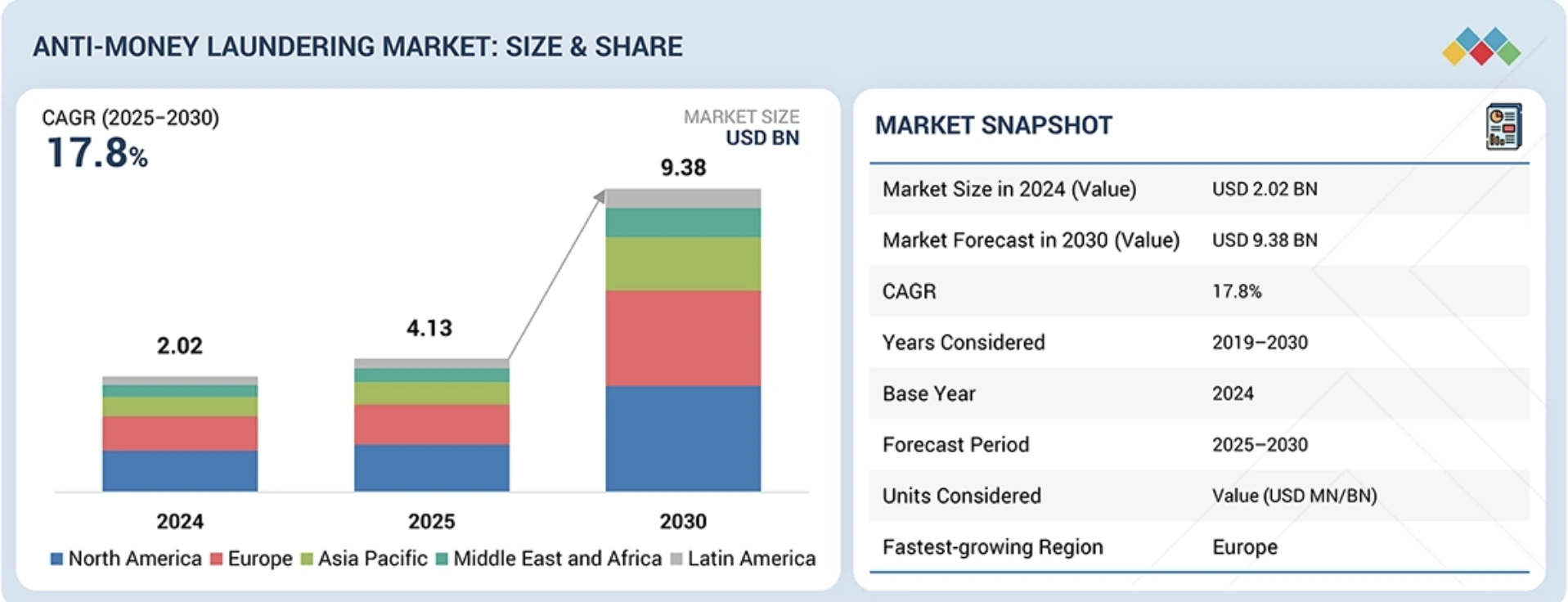

Driven by these severe operational realities, financial institutions are actively modernizing their core financial crime infrastructure. According to a MarketsandMarkets anti-money laundering market study, the global anti-money laundering market size is projected to grow from roughly $4.13 billion in 2025 to $9.38 billion by 2030, representing a Compound Annual Growth Rate (CAGR) of 17.8%. This sustained capital influx reflects a fundamental shift across retail banking and fintech sectors toward specialized automated software.

Rising Workload Pressures

- Elevated Transaction Velocity: The explosive growth of instant digital payments creates an overwhelming stream of automated system alerts.

- Analyst Fatigue: Manual SAR drafting automation consumes skilled investigator hours, converting highly analytical staff into administrative data entry clerks.

- Backlog Risks: Strict FinCEN filing deadlines mean operational backlogs create immediate regulatory examination liabilities for compliance departments.

Evolving Operational Demands

- Intricate Financial Typologies: Modern money laundering methods like crypto-layering, mule networks, and cyber fraud require linking data across siloed platforms.

- Stricter Supervisory Review: Regulators demand that every submitted narrative displays clear, objective evidence, an explicit audit trail, and zero arbitrary assumptions.

- Commercial Vendor Options: Automated SAR tools now appear across major industry platforms like DataRobot, Hawk, Hummingbird, DataWalk, SEON, and NICE Actimize.

Consequently, modern market demand is not simply focused on minor speed improvements. Instead, institutions require explainable, secure financial crime infrastructure that connects data evidence directly to generated prose.

For a comprehensive evaluation of how custom platforms handle these sophisticated operational demands, see our technical analysis of enterprise AML AI copilot platform features. This blueprint outlines the critical modules needed to ensure absolute system defensibility.

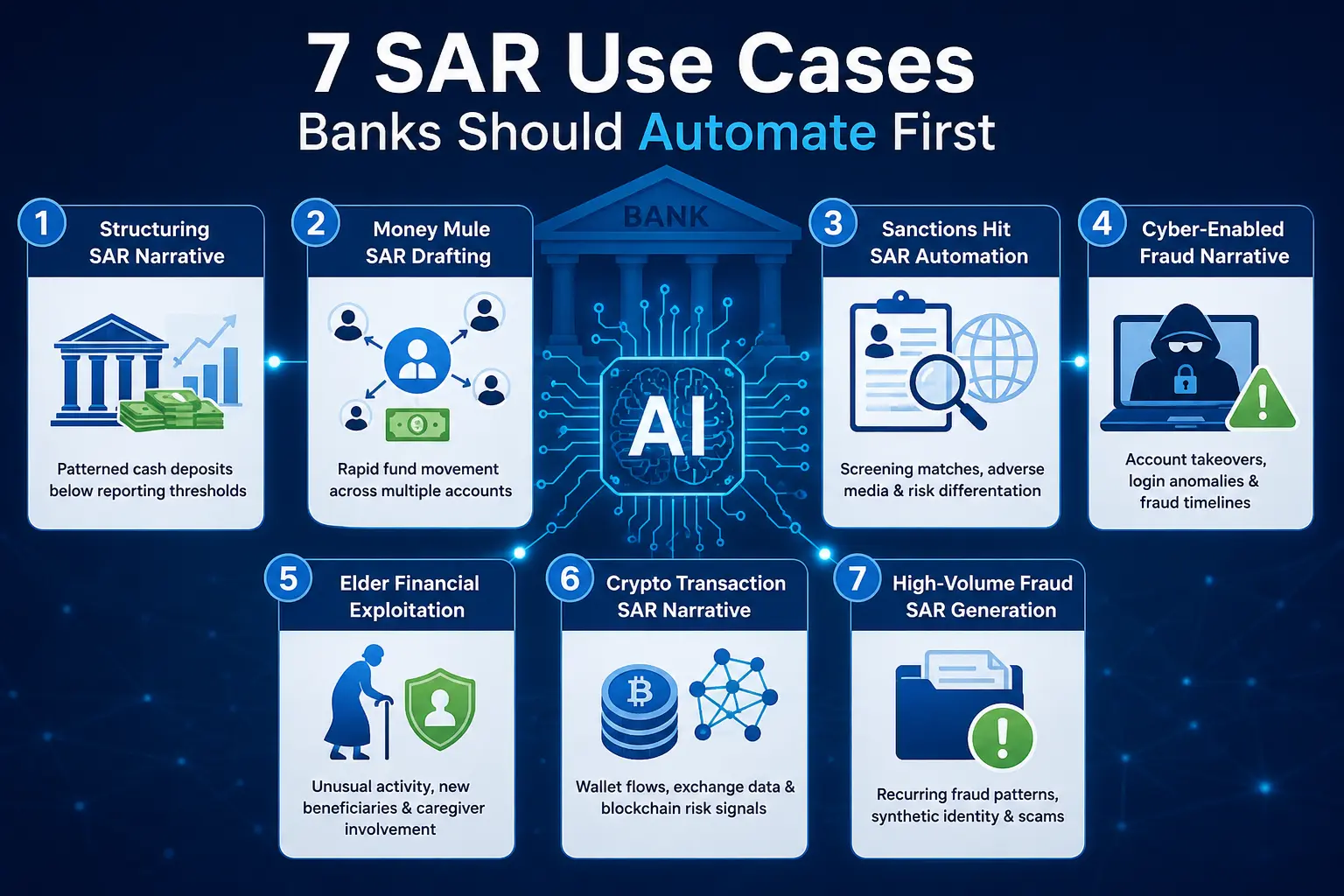

Which SAR Use Cases Should Banks Automate First?

Banks should automate SAR use cases where evidence is structured, reviewer rules are clear, and narrative patterns repeat across high-volume investigations. The best starting points are structuring, money mule activity, sanctions hits, cyber-enabled fraud, elder financial exploitation, crypto transaction activity, and high-volume fraud cases that already follow defined escalation workflows.

1. Structuring SAR Narrative Automation

Structuring is one of the strongest early use cases because the evidence usually includes clear transaction dates, cash amounts, account numbers, branch locations, and threshold-related patterns. AI can convert those records into a chronological SAR draft while avoiding unsupported claims about criminal intent.

Consequently, manual report drafting becomes highly redundant when dealing with fixed mathematical cash limits. Because of this predictability, an automated engine can map out exact physical transaction schedules without losing factual accuracy.

- Algorithmic Ledger Sorting: The platform extracts raw cash deposits and teller timestamps across multiple physical banking hubs simultaneously.

- Contextual Behavioral Profiling: The engine instantly pulls the customer’s historical KYC data to establish their typical cash-handling baseline.

- Chronological Narrative Assembly: As a direct result, the software writes a complete, structured timeline that highlights sequential deposits made just under the critical $10,000 threshold.

For a comprehensive evaluation of how custom platforms handle these sophisticated operational demands, see our technical analysis of enterprise AML AI copilot platform features. This blueprint outlines the critical modules needed to ensure absolute system defensibility.

2. Money Mule SAR Drafting

Money mule cases are strong candidates for AI SAR drafting because they often involve repeatable patterns: rapid inbound transfers, quick withdrawals, unrelated counterparties, device overlaps, new accounts, and unusual payment velocity. AI can organize these signals into a draft that helps analysts validate the flow of funds.

Consequently, compliance teams often struggle to trace these rapid fund movements across disjointed, separate accounts manually. Therefore, using software to instantly connect device footprints and moving funds removes massive investigative friction.

- Transactional Velocity Calculation: The software aggregates incoming peer-to-peer transfers and calculates the exact velocity of immediate, outgoing cash outflows.

- Digital Footprint Correlation: The platform extracts linked hardware identifiers, sharing IP addresses, and cookie data across newly registered profiles.

- Counterparty Mapping: Consequently, the tool automatically constructs a clean data map showing how funds pass through unrelated third-party beneficiaries.

3. Sanctions Hit SAR Automation

Sanctions-related SAR workflows need careful automation because false matches, partial name matches, geography, counterparty identity, and OFAC exposure can change the risk picture quickly. AI should help assemble evidence and draft a factual summary, but reviewers must confirm match quality before escalation or filing.

Because of the high volume of false alarms in filtering systems, analysts spend hours checking simple typos or shared names. As a result, the platform focuses on organizing factual data points rather than making high-risk legal declarations.

- Sourcing Global Watchlists: The platform retrieves official screening scores, match categories, and primary country origin details from internal monitoring files.

- Collating Adverse Media: The tool collects related international news entries, corporate ownership registries, and customer profile attachments.

- Differentiating Risk Signals: Thus, it drafts a highly objective report that clearly separates confirmed evidence from unverified identity matches.

4. Cyber-Enabled Fraud SAR Narrative

Cyber-enabled fraud is a strong AI SAR use case because the evidence often sits across fraud systems, device logs, login records, IP data, customer complaints, and transaction trails. AI can rebuild the event timeline faster than manual drafting while keeping investigators focused on final judgment.

Consequently, combining raw technical network logs with retail transaction data takes up too much human operational time. Therefore, an automated system can ingest these technical tables and translate them into a readable chronological summary.

- Ingesting Security Logs: The system pulls brute-force login attempts, strange device swaps, and confirmed account takeover indicators.

- Tracking Funds Trajectories: The platform maps sudden changes in external banking beneficiaries alongside rapid wire transfer executions.

- Synthesizing Customer Reports: Then, it drafts a cohesive timeline by linking real-time customer support chat transcripts with system alerts.

5. Elder Financial Exploitation SAR Drafting

Elder financial exploitation needs careful AI support because the narrative must stay factual, sensitive, and evidence-backed. AI can compare customer age indicators, account history, withdrawal changes, new beneficiaries, unusual wires, call notes, and branch observations without making unsupported claims about coercion or abuse.

Because these cases require extreme empathy and absolute legal precision, the draft must avoid any emotional speculation. Instead, the software systematically highlights sharp variances against long-standing behavioral baselines.

- Auditing Spending Deviations: The platform analyzes historical transaction histories to highlight sudden, high-value check cashings or unusual power-of-attorney changes.

- Extracting Interaction Notes: The program processes unstructured input fields from branch teller windows and telephonic support queues.

- Enforcing Compliance Safeguards: Furthermore, it isolates sensitive information and screens out subjective descriptions before generating the draft.

6. Crypto Transaction SAR Narrative

Crypto SAR narratives are useful for digital asset platforms, fintechs, and banks with virtual asset exposure because blockchain evidence is difficult to summarize manually. AI can combine wallet activity, transaction hops, exchange data, customer profiles, sanctions exposure, and blockchain analytics into a reviewable narrative.

Consequently, translating public blockchain hashes into a standard corporate report is incredibly slow for traditional compliance staff. Therefore, the automation engine bridges the gap between public ledgers and banking records.

- De-anonymizing Ledger Hops: The engine groups related crypto wallet clusters and calculates risk scores from known illicit addresses.

- Consolidating Exchange Records: The platform pulls standard KYC profiles, fiat deposit paths, and off-ramp transaction details.

- Formatting Plain Explanations: As a result, it explains complex digital asset movements in simple terms for traditional bank reviewers.

7. High-Volume Fraud SAR Generation

High-Volume fraud cases are practical early candidates because banks often see repeated patterns across account takeover, check fraud, card fraud, wire fraud, synthetic identity, and payment scams. AI can reduce repetitive drafting by converting structured investigation records into consistent, reviewer-ready SAR narratives.

Because of the massive volume of identical fraud alerts, compliance departments quickly experience operational bottlenecks. Therefore, automating these standard templates frees up valuable staff for complex cases.

- Consolidating Alert Packages: The program groups incoming card fraud alerts, check copy scans, and direct customer dispute letters.

- Extracting Identity Signals: The engine checks for synthetic identity red flags by auditing credit bureau hits and profile anomalies.

- Populating Typology Templates: Then, it generates a complete draft using pre-approved organizational structures and direct investigator input notes.

Ultimately, the safest first use case is not always the most technologically advanced option. Banks should always start where data quality, clear review rules, and daily filing volumes create immediate, measurable efficiency gains.

How AI Suspicious Activity Report Generation Works

AI suspicious activity report generation works by converting case evidence into a structured, reviewable SAR draft. The system collects transaction data, customer details, counterparty records, investigation notes, typology signals, and prior case history. Then it uses an LLM or agentic workflow to draft a narrative that a compliance officer verifies, edits, approves, and files.

Consequently, this automated layout moves raw transactional patterns into highly structured legal text. This clear transition simplifies life for human analysts.

1. The Automated Intake Pipeline

- Alert Verification: The platform ingests active anomalous alerts from underlying core monitoring systems.

- Case Evidence Compilation: The engine quickly gathers transaction histories, historical KYC documentation, and internal analyst files.

- Investigation Summary Generation: Then, the platform writes a comprehensive financial background summary for further internal analysis.

2. Standardized Drafting and Review

- Suspicious Activity Description Generation: The system shapes text block data using explicit FinCEN SAR narrative structure requirements.

- Transaction Pattern Narrative Construction: The software describes multi-layered account hops using verified numerical facts. (Source: [FFIEC BSA/AML SAR Quality Guidance])

- SAR Filing Workflow Automation: Finally, the tool pushes the completed draft directly into a human review queue.

Therefore, implementing this exact methodology results in high-quality SAR drafting automation across your compliance infrastructure. As a direct result, senior managers maintain total administrative visibility over the final reporting step.

For a detailed look at how to hook these text systems up to underlying transaction ledgers, see our engineering guide on how to build an AI transaction monitoring platform today.

What FinCEN Expects From SAR Narratives

FinCEN expects SAR narratives to explain who conducted suspicious activity, what happened, when it happened, where it occurred, why it appears suspicious, and how the activity was carried out.

AI SAR narrative generation must therefore produce evidence-backed language, not polished summaries. At the same time, accuracy, completeness, timeliness, confidentiality, and reviewer accountability remain mandatory.

1. The Core 5W+H Architecture

FinCEN requires every submitted narrative to answer six fundamental investigative questions systematically. Consequently, the language engine must parse unstructured documentation to extract these key data points without introducing outside assumptions.

- Who and What: The text must clearly isolate the primary account holders and describe the exact transaction types observed.

- When and Where: The system must organize specific execution dates alongside physical branch locations or digital routing points.

- Why and How: The narrative must detail why the pattern deviates from typical behavior and how the funds moved across institutions.

2. Managing Regulatory Timelines and Extensions

Compliance operations must adhere to strict statutory clocks to maintain regulatory compliance. Therefore, the automation platform must track transaction dates and flag potential filing delays within the analyst dashboard.

- Initial Filing Mandate: The bank must file the report within a strict 30-day SAR filing requirement once a suspect is identified.

- Suspect Unknown Extension: If the suspect remains unidentified, the platform can trigger a 60-day SAR extension requirement window.

- Continuing Activity Rules: For ongoing illicit behavior, the system must organize a recurring SAR continuation filing timeline every 90 days.

3. Narrative Quality Control and Amendments

Maintaining high-quality submissions requires continuous validation of historical reports. Because of this, the underlying software must handle complex modification workflows when new financial intelligence comes to light.

- Fulfilling Completeness Expectations: The system automatically checks the report against strict SAR completeness requirements to avoid missing fields.

- Correction Management: Analysts can initiate a structured SAR amendment workflow to update historical filings safely.

- Automated Quality Checks: The platform runs background verification scripts to power comprehensive SAR quality control automation.

4. What the AI Must Never Guess

The AI must never invent suspects, relationships, motives, transaction intent, missing dates, account ownership, counterparty links, or typology conclusions. Every generated claim must map to source evidence. If evidence is missing, the system should mark the gap for reviewer attention instead of filling it with plausible language.

To protect data integrity, the system applies strict boundaries to prevent the software from generating unverified text. Consequently, this engineering approach isolates the writing phase from speculative commentary.

- Unsupported Claim Detection: The engine automatically scans generated text to flag sentences that lack direct source citations.

- Factual Database Grounding: Every statement maps directly to a verified transaction record, KYC file, or investigator note.

- Operational Confidence Scoring: The software calculates an internal reliability score and routes low-scoring drafts to senior review queues.

Once the rules are clear, the next question becomes what technical architecture can enforce them.

For an analytical breakdown of the underlying infrastructure required to handle these complex regulatory pipelines, see our operational guide on how fintech companies build AI AML investigation systems.

The SAR Evidence Ledger: The Control Layer

The SAR Evidence Ledger is a sentence-level audit layer that records which source produced each claim in the AI-generated SAR narrative. It turns SAR drafting from a black-box writing task into a controlled evidence workflow. For SAR managers, this creates a defensible review trail before the report reaches approval or filing.

Consequently, this system gives your compliance team total control over every single word. This clear mapping makes it simple to defend your filings during federal regulatory audits.

1. Verifying Customer and Transaction Claims

A compliant platform must justify every single factual claim with underlying business records. Therefore, the automation infrastructure binds your text directly to active bank databases.

- Identity Verification Tracking: Every customer profile statement links directly to verified KYC or CDD records to maintain absolute narrative accuracy.

- Transaction Pattern Validation: Every transactional description links to explicit transaction monitoring records to prove exact dates, amounts, and locations.

- Counterparty Relationship Mapping: Every counterparty claim links directly to entity resolution graphs to confirm complex network links before drafting.

2. Tracking Logic and System Modifications

System actions and human interventions must be fully trackable over time. Because of this requirement, the software records all background processes and user changes instantly.

| Narrative Claim Type | Required Evidence Source | System Control |

| Customer identity | KYC/CDD profile | Source citation required |

| Transaction pattern | Transaction monitoring records | Date, amount, counterparty validation |

| Counterparty relationship | Entity resolution graph | Link-confidence threshold |

| Suspicion rationale | Investigator notes + typology rules | Reviewer approval required |

| Filing deadline | Case detection timestamp | Filing clock automation |

| Continuing SAR reference | Prior SAR record | Related filing linkage |

| AI-generated text | Model output record | Model versioning and prompt log |

3. Maintaining Model Version Controls

Financial institutions must be able to reproduce past results to prove compliance. Consequently, our engineering framework treats language models like core infrastructure assets that need strict tracking.

- Enforcing Immutable Documentation: The system automatically locks down all case files to generate highly secure, immutable SAR documentation.

- Grounding Model Context: The generation engine references fixed, model-grounding SAR documents to prevent common language hallucinations.

- Tracking Model Versions: The infrastructure implements strict SAR generation model versioning to record the exact prompt history for every run.

Specifically, this strict data tracking provides explainable AI SAR decisions that can easily withstand intense regulatory scrutiny. As a direct result, your bank maintains complete reviewer accountability and true regulator-ready transparency across the entire operation.

Ultimately, this advanced control layer turns basic text automation into a highly defensible compliance platform. It shifts the focus from simple drafting to complete evidence chain validation.

For a deeper look at how to coordinate these agentic AI systems within your financial operations, see our complete guide on how banks use agentic AI for AML compliance automation.

Architecture Supports AI SAR Generation Automation Banking

AI SAR generation automation banking needs a governed architecture that connects transaction monitoring, KYC, case management, regulatory knowledge, evidence retrieval, narrative drafting, reviewer approval, and filing preparation. The safest systems separate evidence retrieval from language generation, then validate the draft before a compliance officer approves the final report.

Consequently, building this enterprise architecture requires deep system integration across multiple isolated financial data layers. This structural approach ensures that your language tools receive clean information.

1. Secure Ingestion and System Integration

The platform must pull data from your existing banking stack to build a complete case file. Therefore, creating a secure data pipeline is the critical first step for the platform.

- Core Banking Integration SAR: The engine connects to central ledgers to pull account balances and basic customer registration fields.

- Payment Processor SAR Integration: The platform tracks digital money movements by linking directly to real-time clearing networks and payment gateways.

- Transaction Monitoring Integration SAR: The system automatically ingests anomalies from traditional monitoring tools to begin processing files quickly.

2. Advanced Evidence Retrieval Pipelines

Gathering secondary context manually takes too much time for busy compliance departments. Because of this bottleneck, automated systems gather supplementary records instantly to support the case file.

- RAG Pipeline Investigation Documents: The platform uses retrieval-augmented generation to pull past transaction files and unstructured company files.

- Case Management System SAR Integration: The tool connects directly to your central queue via RAG case management integration protocols.

- Adverse Media SAR Integration: The system checks verified global news databases to extract contextual risk profiles for the report.

3. Multi-Rail Analysis and Screening

Modern financial crime often moves between traditional fiat currencies and digital ledgers. Consequently, the system unifies data from specialized risk tracking systems into one view.

| Layer | What It Does | Example Inputs | Required Controls |

| Alert ingestion | Receives suspicious activity cases | TM alerts, fraud alerts, sanctions hits | Timestamp and source logging |

| Evidence normalization | Structures case data | Transactions, KYC, notes, attachments | Field validation |

| Entity resolution | Links accounts and counterparties | Devices, accounts, businesses | Match confidence |

| RAG retrieval | Pulls approved evidence | Case docs, policies, prior SARs | Permission-aware retrieval |

| Typology classification | Identifies suspicious pattern | Structuring, layering, mule activity | Reviewer-visible rationale |

| Narrative generation | Drafts SAR narrative | Evidence packets | Grounded generation only |

| Quality validation | Scores draft completeness | 5W+H, missing data, contradictions | Rule-based and LLM judge checks |

| Review workflow | Routes to compliance officer | Draft, sources, edits | 4-eyes approval |

| Filing preparation | Creates form-ready data | FinCEN fields, attachments | Filing deadline checks |

| Audit record | Preserves traceability | Model version, prompt, edits | Immutable logs |

4. Infrastructure Security and Platform Trust

Financial compliance platforms handle highly confidential customer data that requires maximum infrastructure security. Therefore, our system engineering follows a strict protection strategy to maintain absolute data privacy.

- Role-Based Access Control SAR: The software restricts file access so only authorized analysts can see sensitive data fields.

- Data Encryption SAR Platform: The system encrypts all confidential financial text blocks during storage and transmission.

- Zero-Trust SAR Architecture: The technical environment validates every system user and network call to ensure continuous data safety.

Specifically, these strict security features allow the system to maintain full SOC 2 SAR platform compliance easily. As a direct result, your bank keeps its data protected while accelerating daily operations.

Ultimately, your core technical architecture decides whether AI truly speeds up your reviewers or simply creates more quality assurance work. A well-designed system keeps your data clean from start to finish.

Which AI Models Should Power SAR Narrative Generation?

LLM SAR report generation banking should use a combination of retrieval models, classification models, entity resolution models, and controlled language models. A single generic LLM is not enough. SAR automation needs models that extract facts, detect typologies, summarize evidence, draft narratives, score completeness, and flag unsupported statements.

Consequently, relying on a single general text tool will cause severe operational errors. This multi-model approach ensures each technical step balances text fluency with objective truth.

1. Extracting Unstructured Intelligence

The system must first process unorganized text blocks before generating any formal regulatory reports. Therefore, implementing dedicated natural language processing tools helps clean up messy data inputs.

- NLP Investigation Document Analysis: The software reads through long PDF attachments to pull out critical dates and locations automatically.

- Unstructured Data Extraction SAR: The engine converts informal email threads and customer chat transcripts into clean database tables.

- Machine Learning SAR Generation Fintech: The core platform identifies suspicious movement trends within digital wallets using advanced anomaly classifiers.

2. Generating Compliant Prose

Once the data is clean, the language generation layer translates the evidence into professional compliance reports. Because of this specialized task, the system uses tightly controlled environments for generative AI compliance writing.

| Model Type | Role in SAR Automation | When to Use |

| Retrieval model | Finds approved evidence. | RAG over case files and policies. |

| NLP extraction model | Pulls names, dates, amounts, and entities. | Unstructured notes and PDFs. |

| Typology classifier | Detects structuring, mule, fraud, and cyber patterns. | Large alert volumes. |

| Entity resolution model | Connects related accounts and counterparties. | Complex networks. |

| LLM draft model | Writes reviewable SAR narrative. | Evidence-grounded drafting. |

| LLM judge/validator | Scores completeness and accuracy. | QA before reviewer approval. |

| Graph analytics model | Documents network evidence. | Layering, mule, crypto, and sanctions. |

3. Should You Fine-Tune an LLM for SAR Drafting?

Fine-tuning helps when a bank has enough approved, high-quality SAR narratives, consistent labels, and clear typology coverage. However, most first releases should start with RAG, templates, guardrails, and reviewer feedback loops. Fine-tuning becomes valuable after the platform collects enough validated corrections and rejection reasons.

Consequently, rushing into full training without clean information will cause the system to copy old human mistakes. Therefore, building a solid data foundation is an absolute prerequisite.

- SAR Training Dataset Creation: The engineering team compiles historical filings into a highly secure, private training environment.

- Labeled SAR Narrative Training: The software learns from past documents that have been explicitly marked as high-quality by compliance experts.

- LLM Fine-Tuning SAR Data: The model updates its internal weights to match the exact writing style and tone of your specific bank.

Intellivon usually starts with retrieval-grounded drafting and quality scoring before fine-tuning. This avoids training the model on inconsistent historical narratives before the bank defines its current compliance standard. Specifically, we focus our MLOps SAR generation pipeline on continuous model evaluation to keep outputs completely safe.

Once the models are selected, the platform needs a workflow that keeps humans accountable. For a deeper breakdown of how to build these complex machine learning workflows, see our comprehensive guide on what features an enterprise AML AI copilot should include.

How Human Review Should Work in AI SAR Platform Development

AI SAR compliance platform development must keep compliance officers in control of filing decisions, narrative approval, amendment decisions, and continuing SAR reviews. The AI can prepare evidence, draft language, flag gaps, and suggest revisions. However, a qualified reviewer must confirm the facts, rationale, suspicion narrative, supporting documentation, and final filing readiness.

Consequently, this precise manual interface stops the system from operating as a completely unmonitored text generator. This strict boundary ensures human accountability remains intact throughout the investigation lifecycle.

1. The Automated Review Queue and Workflow

The software organizes incoming cases into structured priorities to reduce manual administrative coordination. Therefore, investigators can instantly access pre-assembled evidence folders without hunting through separate databases.

- SAR Review Queue Automation: The platform automatically prioritizes draft reports based on upcoming regulatory filing deadlines.

- SAR Review and Approval Workflow: The system routes completed narrative drafts through a multi-stage corporate validation chain.

- SAR Escalation Workflow: Complex financial crime cases automatically trigger a senior compliance management review path.

2. Validation, Rejection, and Amendments

Analysts must have clear tools to correct machine errors or update historical documents easily. Because of this requirement, the user dashboard supports granular text modifications and continuous quality tracking.

- SAR Rejection and Revision Workflow: Reviewers can instantly send a draft back to the engine with specific correction notes.

- SAR Quality Review Automation: Background validation scripts score every sentence block for absolute factual consistency before submission.

- SAR Amendment Workflow: The application coordinates necessary secondary updates when new financial evidence surfaces.

3. Enforcing Strict Operational Governance

Maintaining regulatory defensibility requires implementing rigorous structural controls across the entire software application. Consequently, the development framework enforces explicit visibility boundaries to protect highly sensitive customer data.

- Four-Eyes Approval Protocols: The system prevents the original drafting analyst from single-handedly approving the final regulatory document.

- Granular Reviewer Permissions: Role-based access keys ensure only certified compliance officers can authorize a formal submission.

- Immutable Decision Logs: Every individual user text modification, model rejection, or final approval is saved automatically.

Specifically, this rigorous human-in-the-loop SAR review interface guarantees that an expert always evaluates the suspicious rationale. As a direct result, your financial institution eliminates the legal exposure of ungrounded automated text generation.

Ultimately, this review design completely prevents the dangerous operational risk where the AI wrote it and a human simply clicked approve without checking the facts. It ensures your compliance officers remain fully empowered decision-makers.

For a deeper breakdown of the transactional rules and data signals that fuel these manual queues, see our complete deployment guide on how to build an AI transaction monitoring platform today.

How to Measure SAR Narrative Accuracy Before Filing

SAR narrative accuracy should be measured through evidence coverage, factual consistency, 5W+H completeness, typology alignment, contradiction checks, reviewer edits, rejection rates, and filing error rates.

ROUGE scores alone are not enough because a SAR can sound fluent while missing material facts or overstating unsupported relationships.

Consequently, relying only on language style can mask dangerous text errors. This structured verification ensures that all generated paragraphs remain legally defensible.

1. Building an Objective Quality System

An enterprise compliance framework requires precise metrics to track text reliability systematically. Therefore, engineers deploy multi-layered validation tests to score drafts before human review begins.

- SAR Narrative Evaluation Metrics: The system automatically calculates precise data coverage scores across every generated sentence block.

- Fulfilling SAR Completeness Requirements: The software audits the text to ensure no regulatory data categories are left blank.

- SAR Filing Error Rate Reduction: Tracking common reporting mistakes helps compliance teams lower their monthly correction filings significantly.

2. Mitigating Generative Language Risks

Using open-ended text tools introduces specific technical vulnerabilities that can compromise confidential filing systems. Because of this risk, the underlying platform implements rigid LLM guardrails and SAR generation barriers.

| Evaluation Metric | What It Measures | Target Standard |

| Evidence coverage | Whether all key evidence appears | 95%+ source-backed material facts |

| Unsupported claim rate | Claims without source evidence | 0% for final filing draft |

| 5W+H completeness | Who, what, when, where, why, how | All required fields present |

| Typology alignment | Correct suspicious activity category | Reviewer-approved category |

| Contradiction score | Conflicts across records | No unresolved contradictions |

| Reviewer edit rate | Manual rewrite burden | Declines across pilot cycles |

| Rejection rate | QA or manager rejected drafts | Tracked by reason code |

| Filing error rate | Form or data issues | Reduced month over month |

3. Why ROUGE Is Not Enough for SAR Quality

ROUGE can compare generated text against reference narratives, but it cannot prove that a SAR draft is accurate, complete, or source-grounded. SAR quality needs claim-level evidence checks, regulatory field validation, typology review, and human approval. Therefore, ROUGE should support evaluation, not define production readiness.

Consequently, using simple phrase matching can trick analysts into accepting highly polished report hallucinations. Therefore, true SAR quality scoring must focus on data lineage rather than poetic writing styles.

- Automated LLM-as-Judge Validation: The platform runs a secondary evaluation model to check the primary draft for hidden contradictions.

- Rule-Based Completeness Tests: Scripted data checks confirm that all critical transaction amounts match core banking ledgers.

- Granular Source Verification: The system visually highlights the exact evidence path for every statement inside the user dashboard.

After quality evaluation, the buyer needs to understand what the system must integrate with.

What Systems Must Integrate With Automated SAR Filing?

Automated SAR filing software development requires integration with transaction monitoring, core banking, KYC, KYB, CRM, case management, sanctions screening, adverse media, blockchain analytics, document repositories, identity tools, and BSA filing workflows. The system’s value depends on how well it retrieves evidence without forcing analysts to leave their investigation workspace.

Consequently, missing hooks into your primary operational architecture will render any text generator completely useless. This data unification ensures that the drafting application can capture every relevant signal across the bank’s digital footprint.

1. Core Ledger and Identity Sourcing

The platform must constantly extract basic customer context and asset histories to fulfill essential regulatory reporting fields. Therefore, engineers establish secure data pipelines directly into your central systems of record.

- Transaction Data Extraction SAR: The pipeline pulls complete account histories, specific currency values, routing numbers, and exact processing execution timestamps automatically.

- Customer Account Data SAR: The infrastructure maps active user profiles to collect legal addresses, Taxpayer Identification Numbers (TINs), and verified employer classifications.

- Core Banking Integration SAR: The system binds text generation elements directly to underlying core ledgers to verify current asset ownership fields before drafting begins.

2. Managing Extended Entity Networks

Modern financial crime investigations require tracking complex business networks and third-party interactions. Because of this structural reality, your implementation must gather secondary institutional and counterparty details simultaneously.

- Counterparty Data Extraction: The platform isolates the names, banks, and account numbers of all external individuals receiving or sending funds.

- Payment Processor SAR Integration: Software connectors monitor high-velocity digital clearinghouses, card networks, and localized merchant nodes to catch immediate money movement patterns.

- Case Management System SAR Integration: The automation software syncs directly with central internal queues to preserve past analyst notes and file attachments.

3. Special Screening and Regulatory Delivery

Submitting reports requires pulling high-risk data hits and transforming them into precise, agency-approved formats. Consequently, our backend development hooks into critical screening software to satisfy complex BSA-AML reporting requirements.

| Integration | Why It Matters | Example Data |

| Transaction monitoring | Alert source | Rules, risk scores, alert history |

| Core banking | Account truth | Balances, account ownership, transfers |

| KYC/KYB | Customer context | Identity, business profile, expected activity |

| Case management | Investigation record | Notes, attachments, dispositions |

| Sanctions/PEP tools | Exposure evidence | Hits, match scores, screening records |

| Adverse media | External intelligence | News, risk articles, source URLs |

| Blockchain analytics | Crypto evidence | Wallet clusters, exposure, typologies |

| CRM/support | Customer explanations | Tickets, emails, call notes |

| Filing workflow | Submission preparation | FinCEN fields, deadlines, status |

Ultimately, these core system integrations determine whether your final generated narrative remains legally defensible under regulatory review. Seamless data pipelines ensure the engine never has to guess a critical fact.

Which Suspicious Activity Types Can AI Draft SARs For?

AI SAR narrative generation platforms can support common typologies such as structuring, layering, money mule activity, fraud, elder exploitation, cyber-enabled crime, terrorist financing, human trafficking indicators, drug trafficking patterns, sanctions exposure, crypto laundering, and unusual business activity. Each typology needs different evidence fields, language patterns, and reviewer checks.

Consequently, using a one-size-fits-all text layout will cause severe compliance gaps across your specialized investigative divisions. Building unique, rule-grounded pipelines ensures each distinct crime pattern receives accurate contextual framing.

1. Tracing Basic Fiat and Placement Schemes

Traditional banking placement methods require pulling highly structured cash ledgers and instant clearing data fields. Therefore, the automation layer focuses on calculating exact transaction schedules to match explicit regulatory archetypes.

- Structuring Narrative Automation: The tool groups consecutive cash movements occurring within tight windows to flag conscious threshold evasion.

- Layering Narrative Generation: The software tracks rapid internal account hops and complex corporate shell movements across multiple banking jurisdictions.

- Money Mule Narrative Automation: The system maps swift inbound digital peer-to-peer transfers followed immediately by cash out-of-network ATM withdrawals.

2. Documenting Fraud and Vulnerable Exploitation

Investigating fraud patterns requires connecting digital hardware identifiers, customer support interactions, and sensitive demographic data points. Because of this complexity, the text generation layer applies rigid vocabulary boundaries to preserve objective framing.

- Fraud Narrative Generation: The platform organizes structured alerts involving check alteration, identity theft, or confirmed account takeover indicators.

- Cyber-Enabled Crime SAR Narrative: The engine processes failed brute-force logins and sudden device swaps alongside transactional paths.

- Elder Financial Exploitation SAR Builders: The application flags sharp deviations against multi-year baseline spending habits without introducing subjective emotional speculation.

3. Isolating Sanctions and Emerging Networks

High-risk network investigations rely on cross-referencing global security watchlists, public distributed ledgers, and international regulatory mandates. Consequently, the platform matches incoming hits to verified background evidence payloads before drafting begins.

| Typology | Evidence AI Must Retrieve | Narrative Risk |

| Structuring | Cash deposits below thresholds | Overstating intent |

| Layering | Rapid movement across accounts | Missing entity links |

| Money mule activity | Incoming/outgoing velocity | Mislabeling victims |

| Elder exploitation | Customer age, unusual transfers | Sensitive language risk |

| Cyber fraud | Device, IP, login, transfer data | Weak causal claims |

| Human trafficking | Pattern indicators and locations | Unsupported conclusions |

| Terrorist financing | Watchlist and transfer patterns | High-risk escalation |

| Crypto laundering | Wallet activity and chain exposure | Poor blockchain interpretation |

| Sanctions exposure | Match data and OFAC context | False match risk |

Ultimately, engineering typology-specific design logic improves both your underlying narrative accuracy and your internal reviewer trust. Ensuring each script maps to exact data fields eliminates common drafting hallucinations.

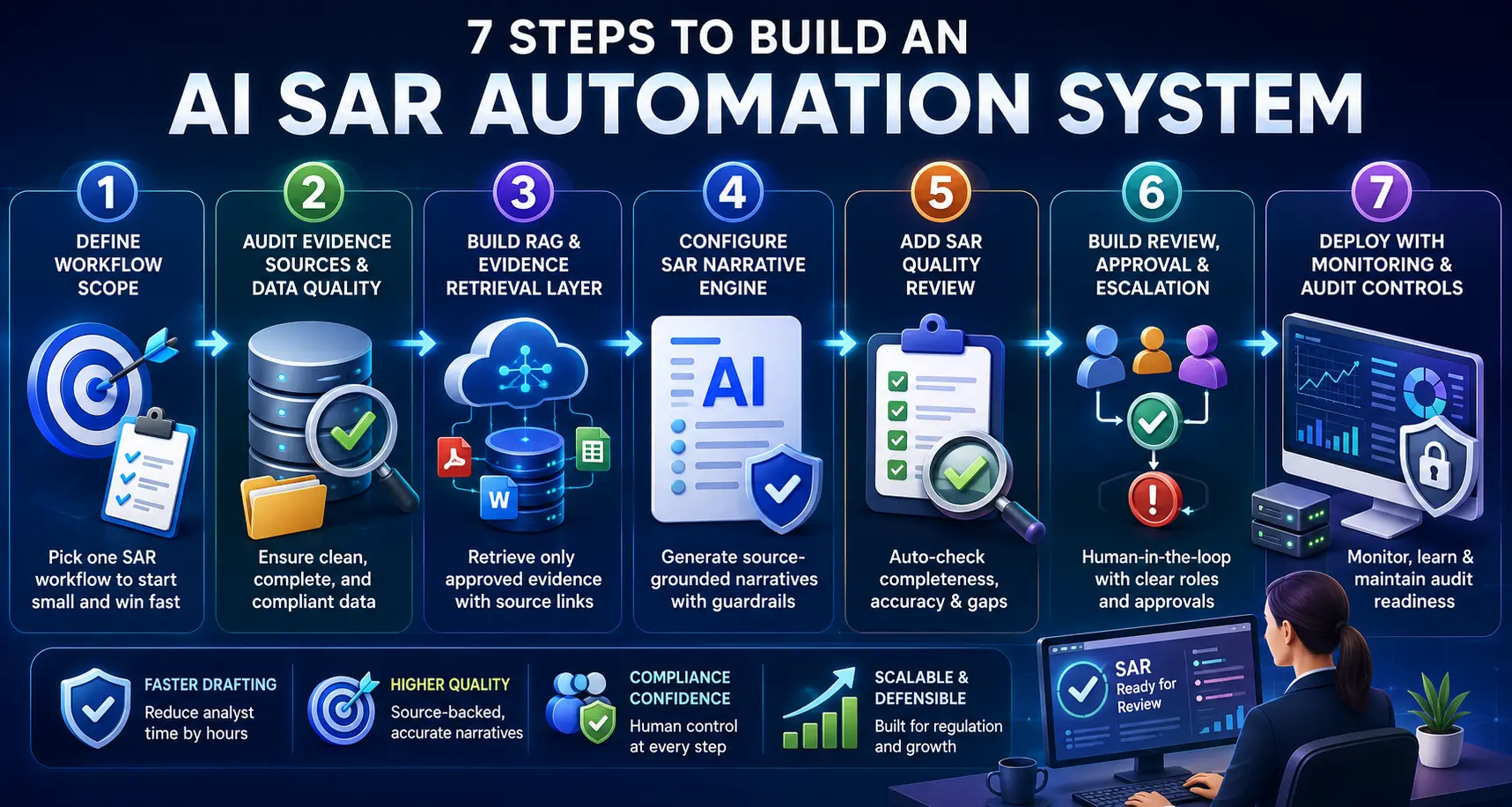

How to Build AI SAR Automation System Step by Step

To build AI SAR automation system capabilities safely, enterprises should start with one controlled SAR workflow, connect approved evidence sources, design retrieval architecture, configure narrative templates, add validation, test reviewer workflows, and deploy gradually. The goal is not full autonomy. The goal is faster, source-grounded drafting under compliance officer control.

Consequently, attempting a complete, multi-department launch on day one will overwhelm your engineering team. Focusing on an incremental rollout ensures that text pipelines remain strictly grounded in reality.

Step 1 — Define the SAR Workflow Scope

The first step is to define which SAR workflow the platform will automate first. A focused MVP may support fraud SAR narratives, structuring cases, sanctions-related SAR support, or crypto transaction narratives. This scope determines integrations, evidence fields, reviewer permissions, deadlines, cost, and QA controls.

Because different financial crimes require entirely separate regulatory information fields, starting too broad causes system drift. Therefore, isolating a single alert queue allows your developers to map data structures perfectly.

- Select One Primary Target Queue: Choose a high-volume, highly predictable alert group like simple structuring to launch the prototype.

- Define Clear Machine Triggers: Document exactly which system alert parameters should signal the engine to begin a draft.

- Establish Baseline Reporting Deadlines: Map out your specific institutional filing windows to keep the automation timeline on track.

Intellivon starts by mapping the live SAR workflow, not a generic compliance diagram. This helps define which tasks AI can perform and which actions must stay with SAR managers.

Step 2 — Audit Evidence Sources and Data Quality

The second step is to audit whether the required SAR evidence exists in usable form. AI cannot produce accurate SAR drafts from incomplete case data, inconsistent transaction fields, missing KYC records, or weak investigation notes. The audit should confirm source ownership, field quality, permissions, retention rules, and update frequency.

Consequently, feeding fragmented, dirty text strings into a language model will guarantee broken summaries. Therefore, ensuring total data hygiene across your central ledgers is an absolute prerequisite.

- Standardize Transaction Database Fields: Confirm all incoming transaction histories contain clean timestamps, branch IDs, and currency values.

- Verify Identity Document Completeness: Check that your customer profiles contain full legal names, addresses, and tax identifiers.

- Establish Clear Data Lineage Paths: Trace every piece of evidence back to its primary host system to fulfill regulatory safety audits.

Intellivon evaluates source systems before model selection. This prevents teams from buying or building an LLM layer before the evidence foundation can support regulated drafting.

Step 3 — Build the RAG and Evidence Retrieval Layer

The third step is to build a permission-aware RAG layer that retrieves only approved evidence for each SAR case. This layer should pull investigation documents, transaction histories, KYC files, policies, prior related cases, and reviewer notes. It must preserve source references so the narrative can prove every material claim.

Because language engines have tight memory limits, pulling irrelevant system records will quickly dilute the model’s focus. As a result, using smart data indexing keeps the generation process highly targeted.

- Deploy Hybrid Vector Database Search: Combine traditional keyword matching with deep semantic vector search to surface contextual background files.

- Apply Metadata Access Restrictions: Enforce strict permission tags so the retrieval engine never views unauthorized user data.

- Compile Structured Evidence Packets: Group all extracted transaction rows and identity logs into a clean, unedited payload file.

Intellivon designs RAG workflows with source permissions, document versions, and retrieval histories preserved. This makes generated narratives reviewable instead of merely readable.

Step 4 — Configure the SAR Narrative Generation Engine

The fourth step is to configure the LLM to draft SAR narratives from structured evidence packets, not open-ended prompts. The generation engine should follow approved narrative templates, FinCEN 5W+H expectations, typology-specific language, reviewer instructions, and institution-specific formatting rules while avoiding unsupported conclusions.

To satisfy federal reviewers, the model must follow rigorous text layouts instead of writing freely. Therefore, your engineers must constrain the engine using fixed structural prompt definitions.

- Build Rigid Generation Templates: Construct precise text prompts that force the model to present dates and methods in a standard sequence.

- Enforce Typology Vocabulary Constraints: Inject specific financial crime terms based on the active case type while banning emotional phrases.

- Apply Character and Word Cap Limits: Hardcode maximum length targets into the API call to avoid verbose, repetitive paragraphs.

Intellivon treats the LLM as a controlled drafting component inside a larger workflow. The model receives approved evidence, defined instructions, and validation checks before reviewers see the output.

Step 5 — Add SAR Quality Review Automation

The fifth step is to add automated QA before human review. The system should check whether the SAR draft includes required fields, source-backed claims, correct chronology, relevant suspicious activity indicators, typology alignment, reviewer notes, and filing deadline status. This prevents reviewers from becoming the first quality control layer.

Consequently, forcing human compliance teams to manually proofread basic structural errors wastes massive operational time. Therefore, deploying a mechanized background checker ensures every report meets baseline standards before eyes ever touch it.

- Execute 5W+H Completeness Sweeps: Run automated scripts to guarantee the drafted text contains clear who, what, and why fields.

- Run Real-Time Contradiction Scans: Compare dates and dollar values inside the text draft directly against raw database tables.

- Calculate a Ready-for-Filing Score: Assign an objective reliability index to each report to isolate weak summaries automatically.

Intellivon builds QA scorecards that show reviewers what the AI included, what it skipped, and which claims need closer inspection. This reduces blind trust in polished drafts.

Step 6 — Build Reviewer, Approval, and Escalation Workflows

The sixth step is to build role-based review workflows where analysts, QA reviewers, SAR managers, and compliance officers perform defined actions. The platform should support edit tracking, rejection reasons, second-line review, escalation, continuing SAR reminders, amendment workflows, and final approval before filing.

Because filing a regulatory report carries immense legal weight, your interface must clearly define who holds signature authority. As a result, the application must isolate basic drafting tasks from final submission approval.

- Enforce a Mandatory Four-Eyes Rule: Block any solo analyst from writing and submitting a report without a separate manager review.

- Log Explicit Form Rejection Reasons: Save every user-entered correction note into a central database to track system changes.

- Automate Continuing Filing Reminders: Track active cases over time and auto-schedule secondary summaries on active regulatory loops.

Intellivon configures reviewer authority around the institution’s compliance policy. The AI can recommend, prepare, and draft, but the platform clearly records who approved each filing-ready version.

Step 7 — Deploy With MLOps, Monitoring, and Audit Controls

The final step is to deploy the system with model monitoring, prompt versioning, drift checks, reviewer feedback loops, access logs, evidence retention, and audit-ready reporting. SAR generation quality must be tracked after release because typologies, regulations, case quality, and reviewer expectations change over time.

Because federal examiner standards shift constantly, software performance must be measured continuously post-launch. Consequently, setting up production logs is vital to catch drop-offs in draft accuracy early.

- Monitor Writing Style Drift Continuously: Run regular background comparisons to ensure the model’s vocabulary matches your baseline rules.

- Track Granular Prompt Version Codes: Store the exact version number of your system prompts alongside every generated report file.

- Maintain Immutable Access Logs: Record every database query and user touchpoint to ensure complete regulatory compliance.

Intellivon designs production SAR automation as a monitored compliance system. This helps teams prove what changed, why outputs changed, and how reviewers controlled final filings.

With the build path clear, readers need absolute cost clarity before kicking off a project. For a transparent breakdown of the budgets and engineering resources needed to deploy this infrastructure, see our market evaluation on what it costs to build an AI AML compliance copilot.

This cost overview details how to manage your development capital efficiently.

How Much Does AI SAR Automation Development Cost?

Enterprise AI SAR platforms cost $60,000 to $250,000 with annual maintenance at 18 to 25%. AI SAR automation development cost usually ranges from $70,000–$140,000 for a controlled MVP and $160,000–$420,000+ for a production AI SAR narrative generation platform, depending on integrations, private deployment, RAG complexity, reviewer workflows, filing support, security controls, and model evaluation depth.

Consequently, attempting to calculate engineering budgets without analyzing backend connectivity leads to severe procurement errors. This transparent framework aligns development hours directly with specialized bank infrastructure requirements.

1. Granular Engineering Cost Breakdown

Building a defensible filing system requires distributing capital across discrete security and infrastructure layers. Therefore, organizations divide technical project stages systematically to avoid standard budget overruns.

| Development Phase | Estimated Cost |

| Discovery, workflow mapping, SAR scope definition | $8,000–$20,000 |

| Evidence audit and data architecture | $12,000–$35,000 |

| Transaction, KYC, and case management integrations | $25,000–$90,000 |

| RAG and evidence retrieval layer | $25,000–$75,000 |

| LLM SAR narrative generation engine | $30,000–$90,000 |

| SAR quality scoring and hallucination controls | $20,000–$70,000 |

| Reviewer workflow and approval dashboard | $25,000–$80,000 |

| FinCEN filing workflow preparation | $15,000–$50,000 |

| Security, RBAC, encryption, audit trails | $20,000–$80,000 |

| MLOps, monitoring, model versioning | $18,000–$65,000 |

2. Structural Cost Tier Classifications

The final price tag remains deeply dependent on the overall number of live external data rails and the complexity of your risk scoring tools. Because of this variation, banks map capabilities to three defined execution levels.

- Controlled SAR Drafting MVP ($70,000–$140,000): Focuses on a single alert queue with limited integrations and direct human-in-the-loop review layers.

- Production SAR Automation Platform ($160,000–$420,000+): Connects multiple data streams, custom RAG pipelines, automated QA verification blocks, and unalterable audit trails.

- Advanced Agentic SAR Platform ($420,000–$750,000+): Incorporates multi-jurisdiction reporting, crypto analytics trackers, and autonomous investigation agents.

3. Projecting Long-Term Operational Maintenance

Ongoing maintenance usually costs 18%–28% of the initial build per year. This covers model monitoring, compliance updates, prompt improvements, source connector maintenance, security reviews, reviewer feedback tuning, SAR quality audits, and infrastructure operations.

Consequently, ignoring these running software charges will quickly lead to system drift as international crime patterns shift. Therefore, allocating continuous optimization funds ensures your application blocks new injection vulnerabilities and stays completely up to date with shifting FinCEN directives.

Ultimately, the technical engineering architecture chosen directly dictates your multi-year compliance budget and daily staff acceleration rates. Investing in rigorous data lineage logic stops automated text models from becoming expensive regulatory liabilities.

Build Generative AI SAR Drafting Software With Intellivon

Intellivon designs SAR drafting systems so every generated sentence can trace back to a source transaction, customer record, alert, document, or analyst note. This gives compliance teams a safer way to use generative AI without creating black-box narratives, unsupported claims, or regulatory review risk.

1.What Intellivon Helps You Build

- Evidence-grounded SAR drafting workflows: Pull transaction records, alert triggers, customer context, KYC/CDD data, case notes, and investigator findings into one structured drafting workspace.

- Reviewer-approved narrative generation: Generate first-draft SAR narratives that compliance officers can edit, approve, reject, or send back for additional investigation before filing.

- Typology-aware narrative support: Align draft narratives with suspicious activity patterns such as structuring, layering, mule activity, funnel accounts, rapid movement of funds, shell company behavior, sanctions exposure, or unusual cross-border activity.

- Source-linked sentence traceability: Connect key narrative claims to the exact transaction, customer profile, account activity, alert history, or case note that supports them.

- Human-in-the-loop approval controls: Keep investigators, AML officers, and compliance reviewers in full control of final SAR decisions, edits, escalations, and approvals.

- SAR quality and consistency checks: Review drafts for missing who, what, when, where, why, and how elements before the narrative moves forward.

- Case summarization and evidence grouping: Summarize long investigation records into clear timelines, suspicious activity patterns, counterparty relationships, and reviewer-ready evidence blocks.

- Audit-ready drafting history: Preserve prompt history, model version, source evidence, reviewer edits, approvals, overrides, and final narrative changes for internal review.

- Secure deployment architecture: Build private, access-controlled SAR drafting workflows with encryption, role-based access, logging, data residency controls, and model governance.

2. When to Build Generative AI SAR Drafting Software

A custom SAR drafting platform makes sense when your compliance team spends too much time assembling evidence manually, rewriting inconsistent narratives, or moving between disconnected case systems. It is also useful when SAR quality depends heavily on senior investigators because junior analysts lack enough context to write complete narratives quickly.

This build is especially relevant if your institution handles high alert volumes, complex payment flows, cross-border transactions, digital assets, layered entity relationships, or repeated suspicious activity patterns. In these cases, a generic writing assistant is not enough. The software must understand AML evidence, case workflow, reviewer authority, and reporting risk.

3. What You Get Before Full Development Begins

Before engineering starts, Intellivon helps your team define the SAR drafting workflow, evidence sources, AI boundaries, reviewer permissions, compliance risks, and technical scope. This gives compliance, risk, and technology leaders a clear build plan before investing in a production system.

The early-stage roadmap can include:

- SAR drafting workflow assessment

- Case evidence and data source mapping

- KYC, CDD, alert, and transaction data review

- Narrative template and typology library planning

- Human-review and approval workflow design

- Prompt, RAG, and model architecture planning

- Source citation and evidence traceability design

- Security, access-control, and audit-log requirements

- Model validation and hallucination-control framework

- MVP scope, cost range, timeline, and rollout roadmap

4. Why This Matters

Generative AI can speed up SAR drafting, but only when the system is controlled carefully. A weak implementation may create fluent narratives that miss key facts, overstate suspicion, invent unsupported links, or remove reviewer accountability.

Intellivon builds SAR drafting software around evidence first. The system helps investigators move faster, but it does not replace their judgment. Every draft remains reviewable, editable, traceable, and governed.

That balance matters because SAR drafting is not just a writing task. It is a regulated decision workflow where accuracy, timing, evidence quality, and human approval all matter.

If your compliance team is evaluating generative AI SAR drafting software, start with a workflow and evidence-readiness review before choosing models. Talk to Intellivon to scope your SAR drafting architecture, case data requirements, human-review controls, hallucination safeguards, compliance documentation, development cost, and rollout roadmap before committing to a full build.

Conclusion

Deploying AI for suspicious activity report generation shifts financial compliance from tedious drafting to strategic validation. By anchoring language engines to structured evidence ledgers, banks can automate high-volume narratives safely while maintaining total regulatory transparency. Success requires a governed, multi-model architecture that isolates factual data retrieval from text creation.

Ultimately, preserving human accountability at the review stage ensures every filed document remains accurate, defensible, and fully compliant.

Things To Know About AI SAR Automation Banking

Q1. Should banks build or buy AI SAR automation software?

A1. Banks should buy software when standard formatting and pre-filled forms are needed immediately. Conversely, they must build custom solutions when handling complex legacy integrations or unique digital asset rails. Ultimately, a hybrid model combining vendor delivery with custom-engineered drafting engines offers the highest operational flexibility.

Q2. Can AI reduce SAR backlogs without reducing compliance quality?

A2. AI accelerates evidence collection and narrative drafting to clear backlogs instantly. However, this automation must be bounded by strict quality tracking. By continuously monitoring factual accuracy and reviewer edit rates, compliance teams can safely speed up processing times without compromising regulatory integrity.

Q3. Does FinCEN allow AI-generated SAR narratives?

A3. FinCEN does not explicitly ban AI-generated narratives, provided they meet strict accuracy and completeness criteria. Under recent regulatory updates, examiners prioritize operational effectiveness and clear, factual timelines over checklist compliance. Consequently, keeping a human officer accountable for final verification ensures the system remains fully defensible.

Q4. Why is HIPAA-compliant SAR generation software not the right phrase for banking?

A4. HIPAA applies exclusively to protected healthcare information, making it irrelevant for standard financial reporting. Banks must instead design software to satisfy BSA, FinCEN, and GLBA privacy frameworks. Therefore, development teams should prioritize robust role-based access controls and encryption standards rather than medical compliance protocols.

To Sum Up:

- A SAR draft that sounds fluent but lacks evidence mapping creates more compliance risk than a slower manual process.

- The strongest AI SAR systems automate evidence assembly before they automate writing.

- SAR managers need sentence-level traceability, not just a generic audit log.

- A human-in-the-loop workflow only works when reviewers can inspect the source behind every material claim.

- The LLM is rarely the most expensive part of AI SAR automation; integrations, QA, governance, and audit controls drive the cost.